You get paid every two weeks, but your rent, utilities, subscriptions, insurance, and credit card bills usually show up monthly.

That mismatch is what makes biweekly pay confusing.

You may think, “I’ll just multiply one paycheck by two.” That works for a normal two-paycheck month, but it does not show your average monthly income for the year.

If you want to know how to calculate monthly income from biweekly paycheck, you need more than a quick estimate. You need to know your yearly pay, average monthly income, real take-home pay, and how three-paycheck months fit into your budget.

The Calculation in One Sentence

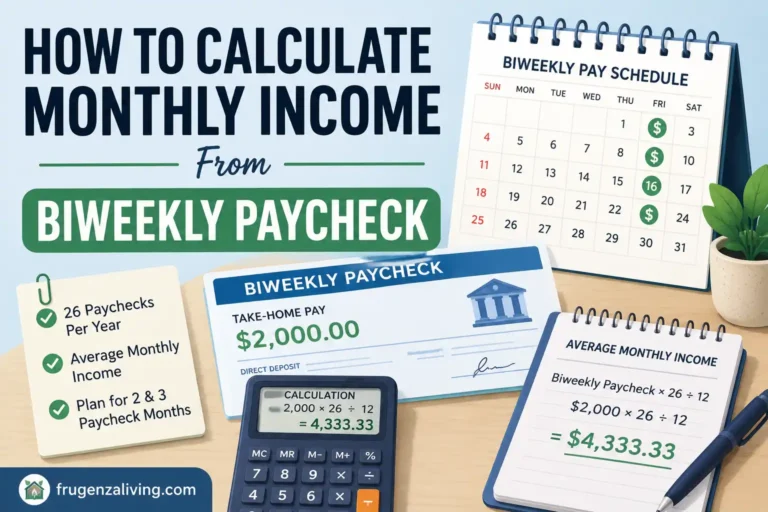

To calculate monthly income from a biweekly paycheck, multiply your take-home biweekly paycheck by 26, then divide by 12.

That gives your average monthly income.

The formula is:

Biweekly paycheck × 26 ÷ 12 = average monthly income

Example:

- Biweekly take-home paycheck: $2,000

- Annual take-home income: $2,000 × 26 = $52,000

- Average monthly income: $52,000 ÷ 12 = $4,333.33

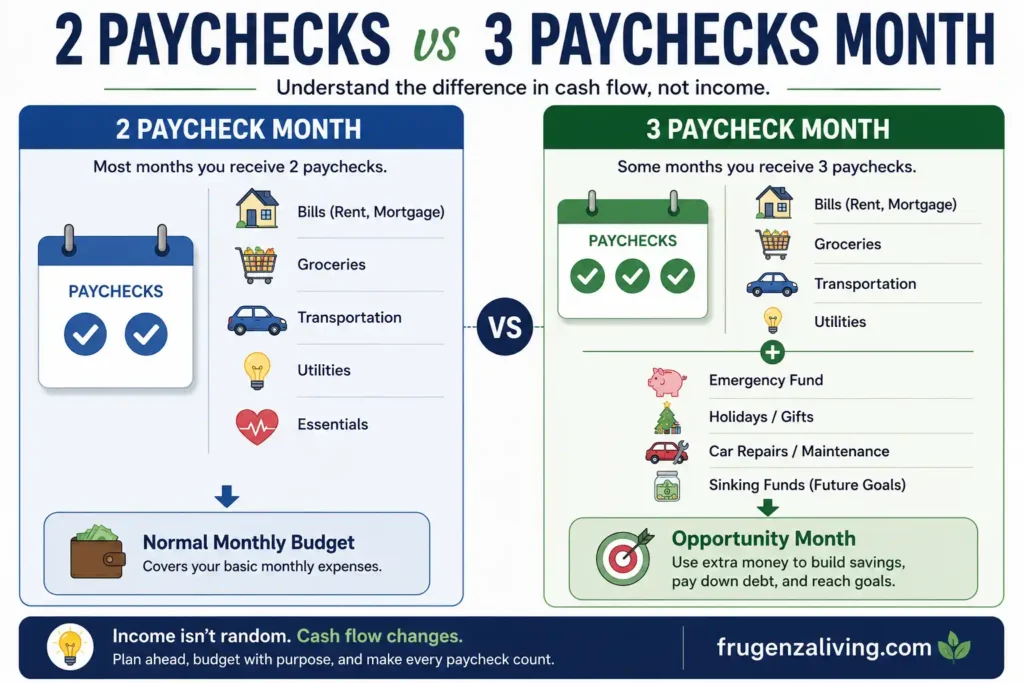

A normal two-paycheck month would deposit $4,000. Your average monthly income is higher because biweekly pay usually creates 26 paychecks per year, not 24.

The Biggest Biweekly Paycheck Mistake

The biggest mistake is treating a biweekly paycheck like a twice-a-month paycheck.

Twice-a-month pay usually means:

- 24 paychecks per year

- 2 paychecks every month

Biweekly pay usually means:

- one paycheck every 14 days

- 26 paychecks per year

- most months with 2 paychecks

- some months with 3 paychecks

That difference matters.

If you only double one paycheck, you are using a two-paycheck month as if it represents your whole year. But your two extra paychecks are still part of your annual income.

The better approach is to calculate annual income first, then divide it by 12.

A quick monthly budget review helps you compare your estimated income with what actually came in.

Biweekly Income Calculator

Use this calculator if you want the number first, then read the sections below to decide which number belongs in your monthly budget.

Frugenza Living · Calculator

Biweekly Paycheck → Monthly Income

Your Results

If you want to turn this number into a real plan, a paycheck budget template can help you organize bills, savings, and spending before the money disappears.

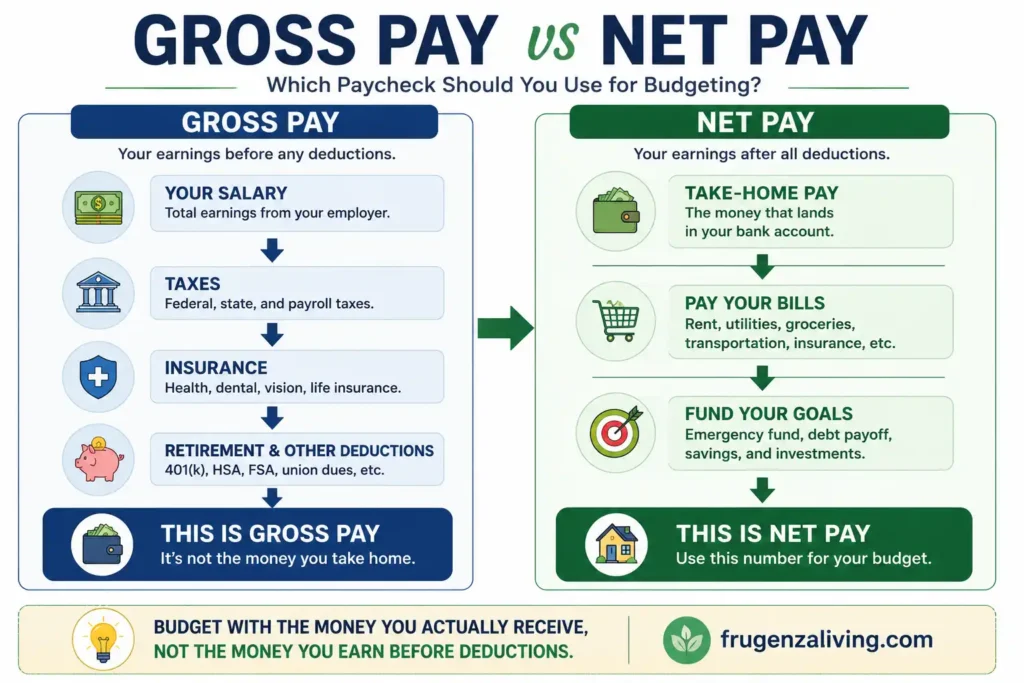

Which Paycheck Number Should You Use?

There are two income numbers:

- Gross pay: what you earn before taxes, insurance, retirement contributions, and deductions.

- Net pay: what actually lands in your bank account.

For monthly budgeting, use net pay whenever possible.

Use gross pay when you are:

- comparing job offers

- estimating salary

- applying for loans

- reviewing annual compensation

Use net pay when you are:

- paying bills

- budgeting groceries

- planning savings

- setting debt payments

- deciding what you can actually spend

If your tax withholding feels confusing, the IRS Tax Withholding Estimator can help you review withholding details. For monthly planning, the CFPB also provides budgeting resources that can help you compare income, expenses, and spending categories.

Which Monthly Number Should You Use?

Do not use the same number for every budgeting decision.

Use this simple guide:

| Situation | Best Number to Use |

|---|---|

| Paying fixed monthly bills | 2-paycheck month income |

| Planning your yearly budget | Average monthly income |

| Estimating salary | Gross annual income |

| Budgeting everyday spending | Net take-home pay |

| Handling overtime or variable pay | Conservative average |

| Planning extra paycheck months | Extra paycheck ladder |

This is the part many people miss.

Your average monthly income helps you understand the year. But your two-paycheck month income should still cover your basic bills.

That prevents you from building a monthly budget around money that only arrives in certain months.

A simple payday budgeting routine can help you use your income number before spending starts.

What If Your Biweekly Paycheck Changes?

Not everyone has the same paycheck every two weeks.

Your income may change because of:

- overtime

- commissions

- bonuses

- unpaid time off

- shift changes

- variable hours

- changing deductions

If your paycheck changes, do not use your highest paycheck as your monthly income estimate.

Instead:

- average your last 3–6 normal paychecks

- exclude one-time bonuses if they are not reliable

- use your lowest predictable paycheck for essential bills

- treat overtime as extra until it becomes consistent

- update your estimate when deductions change

This makes your budget safer.

For example, if your take-home checks are $1,850, $2,100, $1,950, and $2,400 because of overtime, do not build your rent and bills around $2,400. Use a conservative number closer to your normal base pay.

Your Paycheck Calendar Is Not Your Budget

Biweekly income can feel inconsistent because your cash flow changes.

Your bills may stay monthly, but your paychecks move through the calendar.

Think of it this way:

- annual income is the full picture

- 26 paychecks are the delivery schedule

- average monthly income is the planning number

- paycheck dates are the cash-flow timing

A two-paycheck month may feel tighter.

A three-paycheck month may feel easier.

But the income itself is not random. The timing is.

For a full system, read this guide on how to budget biweekly paychecks.

The 5 Calculation Traps

1. Multiplying One Paycheck by Two

This shows a normal two-paycheck month, but it does not show average monthly income from biweekly pay.

Better move: multiply by 26, then divide by 12.

2. Using Gross Pay for Everyday Budgeting

Gross pay can make your budget look bigger than your real spending money.

Better move: use your actual deposit amount after deductions.

3. Budgeting With Your Best Paycheck

If you use a high-overtime paycheck, normal months may feel short.

Better move: use a conservative average or your lowest predictable paycheck.

4. Treating Extra Paychecks Like Free Money

A third paycheck feels like a bonus, but it is part of your yearly income.

Better move: give it a job before it arrives.

5. Forgetting Annual Expenses

Car maintenance, gifts, insurance, medical costs, and holidays can surprise you.

Better move: identify your top 3–5 annual expenses (car maintenance, insurance renewal, holiday gifts, medical copays) and estimate a monthly amount for each. Divide the total by 12, then treat that as a hidden monthly bill. For example, if your car maintenance runs about $600/year, that's $50/month you need to account for even when no bill arrives.

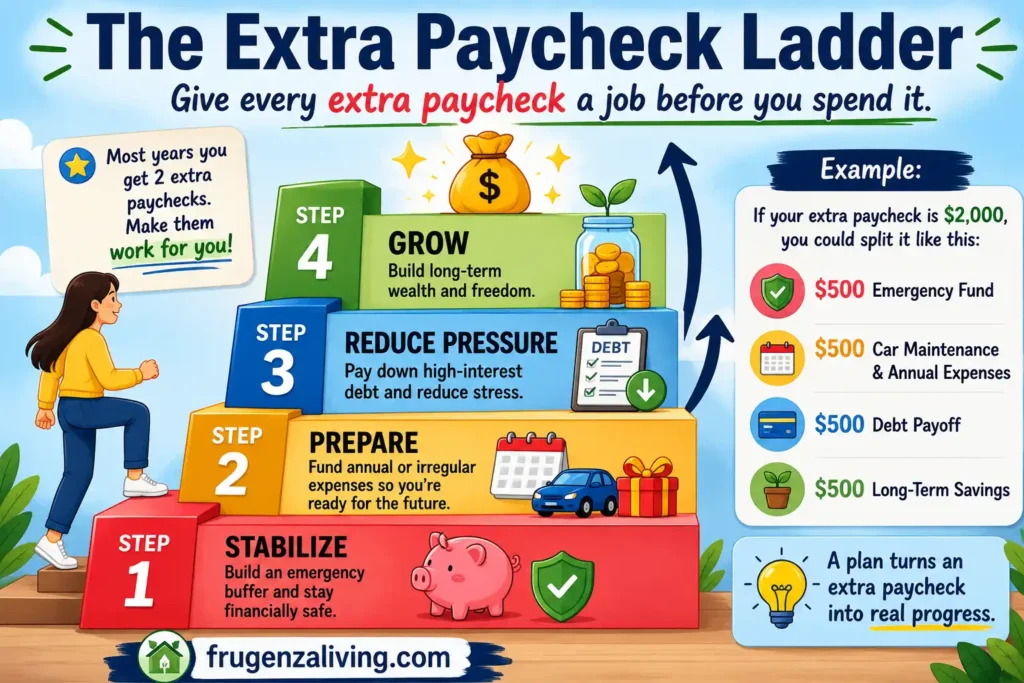

The Extra Paycheck Ladder

Most years, biweekly workers have two months with three paychecks. Instead of treating those checks as random spending money, use a ladder.

Start at the bottom and move up only when the earlier step is handled.

Most years, biweekly workers have two months with three paychecks. Instead of treating those checks as random spending money, use a ladder.

Start at the bottom and move up only when the earlier step is handled.

Step 1: Stabilize

Before anything else, confirm that your regular monthly bills are fully covered from your two standard paychecks. The extra paycheck should only be assigned after essentials are secured. If your two-paycheck months still feel tight, use Step 1 to fill that gap first.

Step 2: Prepare

Fund irregular expenses like insurance renewals, car maintenance, medical costs, or holiday spending.

Step 3: Reduce Pressure

Pay down high-interest debt or reduce next month's financial stress.

Step 4: Grow

Add to long-term savings after urgent and irregular expenses are covered.

Example: if your extra paycheck is $2,000, you might use:

- $500 for emergency savings

- $500 for car maintenance

- $500 for holiday or annual expenses

- $500 for debt or next month's buffer

The exact split can change. The point is to decide before the money arrives.

For a deeper guide on what to do with an extra paycheck, see what to do with an extra paycheck before it disappears

Example:

If your extra paycheck is $2,000, you might use:

- $500 for emergency savings

- $500 for car maintenance

- $500 for holiday or annual expenses

- $500 for debt or next month’s buffer

The exact split can change. The point is to decide before the money arrives.

The Income Confidence Check

Before building your monthly budget, ask:

- Do I know my take-home biweekly paycheck?

- Do I know my annual income from 26 paychecks?

- Do I know my average monthly income?

- Do I know my three-paycheck months?

- Do I have a plan for extra paychecks?

- Am I budgeting from normal income, not my highest paycheck?

If you can answer these questions, your budget is already stronger than a budget built on guesses.

For a worksheet-style setup, a paycheck budget template can help you connect paydays, bills, savings, and spending in one place.

What Helped Me Understand Biweekly Income

The first time I noticed this problem, one month felt comfortable and the next month felt tight, even though my paycheck amount had not changed.

That confused me until I looked at the calendar.

My income was not changing.

My paycheck timing was.

Once I separated income from cash flow, budgeting felt easier. Extra paychecks stopped feeling like surprise money. They became scheduled tools for future expenses.

That shift made monthly budgeting feel less emotional and more predictable.

Final Thoughts

Learning how to calculate monthly income from biweekly paycheck is not just about multiplying numbers.

It is about choosing the right number for the right job.

Remember:

- biweekly pay usually means 26 paychecks a year

- one paycheck × 26 ÷ 12 gives average monthly income

- net pay is better for real-life budgeting

- two-paycheck months should cover your basics

- variable pay should be estimated conservatively

- three-paycheck months should have a plan

Income is not random.

Cash flow is.

Once you understand the difference, monthly budgeting becomes much easier.

The ideas shared here come from real-life experience and practical habits that actually work.

→ Read more about Jeffi

- How to Split Bills Between Paychecks Without Overloading One Check - August 9, 2026

- Subscription Audit Checklist: Find and Review Every Recurring Charge - August 9, 2026

- How to Budget for Subscriptions Without Surprise Renewals - August 7, 2026