A sinking fund categories list can be helpful, but it can also make budgeting feel harder than it needs to be.

You search for ideas, find 50 or 100 possible categories, and suddenly your budget feels behind before you even start. Car repairs, holidays, gifts, home maintenance, medical costs, travel, clothing, pets, school supplies, tech upgrades, furniture, insurance renewals—the list can grow fast.

The problem is not the list itself. The problem is trying to fund every category at once.

The best sinking fund categories are not always the most impressive ones. They are the ones that protect your real budget from real expenses that keep coming back.

This article is general budgeting education, not professional financial advice.

Quick Answer: What Are the Best Sinking Fund Categories?

The best sinking fund categories usually include car maintenance, annual bills, medical costs, holidays, gifts, pet care, home repairs, insurance premiums, travel, school expenses, clothing, and family events.

For beginners, a useful sinking fund categories list should start with 3–5 categories that are most likely to disrupt the monthly budget.

Quick Sinking Fund Categories List

Here is a quick sinking fund checklist you can use as a starting point.

Essential budget protection categories:

- Car maintenance

- Annual subscriptions

- Insurance premiums

- Medical and dental costs

- Home or renter repairs

- Pet medical care

- Taxes or license renewals

Seasonal and life rhythm categories:

- Holidays

- Birthday gifts

- School expenses

- Clothing and shoes

- Family events

- Seasonal utilities

- Guests or hosting

Lifestyle and future planning categories:

- Travel

- Phone replacement

- Appliance replacement

- Furniture

- Moving costs

- Hobbies

- Courses or learning

Before choosing categories, it helps to understand sinking funds for beginners so you know why each fund matters.

This is not a list you need to use all at once. Treat it as a menu, not a command. A good sinking fund checklist works best when you choose categories by priority instead of copying every idea immediately.

Why a Long Sinking Fund List Can Hurt Your Budget

A long list of sinking fund ideas can feel productive.

But for beginners, it can also create pressure.

If you make too many categories too soon, your money gets spread thin. You may end up putting $3 here, $5 there, and $7 somewhere else without feeling real progress anywhere. Then the system starts to feel messy, and you stop using it.

A useful sinking fund list should help you choose, not make you feel behind.

That is why I prefer sorting categories by priority instead of copying every category from a printable list. Some categories protect your budget from predictable damage. Some make life smoother. Others are great goals, but they should not compete with urgent expenses.

For another perspective, Empower explains that sinking fund categories often depend on lifestyle, family size, and personal expenses in its guide to sinking fund categories.

If your budget feels messy, start by learning how to organize your budget category setup before adding sinking funds.

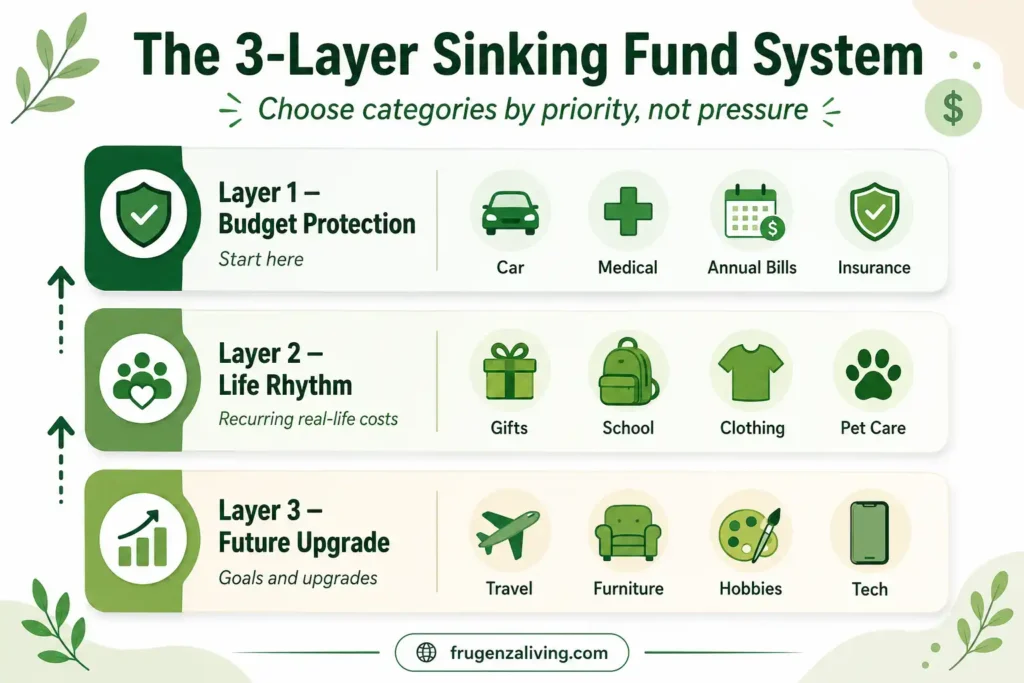

The 3-Layer Sinking Fund Category System

Not all sinking fund categories have the same job.

Use the 3-Layer Category Filter to decide what deserves money first.

- Layer 1 — Budget Protection: categories that stop predictable expenses from breaking your monthly budget.

- Layer 2 — Life Rhythm: recurring seasonal, family, and lifestyle costs.

- Layer 3 — Future Upgrade: goals and upgrades that improve life but are less urgent.

Beginners should usually start with Layer 1. Once those funds feel steady, add Layer 2. Layer 3 is helpful, but it should not push out more urgent planned expenses.

Sinking Fund Categories List by Priority

A good sinking fund categories list should not just be long. It should be useful.

Here is a priority-based list to help you choose what actually fits your budget.

Layer 1: Budget Protection Categories

These are the best sinking fund categories to start with because they often turn into budget problems when ignored.

Good Layer 1 categories include:

- Car maintenance and repairs

- Insurance premiums

- Medical and dental costs

- Annual subscriptions

- Home repairs or renter repairs

- Pet medical care

- Work-related expenses

- School fees or supplies

- Taxes or license renewals

Car maintenance is one of the most useful sinking fund categories for beginners because repairs, tires, oil changes, and registration fees do not always arrive at convenient times.

Annual subscriptions and renewals are another big one. A $120 renewal may not sound huge, but if three annual bills hit in the same month, they can make the budget feel broken.

Medical, dental, pet, and home repair categories are also important because they are not always emergencies, but they can still be too large for one paycheck.

Once you choose your categories, the next step is to split your income for budgeting so each fund gets money consistently.

Layer 2: Life Rhythm Categories

Layer 2 categories are not always urgent, but they repeat often enough to deserve a place in your budget.

These include:

- Holidays

- Birthday gifts

- Family events

- Clothing and shoes

- Kids’ activities

- Back-to-school costs

- Seasonal utilities or heating costs

- Hosting guests

- Personal care

These are the categories that quietly create budget leaks.

Holiday spending does not appear from nowhere. Birthdays happen every year. Kids’ activities, school supplies, and seasonal clothing often repeat. If you ignore these categories, they may not feel urgent until they all show up together.

Layer 3: Future Upgrade Categories

Layer 3 categories are still useful, but they should usually come after the basics.

These include:

- Travel

- Furniture

- Home improvement

- New tech or phone replacement

- Hobbies

- Courses or learning

- Wedding or big celebration

- New car down payment

- Moving costs

These funds can make your budget feel more intentional. But if your car maintenance fund is empty and your annual bills are not covered, a furniture upgrade fund may not be the best first priority.

This does not mean Layer 3 categories are bad. It means timing matters.

The Best Sinking Fund Categories for Beginners

If you are new to sinking funds, do not start with every category.

Start with five:

- Car maintenance

- Annual bills or subscriptions

- Medical or dental

- Holidays and gifts

- Home or renter repairs

These five categories are not perfect for everyone, but they cover many of the most common budget disruptors.

If you do not own a car, replace car maintenance with transportation, public transit, bike repairs, or travel home. If you rent, replace home repairs with renter repairs, moving costs, or basic household replacements.

If these five feel like too much, start with three. A small list you actually fund is better than a perfect list you abandon.

As you choose categories, make sure you understand whether each expense belongs in a sinking fund or emergency fund.

Overlooked Sinking Fund Categories Most People Forget

Some of the best sinking fund ideas are not the obvious ones.

Here are overlooked sinking fund categories by type:

Paperwork and renewals

- Replacement documents or passports

- Car registration or license renewal

- Professional licensing

- Work certificates

Home, tech, and replacement costs

- Appliance replacement

- Phone replacement

- Software renewals

- Small household replacements

Transportation and daily-life costs

- Parking and tolls

- Bike repairs

- Public transit passes

- Travel home

Family, school, and pet costs

- Kids’ school photos and events

- Guests or hosting

- Vet checkups

- Pet medication

- Seasonal clothing

These categories seem small until they arrive together.

A $40 school event, $75 software renewal, $60 parking cost, and $100 pet medication refill can easily feel like a budget emergency if there is no plan. But if you already know they might happen, they belong somewhere in your planned expenses budget.

How to Choose Your Own Sinking Fund Categories

Use the Repeat–Size–Stress Test before creating a new category.

Ask:

- Repeat: Does this expense happen again?

- Size: Is it too large for one paycheck?

- Stress: Would ignoring it create pressure later?

If the answer is yes to at least two of the three, the category may deserve a sinking fund.

For example, holiday gifts usually repeat, may be too much for one paycheck, and can create stress if ignored. That is a strong sinking fund category.

A random item you might want someday may not need its own category yet.

If you need help with the basic setup and formula, read this guide on sinking funds for beginners.

A simple review your sinking funds monthly helps you update your sinking funds before future expenses surprise you.

Categories You Should Not Start With

Not every category deserves a spot right away.

Avoid starting with categories that are:

- Too vague

- Rare and unlikely

- Mostly wishful thinking

- Competing with urgent bills

- Too small to track separately

- Better covered by an emergency fund

- Lifestyle upgrades when basic funds are empty

A category is not bad just because it is optional. Travel, hobbies, home decor, and tech upgrades can all be good sinking fund categories.

But if your Layer 1 categories are unfunded, too many fun funds can make the system weaker.

The goal is not to create the prettiest budget. The goal is to create a budget that survives real life.

Example: A Simple Sinking Fund Category Setup

Here is a simple beginner setup:

- Car maintenance: $50/month

- Annual bills: $20/month

- Medical or dental: $40/month

- Holidays and gifts: $35/month

- Home or renter repairs: $30/month

Total: $175/month

If $175 feels too high, start with three categories:

- Car maintenance

- Annual bills

- Holidays and gifts

Then add medical, pet, home, or family categories later.

If you do not have a car, swap in transportation or travel home. If you have children, school expenses may move into Layer 1 or 2. If you have pets, pet care may be more urgent than travel.

Your list should match your life, not someone else’s printable.

How to Review Your Sinking Fund Categories

A sinking fund categories list should not be frozen forever.

Review it once a month or once per quarter. During a monthly budget reset routine, ask:

- Which category actually got used?

- Which category stayed untouched?

- Which expense surprised me this month?

- Which fund needs a higher monthly amount?

- Which fund can pause for now?

This keeps your list clean. If a category no longer fits your life, remove it. If a new expense keeps showing up, add it.

For digital tracking, you can also organize sinking fund tracker categories inside a digital cash envelope system so each fund has its own balance.

My Simple Rule for Choosing Categories

One thing that helped me save over $15,000 in a year was not creating more categories. It was choosing better ones.

That result did not come from one category or one trick. It came from choosing small systems I could repeat, and car maintenance was one of the first categories that made budgeting feel less chaotic.

Before that, car costs usually felt like they interrupted the month instead of belonging inside the budget. I knew car expenses would come eventually, but I did not treat them like part of normal life.

At first, I thought a good budget needed a category for everything. But the more categories I made, the harder the system became to manage. I was tracking too much and funding too little.

The category that changed the way I looked at sinking funds was simple: car maintenance.

It was not exciting. It did not look impressive. But it protected my budget from one of the expenses that had surprised me before. Once I started putting aside a small amount for car costs, repairs felt less like a crisis and more like something I had already expected.

That became my simple rule:

Start with the category that has already hurt your budget once.

Do not start with the prettiest category. Do not start with the longest list. Start with the expense that has already caused stress in real life. That is usually where your first sinking fund category belongs.

Final Thoughts: A Good Sinking Fund List Should Make Budgeting Easier

A good sinking fund categories list is not the longest list.

It is the list that helps you prepare for the expenses most likely to disrupt your budget.

Start with Layer 1 if your budget feels tight. Add Layer 2 when your basic funds feel steady. Use Layer 3 for upgrades, goals, and bigger plans when your foundation is stronger.

The best sinking fund categories are not the ones that look good on a printable list. They are the ones that stop your real life from wrecking your real budget.

FAQ

What are the best sinking fund categories?

The best sinking fund categories are the ones that protect your budget from predictable expenses. Common examples include car maintenance, annual bills, medical costs, holidays, gifts, insurance premiums, pet care, and home or renter repairs.

How many sinking fund categories should I start with?

Beginners should usually start with 3–5 sinking fund categories. Start with the categories that have already surprised your budget before, such as car maintenance, annual bills, holidays, or medical costs.

What are sinking fund categories for beginners?

Good sinking fund categories for beginners include car maintenance, annual subscriptions, medical or dental costs, holidays and gifts, pet care, home or renter repairs, and school expenses.

What are overlooked sinking fund categories?

Overlooked sinking fund categories include car registration, passports, appliance replacement, phone replacement, seasonal clothing, parking, tolls, pet medication, school photos, work tools, and software renewals.

How do I choose the right sinking fund categories?

Use the Repeat–Size–Stress Test. If an expense happens again, is too large for one paycheck, and would create stress if ignored, it is probably a good sinking fund category.

What sinking fund categories should I not start with?

Avoid starting with vague, rare, or low-priority lifestyle categories if your basic budget protection categories are still empty. Start with categories that have already disrupted your budget before.

The ideas shared here come from real-life experience and practical habits that actually work.

→ Read more about Jeffi

- How to Stop Buying Coffee Every Day Without Giving Up Coffee - July 25, 2026

- 8 Meals for One Without Leftovers—and How to Use the Rest - July 22, 2026

- 9 Cheap Dinners for One Person on a Budget That Feel Complete - July 20, 2026