Getting paid should feel good, but sometimes it creates a different kind of stress.

You look at your income and think, “How much should go to bills? How much should I save? How much can I actually spend without messing up the month?”

That confusion is normal.

Many beginners do not struggle because they are bad with money. They struggle because their income has no clear order after payday.

That is where learning how to split income for budgeting can help.

Income splitting does not mean using perfect percentages or following a strict financial rule. It simply means deciding where your money should go first, second, and last.

The goal is not perfection.

The goal is clarity.

How Should You Split Income for Budgeting?

To split income for budgeting, start with essentials first, set aside money for savings, debt, or future expenses next, then decide how much is safe for flexible spending. Your income split should match your real income, bills, and lifestyle instead of forcing perfect percentages.

What This Income Split Helps You Decide

A simple income split helps you understand:

- what must be paid first

- how much you can safely spend

- how much can go toward savings or debt

- what needs adjusting when money feels tight

Instead of guessing after payday, you give your money a clear direction.

Before splitting your income, it’s important to understand how to start budgeting properly.

Split Your Income by Priority, Not Pressure

Many beginners start budgeting by searching for the perfect percentage.

Should rent be 30%?

Should savings be 20%?

Should fun money be 10%?

Percentages can be helpful, but they can also create pressure.

Real life does not always fit neatly into a perfect formula. Your rent may be high. Your income may change. You may have debt, medical costs, family support, or irregular expenses.

That is why splitting income by priority works better than splitting it by pressure.

Start with what must be covered.

Then protect your future money.

After that, decide what is left for flexible spending.

Splitting income is not about perfect percentages. It is about giving your money a clear order of priority.

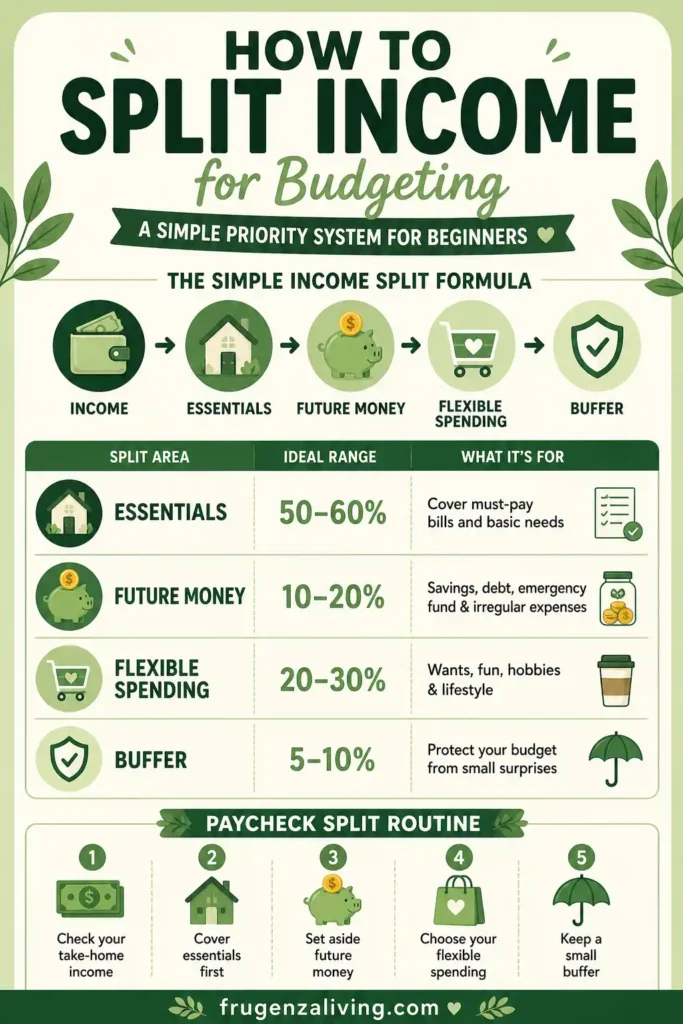

The Simple Income Split Formula

A beginner-friendly income split can follow this order:

Income → Essentials → Future Money → Flexible Spending → Buffer

Here is what that means:

| Income Split Area | What It Covers | Why It Comes Here |

|---|---|---|

| Essentials | Housing, groceries, bills, transportation | These protect your basic stability |

| Future Money | Savings, debt, emergency fund, irregular expenses | This prepares you for later |

| Flexible Spending | Dining out, entertainment, hobbies, personal spending | This gives you room to enjoy life safely |

| Buffer | Small unexpected costs | This keeps small surprises from breaking the plan |

This formula is simple enough for beginners because it does not ask you to manage too many details at once.

It only asks:

“What needs to happen first?”

A Practical Income Split Example

Here is a simple income allocation example based on $2,000 take-home income.

This is not a full monthly budget breakdown. It is just a clear example of how to divide income into main groups.

| Split Area | Example Amount | Purpose |

|---|---|---|

| Essentials | $1,100 | Cover housing, food, bills, and transportation |

| Future Money | $300 | Build savings, pay debt, or prepare for irregular expenses |

| Flexible Spending | $450 | Use for dining out, hobbies, entertainment, and personal spending |

| Buffer | $150 | Protect the budget from small surprises |

This kind of simple income split works because it gives every major money area a place without turning budgeting into a complicated system.

One reason people feel broke after payday is that they do not split their paycheck before spending begins.

Quick Income Split Snapshot

If you want a fast way to remember the order, use this:

- Essentials: pay what must be paid

- Future Money: protect savings, debt, and irregular expenses

- Flexible Spending: spend safely after priorities are covered

- Buffer: protect yourself from small surprises

This keeps your income split simple without making it too rigid.

A structured approach like zero-based budgeting can help you assign every dollar intentionally.

How Much Income Should Go to Essentials?

Essentials usually take the largest part of your income.

This includes things like:

- housing

- groceries

- utilities

- transportation

- phone bill

- insurance

- basic required payments

Many people aim to keep essentials around 50–60% of income, but real life varies.

If your essentials are higher than that, it does not automatically mean you failed. It may simply mean your rent, location, income, or fixed bills make your situation tighter.

The important thing is to know the number.

If essentials take most of your income, you may need to reduce pressure somewhere else instead of forcing an unrealistic savings or spending goal.

How Much Should Go to Savings, Debt, and Future Money?

Future money includes anything that protects you later.

That may include:

- savings

- emergency fund

- debt payments

- irregular expenses

- future bills

- car repairs

- medical costs

A common beginner mistake is saving only whatever is left over.

The problem is that there may be nothing left.

That is why future money should have a place near the beginning of your income split, even if the amount is small.

If money is tight, start with 5–10%.

To stay consistent, it helps to follow a simple weekly budgeting plan that matches your income.

Even a small amount can build momentum because it creates the habit of setting money aside before everything disappears.

You can increase it later when your income grows or your expenses become easier to manage.

How Much Income Can You Use for Flexible Spending?

Flexible spending comes after essentials and future money.

This includes:

- dining out

- coffee

- entertainment

- hobbies

- shopping

- small personal purchases

- weekend plans

This category matters because people still need room to live.

A budget that leaves no flexible spending often becomes too strict and hard to maintain.

But flexible spending should be clear.

When you know the amount, you can spend without guilt because the important parts are already covered.

If you often overspend here, the problem may not be the category itself. It may be that the limit is unclear or too easy to ignore.

What If Your Income Is Low or Expenses Are High?

If your income is low or expenses are high, do not force a perfect split.

Start with stability:

- Cover essentials first: Protect your basic needs.

- Keep future money small but visible: Even $10 or $20 matters if it keeps the habit alive.

- Reduce flexible spending temporarily: Give yourself room to breathe.

- Keep a smaller buffer: Just enough to prevent overdrafts or small surprises.

The goal is not to copy someone else’s percentages.

The goal is to make your current income easier to manage.

A tight income split might look less balanced, but it can still be useful if it shows you what is realistic.

A Simple Paycheck Split Routine

You can use this routine every time money comes in.

If you are wondering how to split paycheck for bills and savings, this gives you a simple order to follow after every payday.

1. Check Your Take-Home Income

Start with the amount you actually receive after taxes and deductions.

This is the real number you can split.

2. Cover Essentials

Set aside money for bills, groceries, housing, transportation, and required payments.

These come first because they protect your basic needs.

3. Set Aside Future Money

Choose an amount for savings, debt, emergency fund, or irregular expenses.

Start small if needed.

4. Choose Flexible Spending

Decide how much you can safely use for personal spending, dining out, entertainment, or hobbies.

This gives you freedom without guessing.

5. Keep a Buffer

Leave a small amount for surprise costs.

A buffer can prevent one small expense from ruining the plan.

What I Noticed After Splitting Income Clearly

Before I started splitting income clearly, payday felt random.

Money would come in, bills would go out, and I would try to guess what was safe to spend.

That guessing created stress.

Once I gave my income a clear order, budgeting became much easier to maintain.

This structure works best when it supports your monthly saving strategies.

Essentials came first. Future money had a place. Flexible spending felt safer because I knew what was already covered.

The biggest change was not that I became perfect with money.

It was that I stopped treating my income like one big pile.

Over time, that clarity became one of the small shifts that helped me save over $15,000 in a year. It did not happen from one perfect budget. It came from repeating simple money decisions that were easier to maintain.

Common Mistakes When Splitting Income

Using Percentages Too Rigidly

Percentages are guides, not rules.

If your life does not fit a perfect formula, adjust the formula.

Forgetting Irregular Expenses

Irregular expenses are easy to ignore until they appear.

Set aside something for repairs, gifts, annual fees, or medical costs if possible.

Saving Only What Is Left Over

If savings only happen at the end, they may not happen at all.

Treat future money as part of the split from the beginning.

Spending Before Bills Are Covered

Flexible spending should not come before essentials.

Cover required payments first so you do not accidentally spend money that already had a purpose.

Not Leaving a Buffer

A budget without a buffer is fragile.

Even a small cushion can make your income split feel more realistic.

How This Fits Into Your Budgeting System

This article focuses on income allocation only.

If you need realistic category numbers, use a monthly budget example for single person.

If you are unsure what counts as essentials, flexible spending, or future money, a simple budget categories list can help.

If you want a stricter method, zero-based budgeting for beginners explains how to assign money more precisely.

And if monthly planning feels too far away, a weekly budget plan for beginners can help you manage your money in shorter time frames.

Income splitting gives your money direction.

The other systems help you refine the details.

FAQ

How should I split my income for budgeting?

You should split your income by priority: essentials first, future money second, flexible spending third, and a small buffer last. This helps you cover what matters most before using money for wants or personal spending.

What is the best way to divide income?

The best way to divide income is to start with your real bills and basic needs, then set aside money for savings, debt, or future expenses, and finally decide what is safe for flexible spending. Percentages can help, but priorities matter more.

Should I use percentages to split income?

You can use percentages to split income, but they should be flexible. Many people use rough guides like 50–60% for essentials, but your real income, location, bills, and goals should decide the final split.

How much income should go to savings?

How much income should go to savings depends on your situation. If money is tight, even 5–10% can be a good start. The most important thing is to make savings visible in your income split instead of waiting for leftovers.

What should I do if my income is too low to split?

If your income is too low to split comfortably, prioritize essentials first. Then keep future money small but visible, reduce flexible spending temporarily, and keep a small buffer. The goal is stability, not a perfect percentage.

Conclusion

Splitting income for budgeting does not need to be complicated.

You need a clear order.

Essentials first.

Future money next.

Flexible spending after that.

A small buffer if possible.

Start with your real income and adjust as life changes.

You do not need the perfect percentage.

You need a clear order for your money.

The ideas shared here come from real-life experience and practical habits that actually work.

→ Read more about Jeffi

- How to Split Bills Between Paychecks Without Overloading One Check - August 9, 2026

- Subscription Audit Checklist: Find and Review Every Recurring Charge - August 9, 2026

- How to Budget for Subscriptions Without Surprise Renewals - August 7, 2026