I used to think reducing living costs meant making big sacrifices.

Moving somewhere cheaper. Cutting everything. Living in a way that felt restrictive.

But after actually tracking my spending for a few weeks, I realized something different.

Most of the problem wasn’t my biggest expenses—it was the small, repeated habits that didn’t feel important at the time.

But reducing living costs is not only about cutting small purchases. It is also about understanding how your daily life is set up.

The way you eat, commute, use your home, manage bills, handle busy days, and replace everyday items all shape your cost of living.

That is why the most sustainable approach is not to ask, “What can I cut today?” A better question is, “Which part of my normal routine keeps making life more expensive than it needs to be?” When you improve the routine, the savings do not depend on willpower every single day.

What “Living Costs” Really Include

When people talk about living costs, they usually focus on big categories like rent, utilities, and groceries.

But in everyday life, it’s more than that.

It also includes:

- takeout on busy days

- subscriptions you barely use

- small online purchases

- convenience spending

These smaller expenses often feel harmless—but they’re usually where most money leaks happen.

Look at Your Cost of Living as a System

Living costs are not just a list of bills. They are a system. Rent, food, transportation, utilities, subscriptions, household supplies, repairs, and convenience purchases all connect to the way your daily life works.

For example, a long commute can increase fuel costs, food costs, and convenience spending. A disorganized kitchen can increase grocery waste and takeout.

A home that is hard to maintain can create more replacement costs. A schedule with no backup plan can make paid convenience feel unavoidable.

When you look at your cost of living as a system, you stop blaming one category and start seeing how one habit affects another. This makes it easier to reduce costs without feeling like you are constantly taking things away.

The goal is to make your normal life cheaper to run.

Why Living Costs Keep Increasing

Lifestyle Inflation

One thing I didn’t notice at first was how my spending slowly increased over time.

Not because I was reckless—but because I kept upgrading small habits.

Better food. More convenience. Slightly more expensive choices.

This is often called lifestyle inflation, and it happens quietly.

Find Your Cost Pressure Points

A cost pressure point is any part of your life that keeps pushing you to spend more. It may not look like a budget problem at first. It may look like a schedule problem, a home setup problem, a transportation problem, or a planning problem.

For example, if evenings are always rushed, dinner becomes more expensive. If your pantry is never stocked with easy meals, takeout becomes easier.

If your bills are scattered across different dates, late fees or forgotten charges become more likely.

If your home is full of items you do not use, you may keep buying duplicates because you cannot find what you already have.

Reducing living costs becomes easier when you identify these pressure points. Instead of trying to cut every category at once, you fix the part of your routine that keeps creating extra costs.

This is different from strict budgeting. You are not only tracking money. You are improving the situation that causes the spending.

Convenience Spending

Modern life makes spending easier than ever.

Food delivery, digital subscriptions, one-click purchases—they all remove friction.

And when spending is easy, it becomes frequent.

This pattern is also influenced by broader factors like inflation and changing consumer behavior, where convenience-based services become more common—and more expensive over time.

Where Most People Overspend Without Realizing

Looking back, my biggest expenses weren’t the problem.

It was everything in between.

- ordering food when I didn’t plan meals

- keeping subscriptions I rarely used

- buying small things online out of habit

- paying extra just to save time

Individually, these didn’t feel like mistakes.

But together, they added up more than I expected.

Use the “Cost Per Routine” Test

One helpful way to reduce living costs is to look at routines, not just purchases. Ask yourself: “How much does this routine cost me each week or month?”

For example, your workday routine may include coffee, lunch, fuel, parking, snacks, or small purchases. Your evening routine may include takeout, delivery fees, streaming, or convenience food. Your weekend routine may include shopping, entertainment, restaurants, or errands that lead to extra spending.

The point is not to remove every routine. The point is to see which routines have become more expensive than you realized. Once you know that, you can redesign one routine at a time.

A cheaper routine is easier to maintain than a strict rule. Instead of saying, “I will never buy lunch again,” you might bring lunch three days a week. Instead of saying, “I will stop all weekend spending,” you might plan one low-cost weekend option before Saturday arrives.

Reducing living costs becomes more realistic when the cheaper choice is built into the routine.

How to Reduce Living Costs (Step-by-Step)

1. Start Tracking (But Keep It Simple)

I didn’t use any complicated app at first.

I just wrote down what I spent—roughly.

That alone changed how I saw money.

2. Reduce Frequency, Not Everything

At one point, I tried cutting everything at once.

No takeout. No small purchases. No flexibility.

It worked—for about a week.

Then I went back to old habits even harder.

That’s when I realized the problem wasn’t discipline. It was trying to change too much too fast.

So instead, I focused on reducing frequency:

- takeout 4 times a week → 2

- online purchases → once a week

- subscriptions → only what I actually used

One of the most effective ways to reduce monthly bills is to cut your monthly expenses.

3. Optimize Fixed Expenses

I didn’t move or drastically change my lifestyle.

But I did:

- switch to a cheaper phone plan

- cancel unused subscriptions

- reduce utility waste

Small adjustments—still noticeable impact.

If you’re just getting started, this frugal living guide for beginners explains how to reduce living costs step by step.

4. Reduce Utility Waste (Simple but Overlooked)

This was one area I used to ignore because the changes felt too small to matter.

But once I paid attention, I realized how often energy and water were being used without purpose.

For example:

- leaving lights on in rooms I wasn’t using

- charging devices overnight every day

- running the washing machine half-full

- using hot water longer than necessary

None of these felt expensive individually.

But over time, they added up quietly.

So I made a few small adjustments:

- turning off lights more consciously

- unplugging chargers when not in use

- washing clothes only with full loads

- reducing shower time by just a few minutes

I didn’t aim for perfection—just awareness.

The difference wasn’t dramatic in a single bill, but over a few months, it became noticeable.

And more importantly, it required almost no sacrifice. This helps you maintain a budget friendly lifestyle over time.

5. Plan Small Things Ahead

One thing that helped more than expected was simple planning.

Not extreme meal prep—just basic preparation.

It reduced those “I’ll just order something” moments.

It’s possible to live cheaply and comfortably without feeling like you’re sacrificing your lifestyle.

6. Add Friction to Spending

I removed saved payment methods and logged out of shopping apps.

It sounds small—but it worked.

Because most unnecessary spending happens when it’s too easy.

Lower the Cost of Repetition

The expenses that matter most are often the ones that repeat. A one-time purchase may feel bigger, but repeated costs quietly shape your cost of living.

Think about what you repeat every week: meals, transportation, laundry, cleaning, groceries, work lunches, snacks, entertainment, and household supplies. If one repeated routine costs a little too much, it can become expensive over a year.

This is why small system changes can be powerful. A cheaper phone plan saves every month. A simple grocery routine reduces waste every week. A full laundry load saves water and energy over time. A planned lunch routine reduces daily convenience spending. A basic home maintenance habit may prevent bigger replacement costs later.

You do not need to change everything. Start with one repeated cost and make it easier, simpler, or cheaper. Repetition is where long-term savings usually begin.

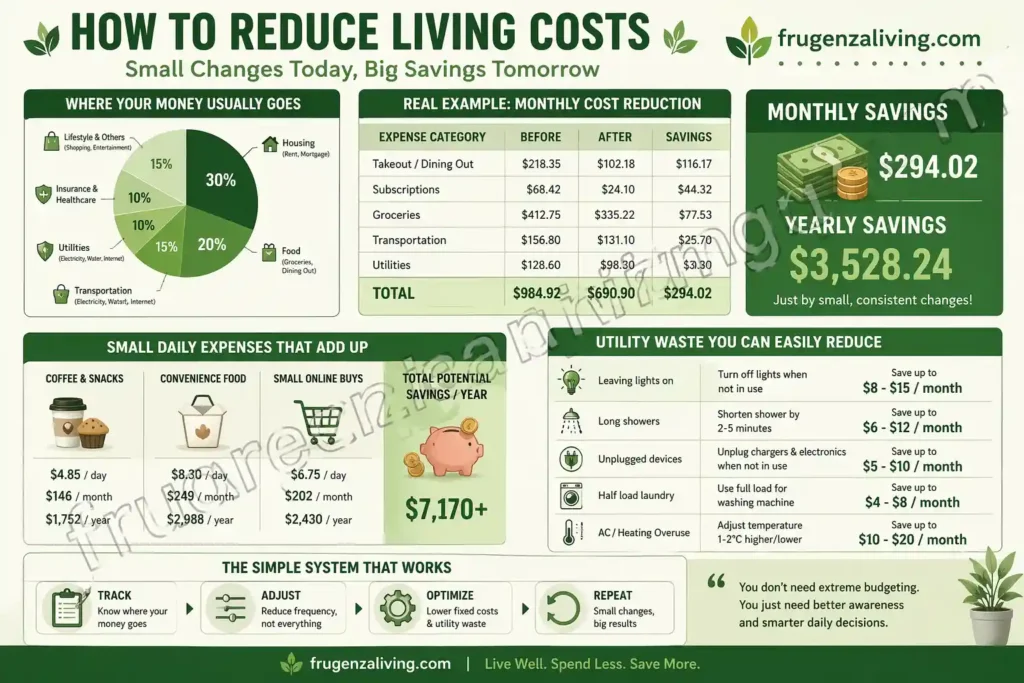

Data from My Spending Adjustment Experiment

After tracking my spending more consistently, I started noticing patterns that didn’t feel obvious before.

Here’s a simplified version of what I found:

| Spending Pattern | Daily Cost | Monthly Cost | Yearly Impact |

|---|---|---|---|

| Coffee & snacks | $4.85 | $146 | $1,752 |

| Convenience food | $8.30 | $249 | $2,988 |

| Small online buys | $6.75 | $202 | $2,430 |

👉 Total potential savings: $7,170 per year

Of course, these numbers vary depending on where you live. Living costs in major cities are different from smaller towns—but the pattern is usually the same.

Small expenses repeat more often than we realize.

The most important lesson from this kind of tracking is not the exact number. The lesson is seeing which costs are connected to repeated routines. Coffee, snacks, convenience food, and small online buys may look separate, but they often come from the same pattern: busy days, low planning, easy payments, or habits that run on autopilot.

That is why the next step should not be guilt. The next step should be redesigning the routine that created the spending. If convenience food keeps showing up, fix the meal routine. If online buys repeat, change the shopping environment. If snacks appear every workday, prepare a cheaper default option.

Tracking is useful only when it leads to a practical change.

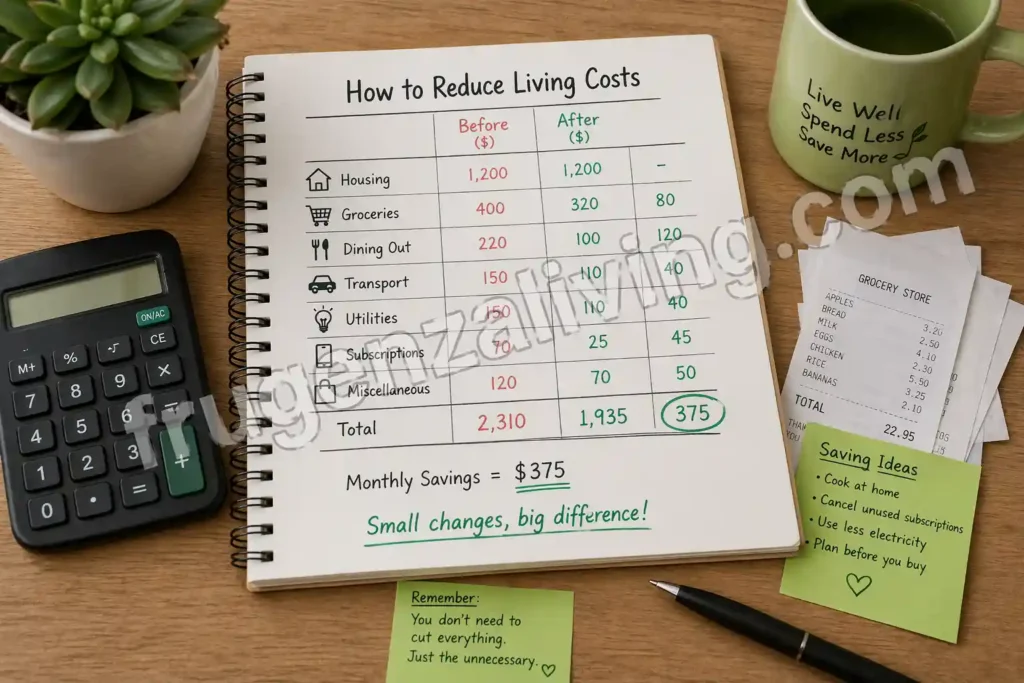

Real Example of Monthly Cost Reduction

Here’s what realistic adjustments looked like for me:

| Expense Category | Before | After | Savings |

|---|---|---|---|

| Takeout | $218 | $102 | $116 |

| Subscriptions | $68 | $24 | $44 |

| Groceries | $412 | $335 | $77 |

👉 Monthly savings: $237

👉 Yearly impact: $2,844

Nothing extreme.

Just consistent changes.

This is only one example, not a guaranteed result. Actual savings depend on location, household size, rent, transportation, food prices, debt, utilities, and current habits. Some people may save less at first, especially if their budget is already tight. Others may save more if they have several repeated routines that can be improved.

The real value is not only the dollar amount. The value is proving that living costs can often be reduced without one dramatic sacrifice. When you improve several normal routines, the savings can become easier to maintain.

A Simple Weekly Reality Check

At one point, I wrote down small purchases from a grocery receipt.

Snacks, drinks, small add-ons.

They didn’t look like much individually.

But over a week, it looked like this:

- Monday → $9.20 takeout

- Wednesday → $11.75 small purchase

- Friday → $8.40 convenience food

- Sunday → $6.15 snacks

👉 Weekly: $35.50

👉 Monthly: $142

👉 Yearly: $1,704

Seeing it written down made it feel more real.

A Simple System to Lower Costs Without Sacrifice

Instead of strict budgeting, I started using a simple idea:

- Automatic spending → happens without thinking

- Intentional spending → happens after a pause

My goal wasn’t to stop spending.

It was to shift more spending into the intentional category.

This becomes easier when you build frugal habits that actually work in your daily routine.

A Better Way to Think About Reducing Costs

I used to think saving money meant cutting things out.

Now I see it differently.

Keep what matters. Reduce what doesn’t.

That small shift made everything easier to maintain. Small adjustments can help you reduce your daily expenses over time.

Do Not Lower Costs in a Way That Raises Stress

Some cost-cutting choices look good on paper but create more stress later. Skipping basic maintenance, buying the lowest-quality item every time, eating meals you dislike, cutting all convenience, or making your schedule too difficult can backfire.

A lower cost is only useful if it still works in real life. If a cheaper choice makes your routine harder, you may end up spending more later because you are tired, frustrated, or forced to replace something too soon.

A better rule is to reduce living costs in a way that keeps your life stable. Choose changes that save money while still protecting your time, energy, health, and basic comfort. Sustainable savings should make life feel more manageable, not more fragile.

FAQ: How to Reduce Living Costs

How can I reduce living costs quickly?

Start by cutting frequent small expenses like takeout and subscriptions. These are easier to adjust and provide immediate savings.

What expenses should I cut first?

Focus on recurring costs you don’t fully use, such as subscriptions and convenience spending.

Can I reduce living costs without moving?

Yes. Most savings come from daily habits rather than major life changes like relocating.

How much can I realistically save?

Many people can save around $200–$400 per month through small, consistent adjustments.

What is the biggest expense to reduce?

Housing is usually the largest, but the easiest savings come from smaller repeated expenses.

How can I reduce living costs without feeling deprived?

Focus on reducing unnecessary spending while keeping what matters. This makes the process sustainable and less restrictive.

Final Thoughts

Reducing living costs does not always require a major lifestyle change. Sometimes the biggest improvement comes from making your normal life cheaper to run.

Look at your routines. Notice which parts of your day create extra spending. Lower the cost of repeated habits. Prevent expenses before they happen. Build a few lower-cost defaults so convenience does not become your only backup plan.

The goal is not to live with less comfort or constant restriction. The goal is to create a life structure that costs less to maintain. When your routines become simpler, your home becomes easier to manage, and your spending becomes less automatic, reducing living costs becomes much more realistic.

The ideas shared here come from real-life experience and practical habits that actually work.

→ Read more about Jeffi

- How to Split Bills Between Paychecks Without Overloading One Check - August 9, 2026

- Subscription Audit Checklist: Find and Review Every Recurring Charge - August 9, 2026

- How to Budget for Subscriptions Without Surprise Renewals - August 7, 2026