You get paid, feel a little relieved, and then life starts taking pieces of that money.

Rent comes out. Groceries cost more than expected. A subscription renews. You grab food because the week is busy. A few small purchases feel harmless. Then the end of the month arrives, and you are not exactly sure where the money went.

That is why having a simple money management plan for beginners matters.

You do not need a perfect spreadsheet, a complicated app, or a strict financial personality. You need a repeatable routine for what happens when money comes in, where it needs to go, and how often you check it.

Money management is not about being perfect with every dollar. It is about making your money less confusing.

What Is a Simple Money Management Plan for Beginners?

A simple money management plan for beginners is a repeatable system for organizing income, bills, flexible spending, savings, debt, and goals.

It helps you know what must be paid first, how much you can spend, and what money should go toward your future before the month gets busy.

At the beginner level, the goal is not to optimize every tiny detail. The goal is to know what money is coming in, what must be paid first, how much you can spend freely, and what amount can go toward your future.

If you are wondering how to manage money as a beginner, start with a system that tells your money where to go before spending starts to drift.

A good beginner money management plan usually includes:

- your real monthly income

- your bills and due dates

- a flexible spending limit

- a small savings habit

- a weekly money check-in

- a way to adjust without shame

If your money has felt messy for a while, this kind of plan gives you a starting point.

Budgeting vs. Money Management: What’s the Difference?

Budgeting and money management are connected, but they are not exactly the same.

A budget is the plan.

Money management is the routine that helps you actually use the plan.

For example, a budget might say you have $400 for groceries this month. Money management is checking how much you have already spent, planning meals around what is left, and noticing early if you are about to go over.

A budget can look nice on paper and still fail in real life if you never check it.

That is why beginners need more than a list of spending categories. You need a simple routine that works during a normal, busy week.

A simple plan works better when you already know the budgeting fundamentals behind it.

The 3-Bucket Money System

One of the easiest ways to organize your money is to use three basic buckets:

- Bills and essentials

- Flexible spending

- Future money

This keeps your money plan simple enough to understand without needing twenty categories from the beginning.

Once your income comes in, the next step is to divide your income properly across your main needs.

This 3-bucket system works because it answers the most important beginner question: what does this money need to do?

Step 1: Know Your Real Monthly Income

Start with your real monthly income.

That means after-tax income, not your salary before deductions.

If you earn a paycheck, look at the amount that actually lands in your account. If you have side income, freelance income, hourly work, or gig work, use a conservative number. Do not build your plan around the best month you hope to have.

If your income changes often, use the lowest realistic month or average your last three months of income.

Include:

- paycheck income

- side income

- freelance income

- benefits

- irregular income

- any reliable monthly support

Beginners often get into trouble when the plan is based on money that might arrive instead of money that usually arrives.

Your money management plan should start with what is real.

If you get paid every two weeks, your plan should help you manage biweekly money management plan clearly.

Step 2: List Your Bills Before You Plan Fun Spending

Before you decide what you can spend freely, list the bills that need to be paid first.

This includes fixed bills and essential expenses like:

- rent or mortgage

- utilities

- phone bill

- internet

- insurance

- minimum debt payments

- transportation

- groceries estimate

- subscriptions

- childcare or family costs if needed

If you have debt, include at least the minimum debt payment in this bucket before planning flexible spending. Extra debt payoff can come later, but the minimum payment should be treated like a bill.

Then create a simple bill calendar.

A bill calendar does not need to be fancy. You can use a notes app, a paper planner, Google Calendar, or a spreadsheet.

For example:

- Rent due on the 1st

- Phone bill due on the 8th

- Credit card minimum due on the 15th

- Insurance due on the 22nd

This reduces surprises.

If you are new to making a budget, the basic idea is to list your income, bills, and expenses clearly before the month begins.

A beginner money management plan becomes much easier when you know which bills are coming before they hit your account.

Step 3: Set a Flexible Spending Limit

Flexible spending is where money often disappears quietly.

This includes things like eating out, coffee, online shopping, entertainment, small Target or Amazon purchases, snacks, convenience items, and random extras.

The problem is not that these purchases are always bad. The problem is that they are easy to underestimate.

Instead of only setting a monthly number, try turning it into a weekly limit.

For example, if you can spend $300 on flexible spending this month, that is about $75 per week.

A weekly limit is easier to feel.

If you spend $60 by Wednesday, you know the rest of the week needs to be lighter. If you only check at the end of the month, it may be too late to adjust.

This is where money management becomes practical. You are not just hoping the budget works. You are checking while there is still time to change something.

Step 4: Pay Yourself First, Even If It’s Small

Pay yourself first means moving money toward savings, debt payoff, or a future goal before all the money gets absorbed by spending.

For beginners, this does not need to be dramatic.

It might be:

- $10 every payday

- $20 a week

- $50 a month

- a small automatic transfer after payday

The first goal can be a starter emergency fund. Even a small cushion can make life feel less stressful when something unexpected happens.

Do not worry about advanced investing if your basic money plan still feels messy. Investing can come later. First, build the habit of keeping some money for your future self.

The amount matters, but the habit matters too.

When you move money early, it has a better chance of staying there.

Step 5: Use a Weekly Money Reset

A beginner money plan often fails because it only gets checked once a month.

That is too long.

A weekly money reset gives you a quick way to stay aware without obsessing over every dollar.

Set aside 10 minutes once a week. During that time, check:

- your account balance

- bills due this week

- flexible spending left

- recent purchases

- savings progress

- anything that needs adjusting

You can do this every Sunday night, Monday morning, or payday evening. The exact day does not matter. The repeatable habit matters more.

A weekly reset helps you catch small problems before they become big ones.

If you overspent on food last week, you can make this week simpler. If a bill is coming soon, you can avoid spending money that already has a job.

This is how you start to control your money without needing a complicated system.

A Simple Payday Routine for Beginners

A money plan gets easier when payday has a routine.

When money arrives, give it an order before the week gets busy.

Use this simple payday routine:

- Cover bills due before your next payday.

- Move a small amount to savings first.

- Set your weekly flexible spending limit.

- Check upcoming due dates.

- Leave a small buffer if possible.

This routine matters because payday can make your account feel bigger than it really is.

If you get paid and immediately spend freely, bills and savings have to fight for whatever is left. But if you decide what the money needs to do first, it is less likely to disappear into random spending.

That is the heart of a simple money management plan: give your money a job before it quietly leaves.

A money management plan becomes easier to follow when you build a simple financial routine around it.

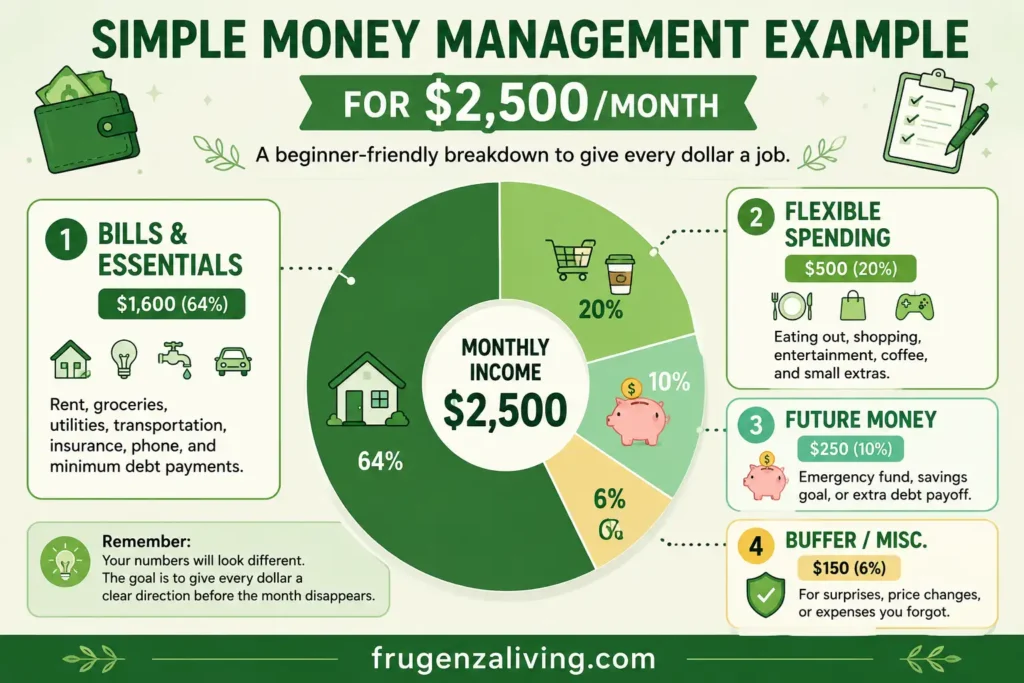

A Simple Money Management Example for $2,500/Month

Here is a simple example for someone earning $2,500 per month after tax.

This is only an example, not a rule.

The bills and essentials bucket might cover rent, groceries, utilities, phone, insurance, transportation, and minimum debt payments.

The flexible spending bucket covers eating out, coffee, shopping, entertainment, and extras.

The future money bucket can go toward an emergency fund, savings goal, or extra debt payment.

The buffer helps with small surprises, price changes, or things you forgot to plan for.

Your numbers may look very different depending on rent, debt, family size, income, and location. Someone living in a high-cost city may need more for essentials. Someone with roommates may have more room for savings.

The point is not to copy the example exactly.

The point is to give every dollar a basic direction before the month disappears.

It is hard to improve your finances if you do not understand where your money goes each month.

The 7-Day Beginner Money Setup

If managing money feels overwhelming, do not try to fix everything in one sitting.

Use a simple 7-day setup:

- Day 1: Write down your income. Use after-tax income. If your income changes, use a conservative number.

- Day 2: List your bills and due dates. Write every bill you can remember. Add due dates next to each one.

- Day 3: Check your last 30 days of spending. Look for food, shopping, subscriptions, transportation, and random extras.

- Day 4: Create your 3 buckets. Separate bills and essentials, flexible spending, and future money.

- Day 5: Set a weekly spending limit. Turn your flexible spending number into a weekly amount.

- Day 6: Move a small amount to savings. Even a small transfer helps build the habit.

- Day 7: Schedule your weekly money reset. Pick a day and time to check your money every week.

This setup gives you a basic money plan without making the process feel too heavy.

What If Your Income Is Irregular?

A simple budgeting plan for beginners can still work if your income changes.

You just need to be more careful with the starting number.

If your income is irregular, build your plan from your lowest realistic month instead of your highest month. Essentials come first. Flexible spending comes after bills. Future money can increase during better months.

You may also need a bill buffer.

A bill buffer is money set aside to help cover bills during lower-income weeks. If you are self-employed, you may also need to separate tax money before spending.

For irregular income, good months should not only feel like extra spending money. They should help prepare for lower months.

That one mindset shift can make inconsistent income less stressful.

What to Do When You Mess Up the Plan

You will not follow your money plan perfectly every month.

That is normal.

Maybe groceries cost more than expected. Maybe you overspent on eating out. Maybe a bill surprised you. Maybe savings did not happen.

Do not restart from zero.

Use this recovery loop:

Notice → Adjust → Protect next week → Continue

If you overspent on eating out, reduce flexible spending slightly next week. If a bill surprised you, add it to your bill calendar. If savings did not happen, lower the amount but keep the habit alive.

A messy week does not mean the plan failed.

It means the plan needs one small adjustment.

The goal is not perfection. The goal is returning to the routine.

My Simple Money Rule

I stopped trying to make my budget perfect.

Instead, I started asking one simple question every payday:

What needs to happen before I spend freely?

That question changed the order of my money.

Bills came first. A small savings transfer came early. Flexible spending got a weekly limit. And I checked my money regularly instead of avoiding it until something felt wrong.

This simple routine became one of the habits that helped me save over $15,000 in a year.

Your numbers may look different, but the habit of checking your money regularly can still make your finances feel less chaotic.

For me, the biggest shift was not having a perfect budget.

It was having a simple money routine I could repeat.

How This Fits Into Your Budgeting System

A simple money management plan is the foundation. Once that foundation feels clear, other budgeting habits become easier.

If you want a deeper breakdown of categories, a simple budget categories list can help you decide where each dollar belongs.

If you need a more detailed example, a monthly budget example for a single person can show what a realistic plan might look like.

If your biggest problem is not knowing where money goes, learning how to track expenses easily can support this plan.

If you want to build savings into your routine, a weekly saving system can help you protect money before spending takes over.

And if you are still learning the basics, basic budgeting tips can help you strengthen the system without making it complicated.

FAQ

What is a simple money management plan for beginners?

A simple money management plan for beginners is a basic system for organizing income, bills, flexible spending, savings, debt, and goals. It helps you decide what money needs to do before the month begins and gives you a routine for checking it regularly.

How do beginners start managing money?

Beginners can start managing money by writing down after-tax income, listing bills and due dates, setting a flexible spending limit, saving a small amount first, and doing a weekly money reset. The goal is to build awareness before trying to make the plan perfect.

What is the easiest budget plan for beginners?

The easiest budget plan for beginners is one that separates money into simple groups: bills and essentials, flexible spending, and future money. This keeps the plan clear without requiring too many categories at the start.

How much money should a beginner save each month?

A beginner should save an amount that is realistic enough to repeat. That might be $10, $20, $50, or a small percentage of income. The habit of saving consistently matters more at first than choosing a perfect amount.

How do I manage money if I live paycheck to paycheck?

If you live paycheck to paycheck, start by listing bills, due dates, and essential expenses first. Then set a small weekly spending limit and try to build even a tiny buffer. The first goal is to reduce surprises, not create a perfect budget overnight.

What are the basic money categories beginners need?

Beginners usually need a few basic money categories: housing, utilities, food, transportation, debt payments, insurance, flexible spending, savings, and emergency fund. You can add more categories later if needed.

How often should I check my budget?

Checking your budget once a week is a good starting point. A weekly money reset helps you see what bills are coming, how much flexible spending is left, and whether you need to adjust before the month ends.

Final Thought: Keep the Plan Simple Enough to Repeat

You do not need a perfect spreadsheet.

You do not need to track every penny forever.

You need a simple plan you can repeat when money comes in, when bills are due, and when spending starts to drift.

Start with your income. List your bills. Set a flexible spending limit. Move something toward your future. Check in once a week.

A simple money management plan works best when it is easy enough to use on a normal, busy week.

The ideas shared here come from real-life experience and practical habits that actually work.

→ Read more about Jeffi

- Annual Expenses Checklist With a Fillable Yearly Planner - July 1, 2026

- Monthly Bills Checklist for Beginners: Track Every Payment Clearly - June 29, 2026

- How Much Should You Save Each Week? Calculate Your Ideal Target - June 28, 2026