The 52-week money challenge sounds easy at first.

Save $1, then $2, then $3.

But when income is low, the later weeks can feel intimidating because $40 or $50 may already be grocery money, gas money, or part of a bill.

That is why the 52 week money challenge low income version needs to be flexible.

This article is not about shame, pressure, or forcing yourself to save $1,378 if that number does not fit your life right now.

It is about building a version of the 52-week challenge that protects your essentials, gives you small wins, and helps you create a little breathing room.

Can the 52-Week Money Challenge Work on Low Income?

Yes, the 52-week money challenge can work on low income, but only if you modify it.

The classic version may be too aggressive for someone living paycheck to paycheck or dealing with irregular income. That does not mean you cannot save. It means your version needs smaller weekly amounts, flexible deposits, a skip-week rule, or a different order.

If you live on paycheck-to-paycheck income, a low-pressure savings challenge may work better than a strict printable chart.

A 52 week money challenge low income plan should help you build consistency, not make rent, groceries, transportation, medicine, or minimum debt payments harder.

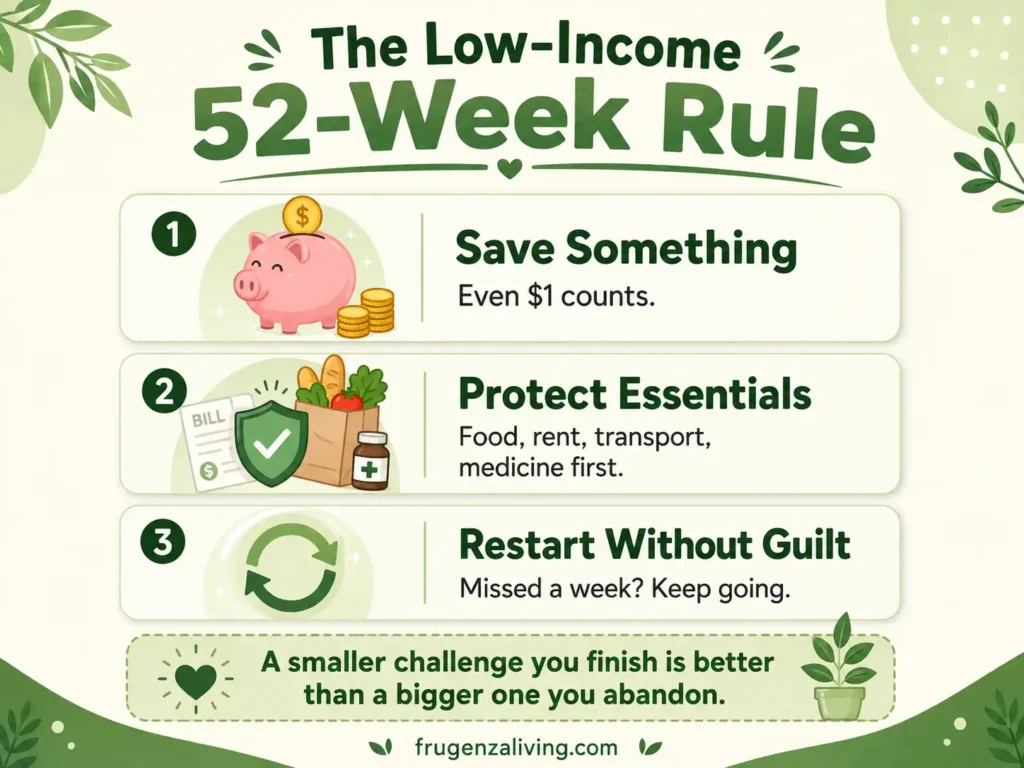

A smaller version you finish is better than a bigger version you abandon.

How the Classic 52-Week Money Challenge Works

The classic 52-week money challenge is simple.

You save:

- Week 1: $1

- Week 2: $2

- Week 3: $3

- Continue until Week 52: $52

If you complete the full version, you save $1,378 in one year.

That number can feel motivating, and the classic 52-week money challenge can work well for people with enough weekly breathing room.

But the later weeks are the hardest part. Saving $45, $48, or $52 in one week may not be realistic if your income is low or your bills change often.

So instead of treating the classic version as the only correct version, treat it as a starting idea.

Then adjust it to fit your real budget.

The Low-Income 52-Week Rule

Use this rule:

Save something. Protect essentials. Restart without guilt.

That is the heart of a realistic low income savings challenge.

A challenge should not make basic needs harder to cover. If saving for the challenge makes groceries, rent, transportation, medicine, utilities, or minimum debt payments harder, lower the amount.

Saving $1 is still saving.

Pausing for a hard week is still better than quitting completely.

Restarting without guilt is part of the system, not a failure.

The 52-week challenge becomes easier when you treat it as a weekly saving routine instead of a big yearly goal.

When This Challenge May Not Be the Right Move Yet

This challenge may not be the right move if saving even $1 makes food, rent, medicine, transportation, utilities, or minimum debt payments harder.

In that case, your first goal may be stability, not a savings challenge.

You can still track spending, look for one small money leak, or wait until your next stable paycheck before starting.

There is no shame in choosing safety first.

A challenge should support your life, not make it harder.

If you are completely new, you may want to start with a money saving challenge for beginners before trying a full 52-week version.

Choose Your Low-Income 52-Week Challenge Version

Pick the version that fits your current life, not the one that looks most impressive online.

Low-Income Friendly Guide

Choose Your 52-Week Money Challenge Version

Pick the version that protects your essentials and still helps you build a saving habit.

Helpful rule:

A smaller 52-week challenge you actually finish is better than a bigger challenge you abandon after a few weeks.

This layout makes the challenge easier to choose because you can compare pressure, total savings, and who each version fits best.

For low-income saving, that matters more than chasing the biggest number.

Try the Reverse 52-Week Challenge If Later Weeks Feel Too Hard

A reverse 52-week money challenge usually starts with the bigger amount first and gets easier later.

For example, the classic reverse version would start at $52, then $51, then $50.

But if income is low, do not force $52 in week 1.

Instead, use a modified reverse version.

Start with your highest comfortable amount, then lower it slowly.

For example:

- Week 1: $10

- Week 2: $9

- Week 3: $8

Then repeat or adjust.

This can work well if you have a slightly better week, a bonus, a refund, or extra cash early in the month.

The point is not to follow a perfect chart.

The point is to save in a way that still lets you pay for real life.

A beginner no-spend week can help you build confidence before trying a longer challenge.

Use the Skip-Week Rule Without Quitting

If a week is too tight, skip the deposit and continue next week.

Do not double the next deposit unless it feels comfortable.

That kind of catch-up pressure can make a low income money saving challenge harder than it needs to be.

Instead, choose one of these options:

- save $1 instead

- pause one week

- restart next week

- switch to the $1 version

- move the missed deposit to the end

Skipping one week does not erase your progress.

Quitting completely is the real risk.

A no shame savings challenge gives you permission to continue without turning one hard week into a failed year.

The hardest part is not starting the challenge, but learning how to stay consistent with with a budget for the full year.

How to Do the Challenge With Irregular Income

If your income changes from week to week, fixed weekly targets may not work well.

That is common for freelancers, part-time workers, gig workers, tipped workers, seasonal workers, or anyone with unpredictable hours.

Use rules that match irregular income:

- save more in better weeks

- save $1 in tight weeks

- skip only if essentials are at risk

- track average progress, not perfection

- review every payday instead of every Monday

If weekly saving feels awkward, make this a payday challenge instead.

Save a small amount every time money comes in, even if the amount changes.

This turns the challenge into a flexible weekly savings challenge low income readers can actually use.

If you get paid on different days, tie the challenge to payday instead of the calendar.

That makes it more realistic.

Turn It Into a Small Emergency Fund

The challenge works better when the money has a purpose.

For low-income readers, one useful goal is a small emergency fund.

Start with:

- $100 first

- then $250

- then $500

You do not need to build a huge fund immediately.

Even a small low income emergency fund can help with surprise expenses, small repairs, bills, medicine, or transportation problems.

If you want the challenge to support building an emergency fund, think of it as money for unplanned expenses, not extra spending money.

A $5 weekly challenge saves $260 in a year. That may not sound huge, but it can still create more breathing room than having nothing set aside.

Use a Simple Tracker

A tracker keeps progress visible.

It also makes small amounts feel real.

Use whatever is easiest:

- printable 52-week challenge

- notes app

- spreadsheet

- calendar

- savings jar

- separate savings account

- digital savings challenge

The tracker should reduce stress, not create pressure.

If a printable chart motivates you, use one.

If seeing missed boxes makes you feel discouraged, use a simple note or savings account balance instead.

The best tracker is the one that keeps you going.

My Simple Rule for Saving on Low Income

I stopped treating saving as all-or-nothing.

I started using small repeatable amounts.

That shift mattered.

Instead of waiting until I had “extra money,” I looked for tiny amounts I could save without hurting essentials. I checked my money once a week, reduced small money leaks, and gave myself permission to restart when things did not go perfectly.

Small savings challenges, weekly check-ins, and reducing money leaks became some of the habits that helped me save over $15,000 in a year.

Your numbers may look different, but a low-pressure challenge can still help you build confidence with money.

Saving on a low income is not about pretending things are easy.

It is about making the habit small enough to survive real life.

How This Fits Into Your Saving Money System

A low-income 52-week challenge works best when it connects with a larger saving system.

If you want more beginner-friendly options, money saving challenge for beginners can help you compare simple savings challenges.

If you need a weekly rhythm, how to save money weekly can help you create a repeatable habit.

If spending leaks keep eating your progress, how to control daily expenses effectively can help you spot small drains.

If your money feels disorganized, a simple money management plan for beginners can help you understand where your income is going.

FAQ

Can I do the 52-week money challenge on low income?

Yes, you can do the 52-week money challenge on low income if you modify it. Try a $1 weekly challenge, $2 weekly challenge, $5 weekly challenge, flexible weekly version, or modified reverse challenge instead of forcing the classic $1,378 version.

How much can I save with a low-income 52-week challenge?

You can save different amounts depending on your version. Saving $1 per week gives you $52 in a year. Saving $2 per week gives you $104. Saving $5 per week gives you $260. A flexible version can save more or less depending on your income.

What is the easiest 52-week savings challenge?

The easiest 52-week savings challenge is the $1 weekly challenge. You save $1 each week for 52 weeks, ending with $52. It is low pressure and useful if you are starting from zero.

What if I miss a week in the 52-week challenge?

If you miss a week, do not quit. Save $1 instead, pause for the week, restart next week, switch to a smaller version, or move the missed deposit to the end of the challenge.

Is the reverse 52-week challenge better for low income?

The reverse 52-week challenge can help if you have more money available earlier in the year, but the classic reverse version may still be too aggressive. A modified reverse challenge with smaller amounts is usually better for low-income budgets.

What is the best 52-week money challenge for paycheck-to-paycheck income?

The best version is usually the $1 weekly challenge, $2 weekly challenge, or flexible weekly challenge. These versions let you save small amounts without forcing a large deposit during expensive weeks.

Where should I keep the money during the challenge?

Keep the money somewhere separate from everyday spending, such as a savings account, cash envelope, savings jar, or digital savings account. The goal is to make the money visible but not too easy to spend casually.

Can I do a 52-week challenge with irregular income?

Yes. If your income is irregular, use a flexible version. Save more in better weeks, save $1 in tight weeks, skip only when essentials are at risk, and review progress every payday instead of every Monday.

Final Thought: A Smaller Challenge You Finish Is Still a Win

The 52-week money challenge does not have to be about saving $1,378.

If your income is low, your version can be smaller, slower, and more flexible.

Saving $52, $104, $260, or any amount you can keep is still progress.

The goal is not to impress anyone.

The goal is to build trust with yourself and create breathing room.

This article is for educational purposes only and is not professional financial advice.

The ideas shared here come from real-life experience and practical habits that actually work.

→ Read more about Jeffi

- Annual Expenses Checklist With a Fillable Yearly Planner - July 1, 2026

- Monthly Bills Checklist for Beginners: Track Every Payment Clearly - June 29, 2026

- How Much Should You Save Each Week? Calculate Your Ideal Target - June 28, 2026