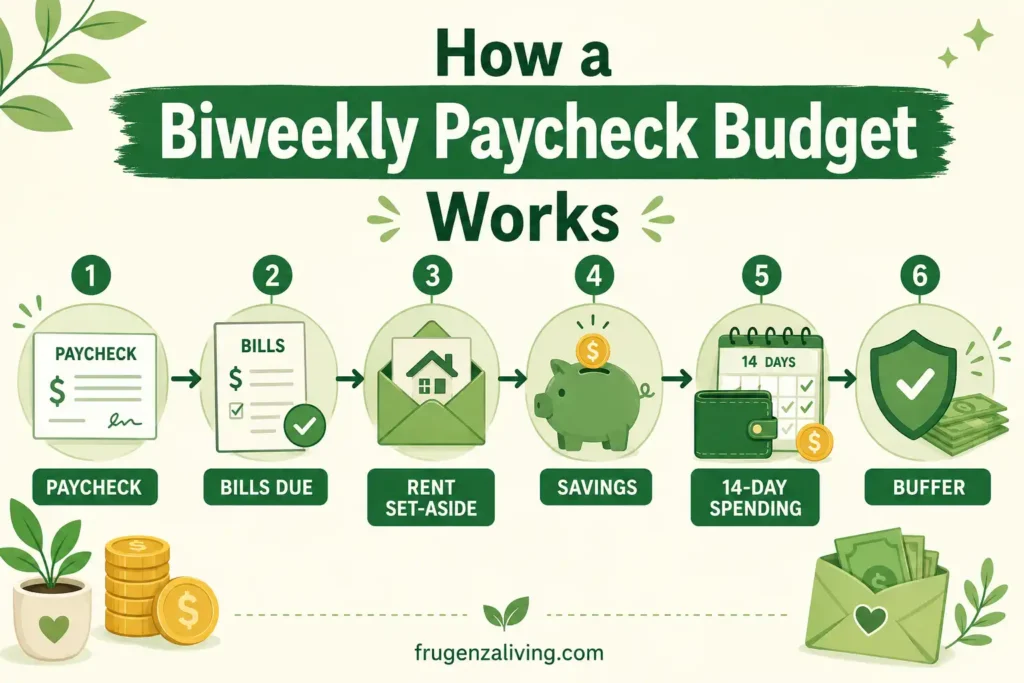

Getting paid every two weeks can feel simple until your bills follow a monthly schedule.

Rent may be due on the 1st, utilities near the end of the month, subscriptions on random dates, and groceries every week. That timing mismatch is why many people feel behind even when their income should technically be enough.

The easiest way to budget biweekly paychecks is to plan one paycheck at a time. Instead of asking, “Can I afford this month?” ask, “What does this paycheck need to cover before the next one arrives?”

In this guide, you’ll build a simple biweekly budget plan for bills, savings, sinking funds, 14-day spending, and three-paycheck months. This is general budgeting guidance, not professional financial advice, but it can help you create a system that feels realistic instead of overwhelming.

Quick Answer: How to Budget Biweekly Paychecks

To budget biweekly paychecks, list your bills by due date, assign each bill to the paycheck before it is due, set aside savings and debt payments, then divide the remaining money across the next 14 days.

Use two regular paychecks for your normal monthly budget and treat third-paycheck months as extra money for savings, debt, or sinking funds.

What Makes a Biweekly Paycheck Budget Different?

A biweekly pay schedule means you get paid every 14 days. In most years, that gives you 26 paychecks instead of 24.

That small detail matters.

If you budget monthly, you may only look at your total income and total expenses. But when you are paid every two weeks, timing matters just as much as the total amount. You might earn enough to cover your bills, but if rent is due before your next paycheck, your budget can still feel tight.

For example, your rent may be due on the 1st, your car payment on the 15th, utilities on the 22nd, and groceries every week. Meanwhile, your paycheck dates keep shifting throughout the year.

A monthly budget gives you the big picture. A biweekly paycheck budget helps you manage the money that is actually available right now.

Step 1: Start With Your Real Take-Home Pay

Before you build a biweekly budget plan, start with your net income, not your gross income.

Gross pay is the amount before taxes, insurance, retirement contributions, and other deductions. Net pay is the money that actually lands in your bank account. Your budget should be based on the amount you can really use.

If your paycheck changes because of overtime, tips, bonuses, or commissions, use a conservative number. It is safer to build your budget around your lowest usual paycheck and treat extra income as a bonus.

For example:

- Biweekly paycheck: $1,650

- Normal two-paycheck month: $3,300

- Three-paycheck month: $4,950

Do not build your normal monthly budget around the three-paycheck month. Since those months do not happen every month, that extra paycheck should have a separate plan.

A safer rule is this: use two paychecks for your normal bills and treat the third paycheck as a tool for savings, debt, or catching up.

Before your next payday, it helps to divide your paycheck properly across bills, savings, and flexible spending.

Step 2: Build a Bill Calendar for Biweekly Pay

A bill calendar is one of the most useful tools for budgeting with biweekly paychecks.

This does not need to be fancy. You can use a spreadsheet, a budgeting app, a notebook, or even the notes app on your phone.

Create a simple list with these columns:

- Bill name

- Amount

- Due date

- Paid from paycheck #1 or paycheck #2

- Autopay or manual payment

Include every fixed or semi-fixed expense, such as rent, utilities, phone, internet, car insurance, minimum debt payments, subscriptions, childcare, medical payments, and loan payments.

This step matters because many people do not fail at budgeting because the total numbers are wrong. They struggle because the timing is wrong.

A simple bill calendar for biweekly pay might look like this:

Paycheck #1 can cover:

- Rent set-aside

- Phone bill

- Groceries for week 1 and week 2

- Minimum debt payment

- Small buffer

Paycheck #2 can cover:

- Utilities

- Internet

- Insurance

- Groceries for week 3 and week 4

- Rent set-aside for next month

A $90 bill due tomorrow is more urgent than a $200 bill due three weeks from now. Once you know what each paycheck must cover, your budget becomes easier to control.

For a broader explanation of basic money planning, you can also check a trusted source like Consumer.gov’s money management guide

Step 3: Use the Biweekly Payday Priority Order

Before you spend from a new paycheck, give the money a job in the right order.

A simple payday priority order looks like this:

- Bills due before the next payday

- Rent or mortgage set-aside

- Minimum debt payments

- Savings or sinking funds

- 14-day spending money

- Small buffer

This order matters because flexible spending should not come before bills that are already due. If you buy groceries, gas, takeout, and household items first, you may accidentally leave yourself short for a bill that hits in three days.

This is the part most people skip. The goal is not to make your budget strict. The goal is to protect the money that already has a job.

After a few pay cycles, you will usually spot the same pressure points. Maybe rent always makes paycheck #1 feel tight. Maybe subscriptions pile up near the end of the month. Maybe grocery spending gets too loose in the first week after payday.

That pattern is useful because it shows you what to fix first.

Since two weeks can feel long between paychecks, using a simple weekly budget can help you stay in control.

Step 4: How to Split Bills Between Biweekly Paychecks

The next step is to divide your bills between your two regular paychecks.

A simple approach is:

- Paycheck #1 covers bills due in the first half of the month.

- Paycheck #2 covers bills due in the second half of the month.

But this does not always work perfectly.

Some bills are too large to handle from one paycheck alone. Rent is the most common example. If your rent is due at the beginning of the month, paycheck #1 may feel completely drained unless you start setting aside part of rent from paycheck #2 in the previous month.

Here is a simple paycheck budget example.

Paycheck #1: $1,650

- Rent set-aside: $900

- Phone: $60

- Groceries and gas: $300

- Savings: $100

- Debt minimum: $90

- Buffer and misc: $200

Paycheck #2: $1,650

- Utilities: $180

- Insurance: $140

- Internet: $70

- Groceries and gas: $300

- Rent set-aside for next month: $600

- Savings: $150

- Buffer and misc: $210

This is only an example, but the idea is important. You are not just paying bills. You are assigning each paycheck a job.

That is the core of the paycheck budgeting method. Your paycheck system becomes more useful when it fits inside a simple money management plan you can repeat every month.

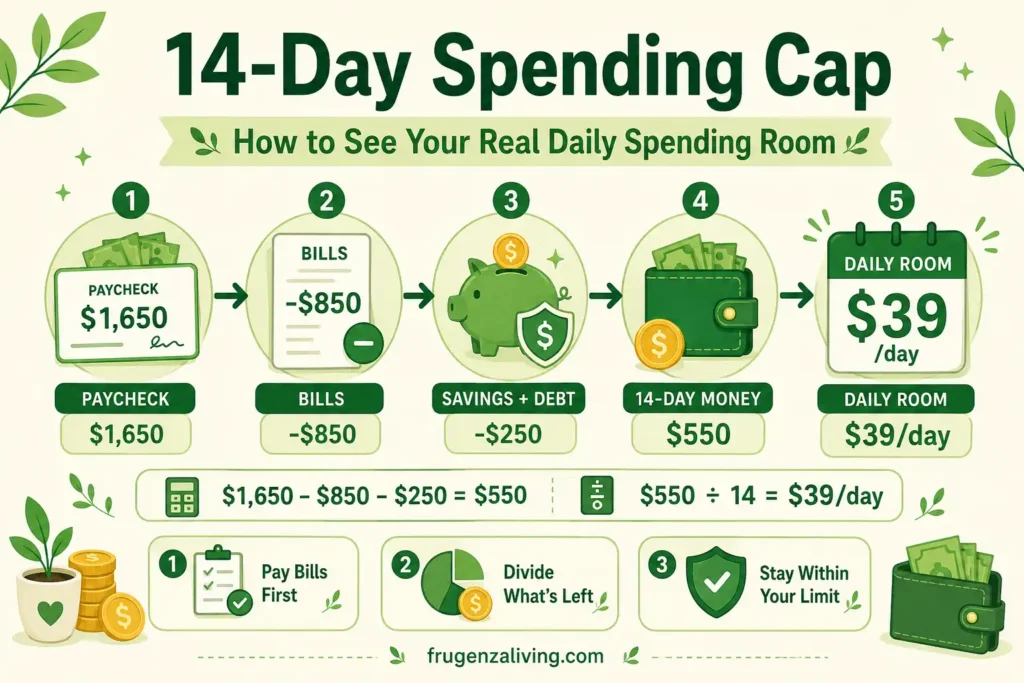

Step 5: Create a 14-Day Spending Cap

This is where a biweekly income budget becomes much more practical.

Many people know their bills but still run out of money because their daily spending has no clear limit. Groceries, gas, takeout, household items, coffee, small subscriptions, and quick online purchases can quietly eat the budget.

A 14-day spending cap helps you know how much money you can safely spend before the next paycheck.

Use this formula:

Biweekly paycheck – bills due before next payday – savings – debt payments = 14-day spending money

For example:

$1,650 – $850 bills – $150 savings – $100 debt = $550 for 14 days

Then divide it by 14:

$550 ÷ 14 = about $39 per day

That does not mean you should spend $39 every day. It simply shows your real breathing room.

If you spend $120 on groceries one day, that is fine, but now you understand how it affects the rest of the 14-day period.

Before building a biweekly budget, it helps to calculate monthly income from a biweekly paycheck so you know your real average monthly number.

This is especially helpful if you are trying to build better spending habits without making your budget feel too strict.

If you get paid every two weeks, it helps to manage money after payday so your income lasts until the next paycheck.

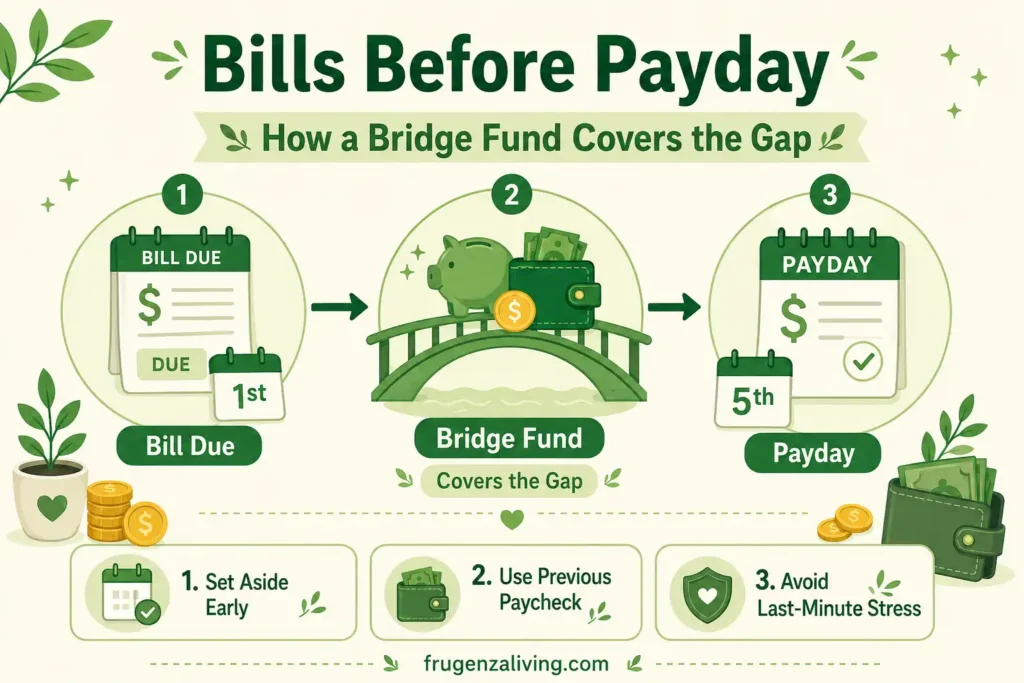

Step 6: What If a Bill Is Due Before Your Next Paycheck?

This is one of the most frustrating parts of monthly bills on a biweekly income.

Maybe rent is due on the 1st, but your paycheck does not arrive until the 5th. Or your insurance payment hits two days before payday. When that happens, the solution is not to hope the timing works out. You need a small bridge.

A bridge fund is a mini buffer that protects you when a bill is due before your next paycheck. It is not a full emergency fund. It is simply money that helps you cross the gap between bill dates and payday.

Start small if you need to:

- First goal: $100

- Better goal: $300

- Stronger goal: one week of basic expenses

You can build it slowly from leftover money, third-paycheck months, tax refunds, or small automatic transfers.

Another option is to ask a service provider if your due date can be moved. This will not work for every bill, but it can help with some utilities, phone bills, credit cards, or insurance payments.

The key rule is simple: if a bill is due before your next paycheck, it should be funded from the previous paycheck.

To see how this works with real numbers, you can compare it with a simple monthly budget example.

Step 7: Use Sinking Funds for Expenses That Don’t Happen Every Paycheck

A common mistake in paycheck-to-paycheck budgeting is only planning for obvious monthly bills.

But real life includes expenses that do not happen every two weeks.

That is where sinking funds help.

A sinking fund is money you set aside little by little for a future expense. Instead of panicking when the bill appears, you prepare for it in small amounts.

Good sinking fund categories include:

- Car maintenance

- Annual subscriptions

- Holiday gifts

- Insurance premiums

- Medical copays

- School expenses

- Clothing

- Home repairs

- Pet care

For biweekly paychecks, the math is simple:

Annual expense ÷ 26 = amount to save per paycheck

For example, if you want $520 per year for car maintenance:

$520 ÷ 26 = $20 per paycheck

That small amount can protect your budget from being wrecked by one irregular expense.

If saving every paycheck feels hard, start small. Even a weekly or biweekly habit can make future expenses less stressful.

Step 8: What If Your Biweekly Paychecks Are Not the Same Amount?

Not every biweekly paycheck is identical.

If you work hourly, earn tips, get commissions, or rely on overtime, your income may change from one paycheck to the next. In that case, avoid building your budget around your best paycheck.

Use your lowest normal paycheck as the base.

For example, if your paychecks usually range from $1,450 to $1,750, build your basic budget around $1,450. Then use the extra money from larger paychecks for savings, debt, sinking funds, or a small buffer.

This protects you from depending on income that may not show up every time.

A simple rule:

Base bills on your lowest usual paycheck. Use extra income to get ahead.

This one change can make a biweekly budget feel much safer, especially if your work schedule changes often.

A Simple Biweekly Budget Template You Can Copy

Use this template before each payday. It gives your paycheck a clear job before the money starts disappearing into bills, groceries, gas, and random purchases.

First, fill it out before payday or on payday morning. Then pay or set aside money for bills first. After that, move money to savings or sinking funds. Finally, divide the remaining money across your 14-day spending categories.

Before your next paycheck, take 10 minutes to review what worked and what felt unrealistic. That small review helps you improve the next budget without starting over.

Paycheck Budget Example: A Realistic Two-Paycheck Budget

Let’s look at a simple two paycheck budget for someone earning $3,600 per month from two regular paychecks.

Each paycheck is $1,800.

Monthly bills and goals:

- Rent: $1,200

- Utilities: $180

- Phone: $60

- Internet: $70

- Car insurance: $140

- Debt minimums: $150

- Groceries and gas: $600

- Savings: $250

- Miscellaneous buffer: $250

Paycheck #1: $1,800

- Rent: $1,200

- Phone: $60

- Groceries and gas: $300

- Savings: $100

- Buffer: $140

Paycheck #2: $1,800

- Utilities: $180

- Internet: $70

- Car insurance: $140

- Debt minimums: $150

- Groceries and gas: $300

- Savings: $150

- Rent set-aside for next month: $600

- Buffer: $210

Notice that paycheck #2 does not only cover second-half bills. It also prepares part of next month’s rent. That is what keeps paycheck #1 from becoming overloaded every month.

If your rent is due before your first paycheck of the month, your rent set-aside should start from the previous paycheck, not the current one.

Step 9: Decide What to Do With a 3-Paycheck Month Before It Arrives

One of the best parts of biweekly pay is the three-paycheck month.

Since there are usually 26 paychecks in a year, you will have some months where you receive three paychecks instead of two. This can feel like extra money, but it is better to plan for it before it arrives.

A smart 3 paycheck month budget might include:

- Build your emergency fund

- Pay down high-interest debt

- Catch up on delayed bills

- Fund sinking funds

- Save for a planned purchase

- Allow a small guilt-free spending amount

For example, if your third paycheck is $1,650, you could divide it like this:

- Emergency fund: $700

- Debt payment: $400

- Car repair fund: $300

- Annual subscriptions: $150

- Guilt-free spending: $100

This gives the paycheck a purpose without making the plan feel miserable.

You do not have to use every dollar for serious goals. A small amount of fun money can make your budget easier to stick with long term.

Common Biweekly Budgeting Mistakes to Avoid

Even a good budget can fail if a few small problems keep repeating. Here are the most common mistakes to watch for:

- Budgeting Monthly but Spending Biweekly: A monthly budget can show the big picture, but it may not show what your current paycheck can actually handle. Always check what needs to happen before the next payday.

- Forgetting About Bills Due Before the Next Paycheck: Due dates matter. A bill due in three days should be handled before money goes to flexible spending.

- Treating the Third Paycheck Like Free Money: A third paycheck can help you get ahead, but only if it has a plan. Decide where it will go before it hits your account.

- Not Separating Rent or Mortgage Early Enough: If rent takes most of one paycheck, start setting aside part of it from the previous paycheck. This can make the beginning of the month less stressful.

- Ignoring Small Subscriptions: A few small subscriptions can quietly drain your buffer. Review them at least once a month.

- Using Average Income That Includes Overtime: If overtime is not guaranteed, do not build your basic budget around it. Use it for savings, debt, or catch-up goals instead.

- Making the Budget Too Strict: A budget with no room for real life usually does not last. Include a small buffer when possible.

Final Thoughts: Make Payday Less Stressful

Learning how to budget biweekly paychecks is not about creating a perfect spreadsheet or tracking every penny forever.

It is about matching your money to your real life.

Your bills have due dates. Your paychecks arrive every 14 days. Your groceries, gas, savings, and personal spending all need space too. When you plan one paycheck at a time, the system becomes easier to understand.

Start with your take-home pay. Build a bill calendar for biweekly pay. Use a payday priority order. Split bills between paycheck #1 and paycheck #2. Create a 14-day spending cap. Use a bridge fund when bills arrive before payday. Then make a plan for every third paycheck month before it arrives.

A simple biweekly budget can make payday feel less like a reset button and more like a plan you actually control.

FAQ

How do I budget if I get paid every two weeks?

The easiest way is to budget by paycheck. List the bills due before your next payday, subtract savings and debt payments, then use the remaining money for groceries, gas, personal spending, and a small buffer.

How do I split monthly bills between biweekly paychecks?

List your bills by due date, then assign each bill to the paycheck that arrives before the due date. If one bill is too large, like rent or mortgage, split it across two paychecks.

How do I handle rent with biweekly paychecks?

If rent is too large for one paycheck, set aside part of it from the previous paycheck. For example, you might save part of next month’s rent from paycheck #2 so paycheck #1 does not have to carry the full amount alone.

How do I budget biweekly paychecks with variable income?

Use your lowest normal paycheck as your base budget. Then use extra money from overtime, tips, bonuses, or larger paychecks for savings, debt, sinking funds, or a small buffer.

What should I do with a third paycheck month?

Use a third paycheck month to get ahead. Good options include building an emergency fund, paying down high-interest debt, catching up on bills, funding sinking funds, or saving for a planned purchase.

The ideas shared here come from real-life experience and practical habits that actually work.

→ Read more about Jeffi

- How to Stop Buying Coffee Every Day Without Giving Up Coffee - July 25, 2026

- 8 Meals for One Without Leftovers—and How to Use the Rest - July 22, 2026

- 9 Cheap Dinners for One Person on a Budget That Feel Complete - July 20, 2026