A monthly budget can look fine until a predictable expense shows up all at once.

A car repair. Holiday gifts. An annual subscription. School fees. Pet care. Insurance renewal. These expenses can feel like surprises, but many of them are not truly unexpected. They happen again and again. They just do not happen every month.

That is where sinking funds for beginners can help.

A sinking fund is a simple way to save a little each month for a specific future expense. Instead of letting a $600 car repair or $480 holiday budget hit your checking account at once, you prepare for it slowly.

This is general budgeting education, not professional financial advice. Adjust the examples based on your income, bills, debt, and personal situation.

Quick Answer: What Is a Sinking Fund?

A sinking fund is money you set aside little by little for a specific planned expense. Common sinking fund examples include car repairs, holidays, gifts, annual subscriptions, insurance, travel, medical costs, and home maintenance.

Sinking funds are different from emergency funds because they are used for planned or expected expenses, not urgent surprises.

When I started taking planned expenses more seriously, sinking funds became one of the small systems that helped me save over $15,000 in a year.

That number did not come from one trick. It came from many small systems working together, and sinking funds helped stop predictable costs from turning into budget emergencies.

Why Sinking Funds Matter More Than Beginners Think

Most people do not break their budget because of one coffee or one small purchase.

A lot of budgets break because of expenses that were easy to forget.

Annual subscriptions renew. Tires wear out. Birthdays come back. Holidays arrive. Pets need care. Kids need school supplies. Homes need maintenance. These costs may not happen every month, but they still belong in your budget.

Most sinking funds are not for emergencies. They are for expenses your future self can already see coming.

That sentence matters because it changes the way you look at budgeting. A holiday budget may feel stressful in December, but December was always coming.

A pet bill may feel sudden when it happens, but pet care itself is not random. A car repair may feel frustrating, but cars usually need maintenance sooner or later.

In a planned expenses budget, sinking funds help you treat annual and irregular expenses as part of normal life instead of financial interruptions.

Once you understand the basics, the next step is choosing from a sinking fund categories list that matches your real expenses.

Sinking Fund vs Emergency Fund vs Savings Account

A sinking fund, emergency fund, and savings account are not the same thing.

A sinking fund is for a planned or expected expense. An emergency fund is for urgent and unexpected problems. A savings account is simply a place to store money. You can keep sinking funds inside a savings account, but the money still needs a clear label.

The mistake many beginners make is keeping all savings in one unlabeled pile. That makes it hard to know what the money is actually for.

Before creating sinking funds, it helps to understand your main budget categories so each future expense has a clear place.

The Beginner Sinking Fund Rule

A simple way to start is the P.L.A.N. Method.

- P — Pick the expense: Identify what you are saving for.

- L — List the due date: Know exactly when the money is needed.

- A — Assign a monthly amount: Divide the total by the months left.

- N — Name the fund clearly: Give it a specific label so you do not spend it accidentally.

A sinking fund without a name often turns into general savings you accidentally spend.

For example, “savings” is vague. “Car maintenance — $600 by December” is clear. “Holiday gifts — $480 by November” is clear. The more specific the fund, the easier it is to protect.

Your First 15-Minute Sinking Fund Setup

You do not need a perfect system to start.

Here is a simple setup you can do quickly:

- Pick three sinking funds.

- Write the target amount for each one.

- Write the due date or expected month.

- Divide the target by the months left.

- Create a clear label in your tracker, bank bucket, or savings note.

- Schedule the monthly transfer after payday.

This small setup is better than waiting until you have the perfect spreadsheet, the perfect app, or the perfect budget.

Step 1: Start With 3 Sinking Funds, Not 15

Many beginners search for sinking fund categories and find huge lists with 50 ideas.

That can be exciting, but it can also become overwhelming.

You do not need 15 sinking funds in your first month. Start with three categories that are most likely to disrupt your budget.

Choose:

- One annual bill

- One seasonal expense

- One maintenance or repair category

For example:

- Annual subscription

- Holidays or gifts

- Car maintenance

This starter setup is simple enough to manage. After 30–60 days, you can add more sinking funds if your budget can handle them.

The goal is not to prepare for every possible expense immediately. The goal is to stop the most predictable expenses from catching you off guard.

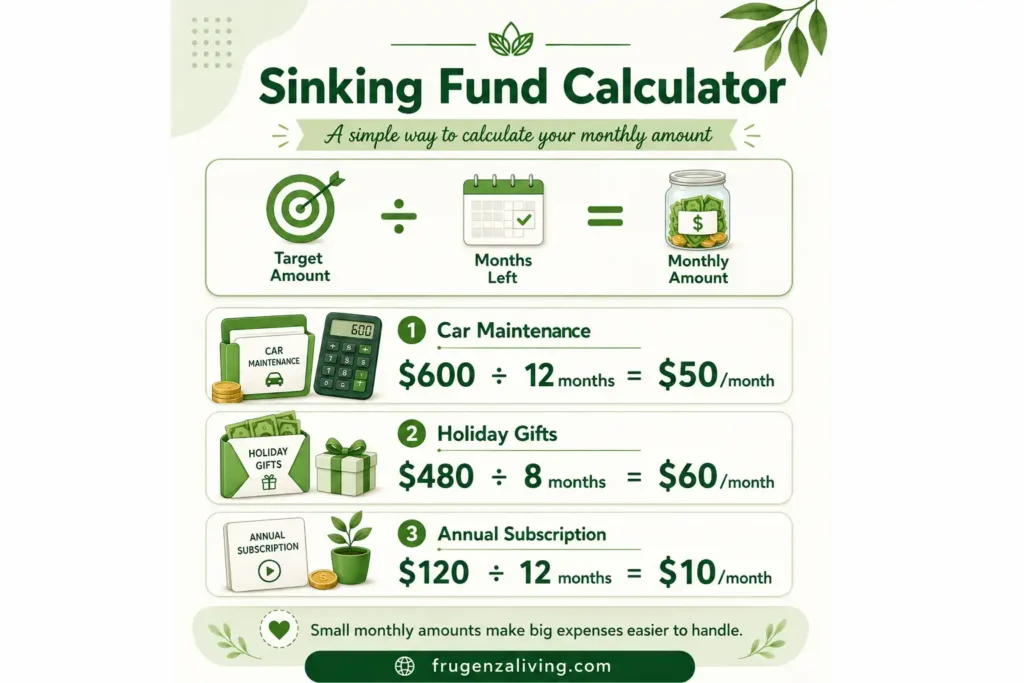

Step 2: Calculate Your Monthly Sinking Fund Amount

The sinking fund formula is simple:

Total needed ÷ months left = monthly sinking fund amount

For example:

- Car repairs target: $600

- Time left: 12 months

- Monthly amount: $50

Another example:

- Holiday gifts target: $480

- Time left: 8 months

- Monthly amount: $60

If the monthly sinking fund amount feels too high, do not quit. Adjust the plan. You can lower the target, extend the timeline, start with a smaller amount, or prioritize the expense that is due soonest.

A simple sinking fund tracker can help you see the target, due date, monthly amount, current balance, and withdrawals in one place.

This formula turns a future expense into a monthly decision.

Each payday, try to set money aside for future expenses before using the rest for flexible spending.

Step 3: Choose Sinking Fund Categories That Actually Matter

Not every possible category needs its own fund.

A beginner sinking fund budget should focus on the expenses that are predictable, large enough to hurt, and likely to happen again.

Useful sinking fund categories for beginners include:

- Car maintenance

- Holidays and gifts

- Annual subscriptions

- Insurance premiums

- Medical costs

- Pet care

- Home maintenance

- Clothing

- School expenses

- Travel

- Family events

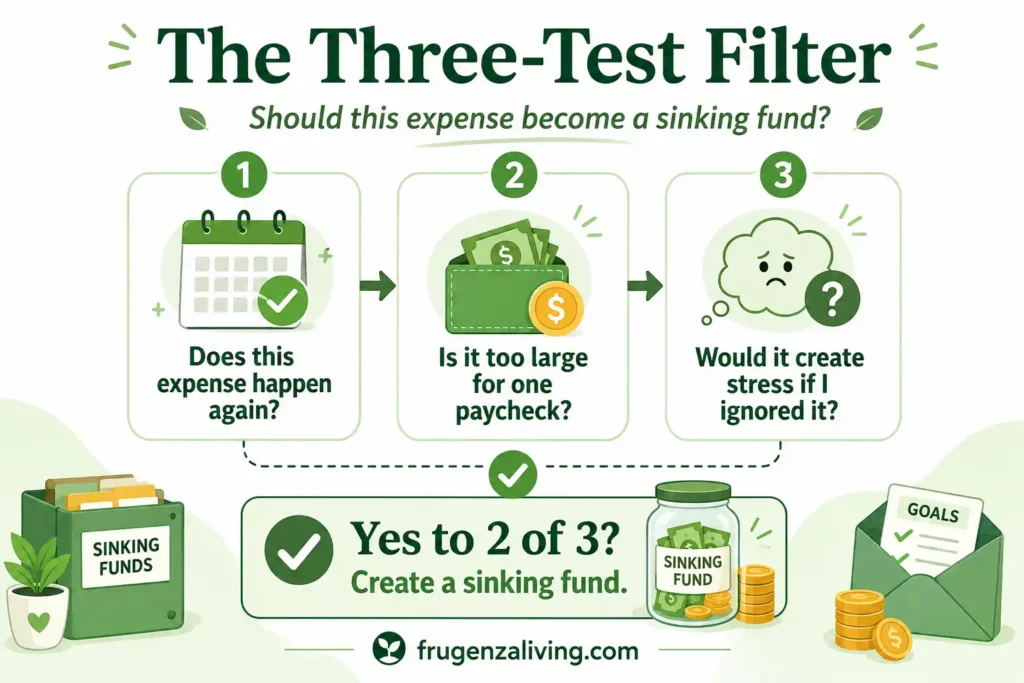

Use the Three-Test Filter before creating a new fund:

- Does this expense happen again?

- Is it too large for one paycheck?

- Would it create stress if I ignored it?

If the answer is yes to at least two of those questions, it probably deserves a sinking fund.

This keeps you from creating too many categories just because they sound useful.

If you budget by paycheck, a simple payday budget template makes sinking funds easier to repeat.

Step 4: Where Should You Keep Sinking Funds?

You do not need a separate bank account for every sinking fund.

You can keep sinking funds in:

- A separate savings account

- Bank buckets or savings pockets

- A spreadsheet tracker

- Digital envelopes

- Cash envelopes for short-term goals

The key is labeling. If your money sits in one account with no tracker, it is easy to forget which dollars belong to which goal..

A simple setup could be one savings account plus a tracker that shows:

- Car maintenance: $150

- Holiday gifts: $220

- Annual subscriptions: $60

- Pet care: $90

The bank account holds the money. The tracker gives the money a purpose.

Step 5: Fund Sinking Funds After Payday

Sinking funds should not depend only on leftover money.

If you wait until the end of the month, there may be nothing left to move. Instead, include sinking funds in your payday routine.

A simple order can look like this:

- Bills

- Basic needs

- Minimum debt payments

- Starter sinking funds

- Flexible spending

This does not mean sinking funds are more important than rent, food, or debt minimums. It means predictable future expenses deserve a place in the budget before flexible spending absorbs everything.

A monthly budget reset helps you check whether your sinking funds still match your upcoming expenses.

Step 6: What If You Cannot Fully Fund Every Sinking Fund?

You may not be able to fund every category perfectly.

That does not mean the system failed.

Use priority mode:

- Fund due-soon expenses first

- Reduce lower-urgency categories

- Stretch the deadline

- Lower the target temporarily

- Pause non-critical funds

For example, car insurance due in two months is more urgent than a vacation planned for next year. A medical bill due soon is more urgent than replacing furniture someday.

Sinking funds should make your budget calmer, not impossible. If the total monthly amount is too high, start smaller and protect the most urgent fund first.

Sinking Fund Example for Beginners

Here is a simple starter setup:

- Car maintenance: $50/month

- Holiday gifts: $40/month

- Annual subscription: $10/month

Total sinking funds: $100/month

This does not solve every future expense. But it helps protect your budget from three common problems: car costs, seasonal spending, and annual renewals.

A beginner sinking fund method should be useful before it is perfect. Once you can consistently save $100/month across three funds, you can add another category.

Common Sinking Fund Mistakes Beginners Make

Watch for these beginner mistakes:

- Starting with too many funds: Too many categories can make the system feel impossible.

- Saving without a name: Unlabeled savings are easier to spend accidentally.

- Ignoring due dates: A fund without a deadline is harder to calculate.

- Making the monthly amount unrealistic: The goal should fit your real budget.

- Using sinking funds for emergencies: Planned expenses and emergencies need different jobs.

- Not tracking withdrawals: If you use the fund, update the balance.

- Forgetting small annual bills: Annual subscriptions can quietly break a monthly budget.

My Simple Rule for Sinking Funds

One thing that helped me save over $15,000 in a year was learning that not every “surprise expense” deserved to surprise me.

For a long time, I treated things like car maintenance and holiday spending as if they came out of nowhere. They did not. I simply had no small fund waiting for them.

The sinking fund that changed the way I budgeted was a simple car maintenance fund. It was not dramatic. It was not a huge amount. But putting aside a small amount consistently meant that when a repair came up, I did not have to panic, drain another category, or feel like the whole month was ruined.

That is my simple rule for sinking funds:

If an expense has happened before and will probably happen again, start preparing before it returns.

This is why I prefer starting with three funds instead of trying to build a perfect system. A small sinking fund you actually use is better than a long list of categories you abandon after two weeks.

Final Thoughts: Make Future Expenses Less Surprising

Sinking funds for beginners work best when they start small.

You do not need a long list of categories or a complicated tracker. Start with three funds: one annual bill, one seasonal expense, and one maintenance category. Use the formula target amount ÷ months left to find your monthly sinking fund amount. Give every fund a clear name and review it during your monthly budget check-in.

A sinking fund budget does not make an expense disappear. It makes the expense easier to meet when it arrives.

FAQ

What are sinking funds for beginners?

Sinking funds for beginners are small savings categories for planned future expenses. They help you prepare for costs like car repairs, holidays, gifts, annual subscriptions, insurance, travel, or pet care before they hit your budget all at once.

How do you calculate a sinking fund?

To calculate a sinking fund, divide the total amount you need by the number of months left before the expense. For example, if you need $600 in 12 months, you would save $50 per month.

What are good sinking fund categories?

Good sinking fund categories include car maintenance, holidays, gifts, annual subscriptions, insurance premiums, medical costs, pet care, home maintenance, clothing, school expenses, and travel.

How many sinking funds should I start with?

Beginners should usually start with three sinking funds. Pick one annual bill, one seasonal expense, and one maintenance or repair category. You can add more funds later once the habit feels manageable.

Where should I keep my sinking funds?

You can keep sinking funds in a savings account, bank buckets, digital envelopes, cash envelopes, or a spreadsheet tracker. The most important part is labeling each fund clearly so the money does not blend into general savings.

What is the difference between a sinking fund and an emergency fund?

A sinking fund is for planned or expected expenses, while an emergency fund is for urgent and unexpected expenses. Car maintenance, holidays, and annual subscriptions are sinking fund examples. Job loss or an urgent repair may need an emergency fund.

The ideas shared here come from real-life experience and practical habits that actually work.

→ Read more about Jeffi

- How to Stop Buying Coffee Every Day Without Giving Up Coffee - July 25, 2026

- 8 Meals for One Without Leftovers—and How to Use the Rest - July 22, 2026

- 9 Cheap Dinners for One Person on a Budget That Feel Complete - July 20, 2026