If you’ve ever looked at your bank account and thought, “I don’t know where my money went,” zero-based budgeting might finally make budgeting feel clearer.

A normal budget can feel vague.

You write down a few categories. You guess how much you might spend. Then the month happens, and somehow the numbers don’t match real life.

That is where many beginners get stuck.

Zero-based budgeting gives your money a clearer direction before it disappears. But the name can sound intimidating, especially if you’ve never tried it before.

The good news is simple:

Zero-based budgeting does not mean you end the month with zero money.

It means every dollar has a job.

That job might be rent, groceries, savings, debt payments, emergency fund, or even fun money. The goal is not to punish yourself. The goal is to know where your money is going before it gets spent randomly.

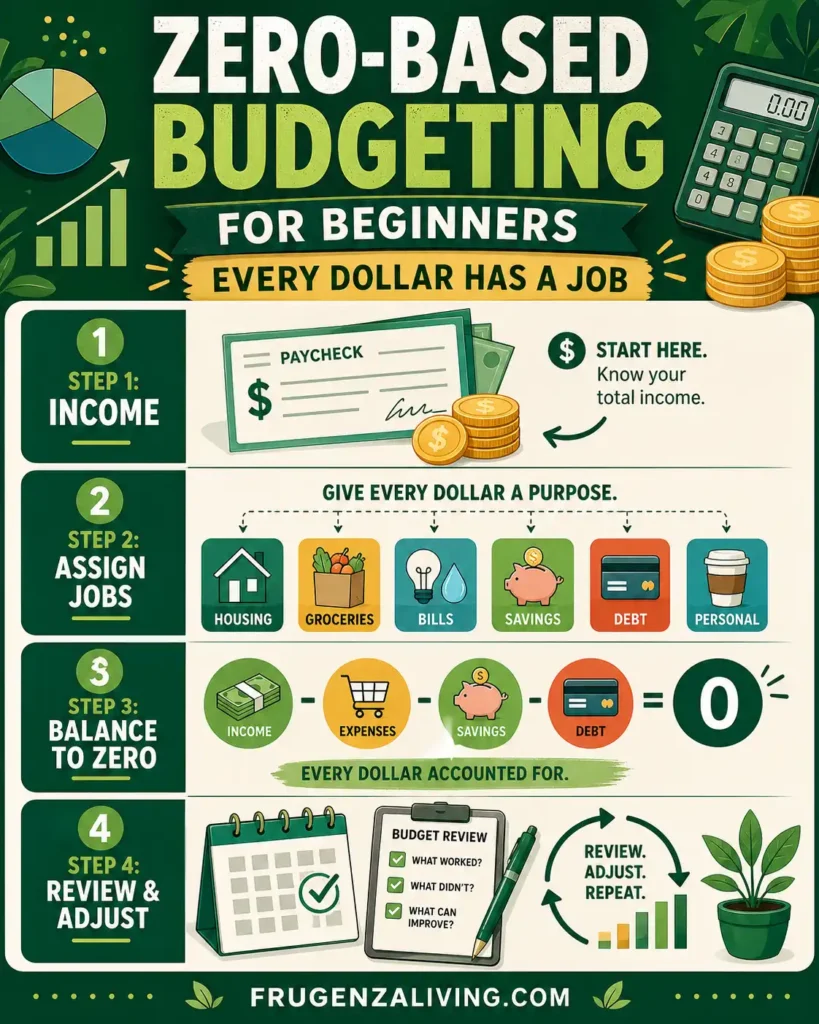

What Is Zero-Based Budgeting for Beginners?

Zero-based budgeting for beginners is a budgeting method where you assign every dollar of your income a specific job before the month starts. Your income minus planned expenses, savings, and debt payments equals zero. This does not mean spending everything. It means every dollar has a purpose.

Zero-based budgeting is one of several budgeting methods you can use depending on your needs.

Key Takeaways

- Zero does not mean you are broke

- Every dollar gets a clear purpose

- Savings count as a budget category

- Beginners should start with simple categories first

Zero-Based Budgeting Is About Clarity, Not Restriction

The word “zero” is what confuses many people.

It sounds like you are supposed to spend everything until nothing is left.

That is not the point.

In zero-based budgeting, “zero” means your money is fully assigned. You are not leaving random dollars floating around without a purpose.

For example, if you have $200 left after bills, that money still needs a job.

It could go to:

- savings

- debt payment

- groceries

- next month’s rent

- emergency fund

- personal spending

Even fun money counts.

That is what makes zero-based budgeting different from a strict budget. It does not say you can never enjoy your money. It simply asks you to decide where your money should go before it disappears.

A good zero-based budget should feel clear, not punishing.

How Zero-Based Budgeting Works

The basic formula is simple:

Income – Planned Spending – Savings – Debt Payments = Zero

That does not mean you spend all your money.

It means you assign all your money.

Here is a simple example:

| Category | Amount |

|---|---|

| Income | $2,500 |

| Rent | $900 |

| Groceries | $300 |

| Bills | $250 |

| Transportation | $150 |

| Personal Spending | $200 |

| Savings | $400 |

| Debt / Irregular Expenses | $300 |

| Remaining | $0 |

Notice something important.

The savings category is included in the budget.

That means the money is not “leftover.” It already has a job.

This is the mindset shift that makes the zero-based budgeting method useful for beginners.

If you’re new, it’s helpful to start with simple budgeting for beginners before using advanced methods.

Zero-Based Budgeting Example for Beginners

Here is a beginner zero-based budget example that focuses on assigning jobs to dollars.

This is not meant to be a perfect budget. It is just a simple way to see how the method works.

| Budget Category | Planned Amount | Purpose |

|---|---|---|

| Rent / Housing | $900 | Keep housing covered first |

| Groceries | $300 | Plan food spending before shopping |

| Utilities | $150 | Cover electricity, water, or gas |

| Transportation | $150 | Pay for fuel, transit, or basic travel |

| Insurance / Bills | $250 | Handle fixed monthly payments |

| Personal Spending | $200 | Allow flexible spending without guilt |

| Savings | $300 | Build future stability |

| Debt Payment | $200 | Reduce balances intentionally |

| Irregular Expenses | $50 | Prepare for non-monthly costs |

The point is not to copy these numbers exactly.

The point is to understand the role of each dollar.

If you need realistic category amounts, a monthly budget example for single person can help you compare common spending ranges. But for this article, the focus is the method: giving every dollar a job.

This method works best when combined with realistic ways to save money every month.

How to Start Zero-Based Budgeting Step by Step

You do not need a perfect spreadsheet to start.

You just need a clear process.

1. Write Down Your Monthly Take-Home Income

Start with the money you actually receive after taxes.

This might be your salary, freelance income, side income, or any regular payment.

If your income changes, use a conservative estimate. It is better to plan with a lower number than to build a budget around money you might not receive.

2. List Your Fixed Expenses

Fixed expenses are the bills that usually stay the same.

Examples include:

- rent

- insurance

- phone bill

- internet

- loan payments

These are usually the easiest to enter first because they are predictable.

This method works best when you clearly define your budget categories first.

3. Add Flexible Expenses

Flexible expenses change from month to month.

Examples include:

- groceries

- gas

- dining out

- personal spending

- household items

Beginners often struggle here because these numbers are not always obvious. If you are unsure, start with your best estimate and adjust later.

4. Add Savings as a Category

This is one of the most important parts.

In zero-based budgeting, savings is not what happens after everything else.

Savings gets a job from the beginning.

You can create categories like:

- emergency fund

- monthly savings

- future bills

- vacation fund

- car repair fund

This is also where realistic ways to save money every month can support your zero-based budget if your goal is consistent saving.

5. Add Irregular Expenses

Irregular expenses are the costs that do not happen every month but still show up eventually.

Examples:

- car maintenance

- gifts

- medical costs

- yearly fees

- repairs

- school costs

- clothing replacement

If you forget this category, your zero-based budget may look good on paper but break in real life.

6. Adjust Until Every Dollar Has a Job

Now compare income with planned spending.

If you have money left, assign it.

If you are over budget, reduce or adjust a category.

The goal is to reach zero on paper:

Income – planned categories = zero.

Again, this does not mean zero dollars in your bank account. It means zero unassigned dollars.

7. Review and Repeat Monthly

Your first zero-based budget will not be perfect.

That is normal.

Review it during the month, adjust when needed, and repeat next month.

The method gets easier after you see your real patterns.

To make it easier, you can follow a simple monthly budget for one person.

The “Every Dollar Has a Job” Method

The heart of zero-based budgeting is simple:

Every dollar needs a job.

A bill is a job.

Groceries are a job.

Savings are a job.

Fun money is a job.

Even a buffer is a job.

Instead of saying, “I have $300 left,” you decide what that $300 is supposed to do.

Maybe $150 goes to savings, $75 goes to groceries, $50 goes to personal spending, and $25 goes toward next month’s bills.

That is the difference.

The money is no longer waiting to be accidentally spent. It already has a direction.

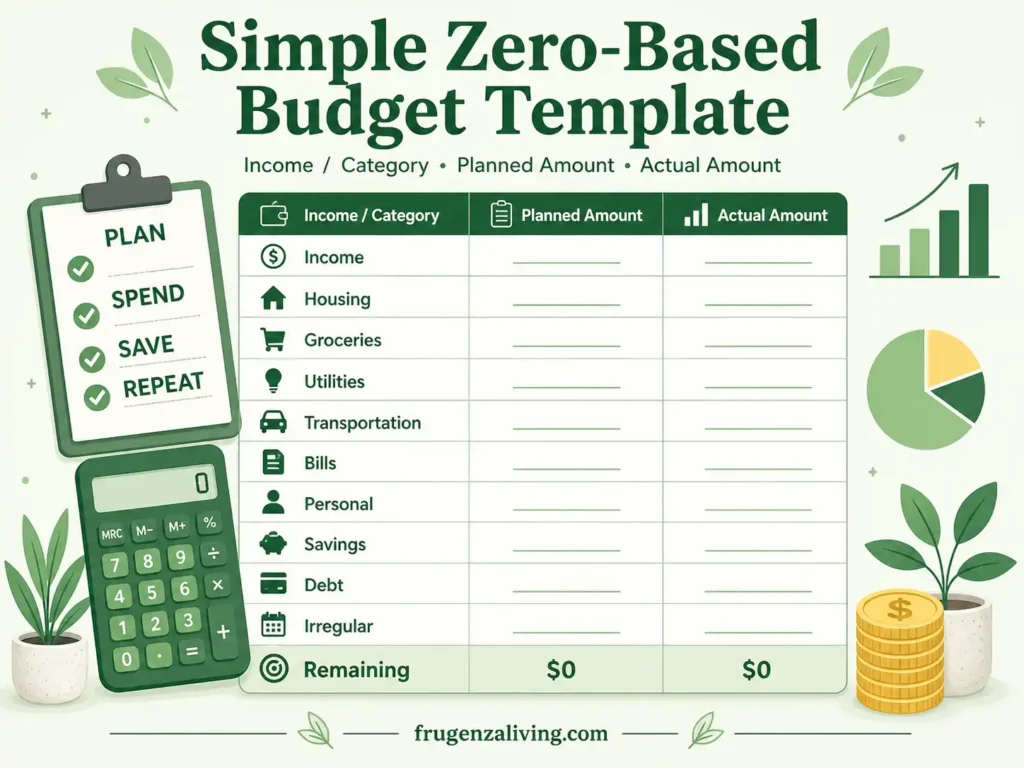

A Simple Zero-Based Budget Template

Here is a clean zero-based budgeting template you can copy or recreate.

| Income / Category | Planned Amount | Actual Amount |

|---|---|---|

| Income | ||

| Housing | ||

| Groceries | ||

| Utilities | ||

| Transportation | ||

| Bills | ||

| Personal | ||

| Savings | ||

| Debt | ||

| Irregular | ||

| Remaining | $0 |

Keep the template simple at first.

Too many categories can make zero-based budgeting feel harder than it needs to be.

If you do not know your actual spending yet, learning how to track expenses easily can help you fill in the “actual amount” column more accurately.

What I Noticed After Trying Zero-Based Budgeting

When I first tried zero-based budgeting, I expected it to feel strict.

But the opposite happened.

It made my money feel less vague.

Before, I would see money in my account and assume I had room to spend. Then later, a bill or unexpected cost would show up and make the month feel tight.

With a zero-based budget, I started giving money a direction earlier.

Spending decisions became clearer because I knew what each dollar was already supposed to do.

I was not perfect at first. Some categories were too low. Some expenses surprised me. I had to adjust more than once.

But the biggest change was not that I became perfect with money.

It was that every dollar had a direction before I could accidentally spend it.

Over time, using simple budgeting systems like this became one of the foundations that helped me save over $15,000 in a year. Not from one perfect spreadsheet, but from repeating clearer money decisions month after month.

Common Beginner Mistakes With Zero-Based Budgeting

Zero-based budgeting is simple, but beginners can still make it harder than necessary.

Thinking Zero Means No Money Left

This is the most common misunderstanding.

Zero-based budgeting does not mean your bank account should hit zero.

It means your income minus assigned categories equals zero on paper.

Forgetting Savings

Savings must be included as a category.

If you only save what is left over, there may not be much left.

Forgetting Irregular Expenses

Many beginners budget for monthly bills but forget non-monthly costs.

Then car repairs, annual fees, gifts, or medical expenses feel like emergencies.

Making Too Many Categories

A detailed budget sounds helpful, but too many categories can become exhausting.

Start simple.

You can always add more categories later.

Being Too Strict

If the budget feels like punishment, you probably will not stick with it.

Include personal spending and fun money if possible. A realistic budget is easier to repeat.

Not Adjusting During the Month

A zero-based budget is not frozen.

If groceries cost more than expected, adjust another category.

The goal is clarity, not perfection.

Who Should Use Zero-Based Budgeting?

Zero-based budgeting can work well for people who want more clarity.

It may be helpful if:

- you often wonder where your money went

- you want a clear plan before the month starts

- your income is fairly steady

- you like knowing exactly what each dollar is for

- you want savings and debt payments to be intentional

But it may need adjustment if:

- your income changes a lot

- your budget is extremely tight

- you dislike detailed planning

- you get overwhelmed by categories

If you have irregular income, you can still use the method, but you may need to budget based on your lowest expected income or update your numbers more often.

The zero-based budget is flexible enough to adjust, but it does require attention.

How to Use Zero-Based Budgeting When Your Income Changes Every Month

Zero-based budgeting works cleanest when your income is predictable.

But many people — freelancers, part-time workers, those with side income, or anyone who earns commission — do not have a fixed number to plan around each month.

The good news is that the method still works. It just needs one adjustment.

Use your lowest realistic income as your base.

Instead of budgeting from what you hope to earn, build your zero-based budget around the lowest amount you can reasonably expect. If your monthly income has ranged from $1,800 to $2,800 over the past few months, build your categories around $1,800.

This does the important thing: it keeps your fixed commitments — rent, bills, debt — covered even in a slow month.

Then, when income comes in higher than your base, you already have a decision ready.

This is where a simple rule helps.

Before the extra money lands in your account, assign it a job in advance.

You can call this your income tier rule. It works like this:

If income reaches the base amount, the regular budget runs as planned.

If income exceeds the base by a small amount — say, $200 to $400 — that extra goes directly to savings or an irregular expense category.

If income exceeds the base by a larger amount, split the excess between savings, debt, and a small discretionary category so the extra does not quietly disappear into daily spending.

The reason this matters is not just practical. It is psychological.

When irregular income arrives without an assigned job, it tends to get absorbed into spending without being noticed. A tier rule gives extra income a destination before the decision needs to be made under pressure.

The first month using this approach will not be exact. That is fine. The goal is not a perfect number. The goal is a budget that does not collapse the moment your income shifts by a few hundred dollars.

Zero-Based Budgeting vs Traditional Budgeting

Here is a simple comparison:

| Budget Type | How It Works | Best For |

|---|---|---|

| Traditional Budget | Sets general spending limits for categories | People who want a simple overview |

| Zero-Based Budget | Assigns every dollar a specific job until income minus categories equals zero | People who want detailed clarity |

| Simple Monthly Budget | Divides income into broad groups like essentials, lifestyle, and savings | Beginners who want fewer categories |

A traditional budget can be easier to start.

A zero-based budget gives more control.

A simple monthly budget may feel less detailed.

The best choice depends on how much structure you want.

How to Make Zero-Based Budgeting Easier

Zero-based budgeting does not need to be complicated.

Start with fewer categories.

Use rounded numbers.

Review once a week instead of every day.

Leave a small buffer if your income allows it.

Adjust without guilt when real life changes the numbers.

One helpful beginner rule is this:

Do not try to make your first zero-based budget perfect.

Make it usable.

You can improve it next month.

If impulse purchases keep breaking your plan, it may help to work on how to control spending habits alongside your budget. A budget gives money a direction, but spending habits help protect that direction.

How This Fits Into Your Budgeting System

Zero-based budgeting is one method inside a bigger money system.

If you need realistic category numbers, start with a monthly budget example for single person.

If you do not know where your money currently goes, use a simple expense tracking method first.

If impulse purchases keep causing problems, work on spending habits.

If your main goal is saving, connect your categories to a realistic monthly saving plan.

The zero-based budgeting method works best when it helps you make clearer decisions, not when it becomes another stressful rule.

FAQ

What is zero-based budgeting in simple terms?

Zero-based budgeting means giving every dollar of your income a specific job before the month starts. Your income minus planned spending, savings, and debt payments should equal zero on paper. It does not mean spending everything or having no money left.

Is zero-based budgeting good for beginners?

Zero-based budgeting can be good for beginners because it makes money decisions clearer. It helps you see where every dollar should go. Beginners should start with simple categories first so the method does not feel overwhelming.

Does zero-based budgeting mean I spend all my money?

No, zero-based budgeting does not mean you spend all your money. Savings, debt payments, emergency funds, and future expenses all count as jobs for your money. The goal is to assign every dollar, not waste every dollar.

How do I start a zero-based budget?

Start a zero-based budget by writing down your take-home income, listing fixed and flexible expenses, adding savings and irregular expenses, then adjusting until every dollar has a purpose. Review your budget during the month and adjust when needed.

What is the biggest mistake beginners make with zero-based budgeting?

The biggest mistake beginners make with zero-based budgeting is thinking “zero” means having no money left. Another common mistake is forgetting to include savings and irregular expenses as planned categories, which can make the budget feel unrealistic.

Conclusion

Zero-based budgeting does not need to feel scary.

You do not need a perfect spreadsheet.

You do not need to control every tiny purchase.

You just need to give your money direction before the month happens.

Start simple. Use broad categories. Adjust as real life changes.

Because zero-based budgeting is not about controlling every penny.

It is about knowing where your money is going before it disappears.

The ideas shared here come from real-life experience and practical habits that actually work.

→ Read more about Jeffi

- How to Split Bills Between Paychecks Without Overloading One Check - August 9, 2026

- Subscription Audit Checklist: Find and Review Every Recurring Charge - August 9, 2026

- How to Budget for Subscriptions Without Surprise Renewals - August 7, 2026