Getting an extra paycheck can feel like a lucky break. You open your account, see more money than usual, and suddenly it feels easier to spend without thinking too much.

But if you are paid biweekly, that extra paycheck is usually not a bonus. It happens because a biweekly schedule creates 26 paychecks per year, which means some months have three paychecks instead of two.

That makes the real question important: what should you do with an extra paycheck before it disappears?

The best answer is not always “save it” or “pay debt.” The best answer depends on your biggest financial pressure point right now. A third paycheck should not just give you a good weekend. It should make your next budget cycle easier.

Think of it as a cash-flow reset button.

Editor’s note: This article is for general budgeting education only. It is not personalized financial, tax, debt, or investment advice. For complex debt, tax, or investment decisions, consider speaking with a qualified financial professional.

First, Make Sure the Paycheck Is Actually Extra

Before you spend or transfer anything, check your next bill cycle.

A three-paycheck month can feel exciting, but your bills may not line up neatly with your paydays. Rent, mortgage, utilities, insurance, subscriptions, childcare, and automatic payments may still come due before your next regular paycheck arrives.

Use this quick check:

- List every bill due before your next payday.

- Keep enough in checking for those payments.

- Treat only the leftover amount as your true extra paycheck money.

Many people use the third paycheck for shopping or debt payoff immediately, then realize that rent, groceries, or insurance still needs money before the next payday.

That is why the first job of an extra paycheck should often be protection, not excitement.

Before deciding what to do with an extra paycheck, it helps to calculate monthly income from a biweekly paycheck so you understand whether the money is truly extra.

Biweekly Pay vs. Twice-a-Month Pay

This matters because not every pay schedule creates the same extra paycheck situation.

If you are paid biweekly, you are usually paid every 14 days. That can create two months each year with three paychecks.

If you are paid twice a month, such as on the 1st and 15th, you usually receive 24 paychecks per year. In that case, you may not get a true third paycheck month.

To check your own situation, look at your payday calendar and mark each payday. If three paydays fall inside one calendar month, that is your extra paycheck month.

An extra paycheck is easier to use well when you already know how to budget biweekly paychecks during normal months

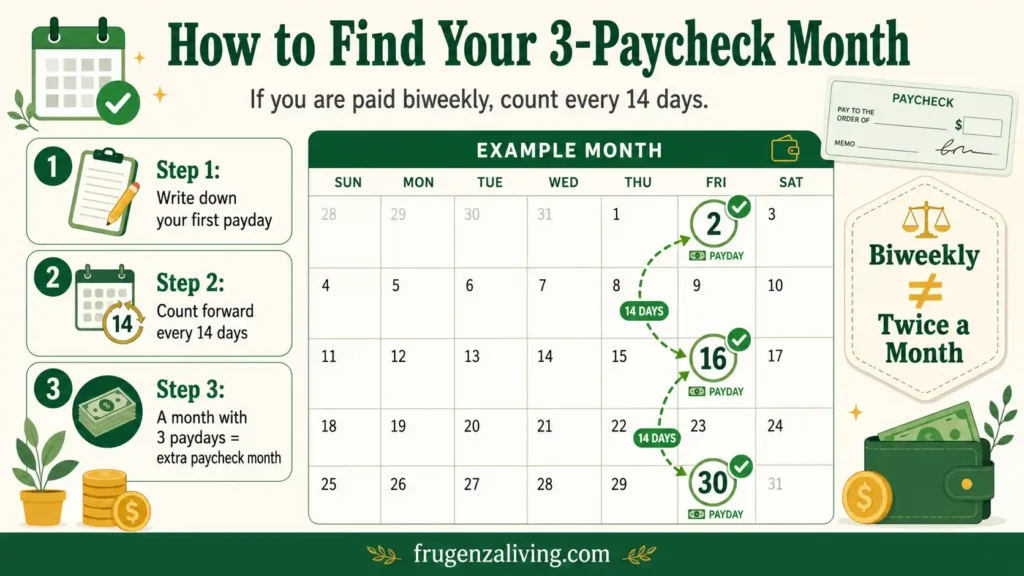

How to Find Your 3-Paycheck Months

You do not need a complicated tool to find your three-paycheck months.

Start with your first payday of the year. Then count forward every 14 days. Any month with three payday dates is a 3-paycheck month.

For example, if your first payday is Friday, January 2, count forward every 14 days: January 16 and January 30. That means January is a three-paycheck month for that schedule.

The 24-Hour Rule Before You Spend It

When the extra paycheck arrives, do not make a big money move immediately.

Give it 24 hours.

Leave the money in checking or move it to savings temporarily. Do not shop, upgrade your lifestyle, make a random debt payment, or divide the money into too many categories right away.

This short pause helps prevent invisible spending.

Invisible spending happens when extra money slowly disappears through takeout, groceries, online orders, upgrades, and small purchases. By the end of the month, the paycheck is gone, but nothing meaningful changed.

A 24-hour pause turns emotional money into intentional money.

A beginner paycheck budget worksheet can help you split an extra paycheck into savings, debt, sinking funds, and flexible spending.

Extra Paycheck Split Calculator

Use this simple calculator to give your extra paycheck a clear job before it disappears.

“`htmlExtra Paycheck Split Calculator

Enter your extra paycheck amount and choose the situation that fits you best.

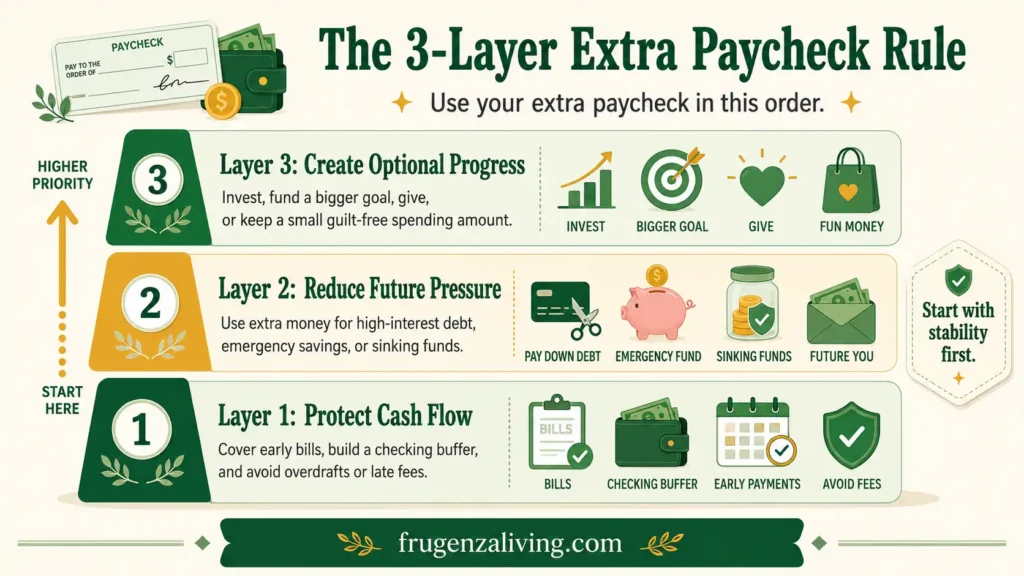

The 3-Layer Extra Paycheck Rule

Most extra paycheck advice sounds the same: save it, pay debt, invest it, or spend a little.

Those ideas are useful, but they can still feel too broad. A better way is to think in layers.

Layer 1: Protect cash flow.

Cover early bills, build a checking buffer, and prevent overdrafts or late payments.

Layer 2: Reduce future pressure.

Use the money for high-interest debt, emergency savings, or sinking funds.

Layer 3: Create optional progress.

Invest, fund a bigger goal, give, or allow a small guilt-free spending amount.

This order matters. If your checking account is constantly under pressure, investing the whole extra paycheck may look responsible but still leave you stressed next month.

Best Ways to Use an Extra Paycheck Based on Your Pressure Point

1. Build a Bill Buffer

A bill buffer is money kept in checking so your account is not always waiting for the next deposit.

This can be the best move if your rent, mortgage, car payment, or insurance is due early in the month. A buffer may not feel exciting, but it can reduce stress, late payments, overdraft risk, and credit card use between paydays.

2. Start or Refill an Emergency Fund

An emergency fund is cash set aside for unplanned expenses or financial emergencies. The Consumer Financial Protection Bureau describes emergency savings as a cash reserve for unexpected expenses such as car repairs, home repairs, medical bills, or loss of income.

If you do not have much saved, an extra biweekly paycheck can help you build a starter cushion. Even $500 to $1,000 can make a small emergency less damaging.

An extra paycheck can help you build emergency savings and sinking funds faster if you assign it before it gets absorbed into daily spending.

3. Make One Focused Debt Payment

If high-interest debt is your biggest pressure point, use part of the paycheck for one focused payment.

Some people choose the smallest balance for motivation, while others focus on the highest-interest balance to reduce interest pressure faster. The better choice depends on your cash flow, interest rates, and whether you can avoid adding new debt.

Just be careful not to send every dollar to debt if you have no cash cushion. Paying debt is helpful, but having no emergency savings can push the next surprise expense back onto a card.

4. Fund Predictable Expenses

Some expenses feel unexpected only because they do not happen every month.

Car insurance, holiday gifts, annual subscriptions, school costs, medical visits, home repairs, taxes, and travel often come back every year. An extra paycheck can help fund these sinking funds before the bill arrives.

Emergency savings are for unexpected problems. Sinking funds are for expected expenses that are easy to forget.

One smart use for an extra paycheck is building sinking funds for expenses that do not happen every month.

5. Get One Budget Category Ahead

You may not be able to get one full month ahead on everything. But you might be able to get ahead in one category.

For example, use part of the extra paycheck to pre-fund next month’s groceries, utilities, gas, or childcare. This can make your next paycheck feel less crowded.

The best use of extra money is often the one that removes your most repeated budget stress.

6. Invest After Short-Term Cash Is Stable

Investing part of an extra paycheck can make sense if your bills are current, emergency savings are stable, and high-interest debt is under control.

But if investing the money leaves you short for groceries, rent, or emergencies, your foundation may need attention first.

This is general education, not personal financial advice.

7. Keep a Small Guilt-Free Spending Portion

You do not have to be extreme.

If your bills are covered and most of the paycheck has a responsible job, it is okay to enjoy a small part of it. A simple range is 5% to 10%.

Planned spending is not the problem. Letting the whole paycheck disappear without a plan is.

Example: How to Split a $1,600 Extra Paycheck

Here are two practical examples.

Scenario A: You are behind on bills

- $1,100 bill buffer

- $300 emergency savings

- $200 groceries or gas

- $0 guilt-free spending

This plan prioritizes stability first. It may not feel fun, but it can stop the next month from starting in panic mode.

Scenario B: Your budget is stable

- $500 emergency fund

- $400 sinking funds

- $400 debt payoff or investing

- $160 guilt-free spending

- $140 checking cushion

This plan gives the paycheck several jobs without spreading it too thin.

What Not to Do With an Extra Paycheck

Avoid these mistakes:

Spending it before checking upcoming bills.

Your next bill cycle still matters.

Treating it like a bonus when you are behind.

A third paycheck can help you catch up, but it should not create false confidence.

Paying debt while leaving no emergency cushion.

Debt payoff is helpful, but a small cash reserve can prevent new debt.

Splitting it into too many tiny goals.

Choose one urgent goal and one future goal if you feel overwhelmed.

Creating a permanent lifestyle upgrade.

One extra paycheck should not create a new monthly payment or subscription.

Where This Fits in Your Bigger Budget

If you are paid biweekly, this extra-paycheck plan should sit beside your regular paycheck routine.

Your normal paychecks should cover bills and everyday spending. Your third paycheck should solve one specific problem, such as catching up, building a buffer, funding sinking funds, or getting one category ahead.

If you do not already have a system, start with a simple biweekly paycheck budget or use a paycheck budget template before your next 3-paycheck month. You can also reset your monthly budget before the next payday, set up sinking funds for predictable expenses, or separate spending categories with cash envelopes.

You do not need a complicated system. You need a clear job for the money before it disappears.

Final Thoughts

The best thing to do with an extra paycheck is to use it before it becomes invisible.

Start by checking upcoming bills. Then choose your biggest pressure point: bill timing, emergency savings, high-interest debt, future expenses, or long-term goals.

A third paycheck may feel like bonus money, but it can do much more than fund random spending. It can reset your cash flow, lower stress, and make your next budget cycle easier.

One extra paycheck may not fix everything. But one intentional paycheck can create progress you can actually feel.

FAQ

What should I do first with an extra paycheck?

First, check which bills are due before your next payday. Keep enough money in checking for those payments before using the rest for debt, savings, sinking funds, investing, or spending.

Is a third paycheck really extra money?

A third paycheck can feel extra, but it is not always free money. If you are paid biweekly, it usually happens because of the calendar. Always check your bills before treating it as extra.

What should I do with an extra paycheck when paid biweekly?

If you are paid biweekly, first check whether your bills are covered through the next payday. Then use the extra paycheck to build a buffer, pay high-interest debt, fund emergency savings, or prepare for upcoming expenses.

Should I save or pay off debt with an extra paycheck?

If you have no emergency cushion, saving part of the paycheck can help prevent new debt. If you already have some savings and high-interest debt, using a large portion for debt payoff may be more useful.

How do I budget a 3-paycheck month if I am behind on bills?

Use most of the extra paycheck to catch up and build a bill buffer. A simple split could be 70% for bills, 20% for emergency savings, and 10% for essentials.

How do I avoid wasting an extra paycheck?

Use a 24-hour pause, check bills due before your next payday, and assign the money to no more than three main purposes. The fewer jobs you give the paycheck, the easier it is to see progress.

The ideas shared here come from real-life experience and practical habits that actually work.

→ Read more about Jeffi

- How to Split Bills Between Paychecks Without Overloading One Check - August 9, 2026

- Subscription Audit Checklist: Find and Review Every Recurring Charge - August 9, 2026

- How to Budget for Subscriptions Without Surprise Renewals - August 7, 2026