Living on a budget doesn’t usually fail because of big decisions.

It fails because of small ones that feel harmless.

That late-night food order after a long day.

That “just scrolling” moment that turns into a purchase.

That extra upgrade that feels too small to matter.

None of these feel like mistakes.

But repeated often enough, they quietly shape your entire cost of living.

What makes this difficult is that these decisions rarely feel like financial decisions in the moment. They feel like convenience, relief, or even a reward after a long day. That’s why traditional advice like “just spend less” often doesn’t work—it ignores how spending actually happens in real life.

Why Budget-Friendly Living Feels Hard (Even When It Shouldn’t)

Most spending decisions aren’t logical.

They’re emotional.

After work, energy drops. Decision-making gets weaker. Convenience starts to feel like a necessity.

This is where decision fatigue comes in.

Studies on consumer behavior show that people are significantly more likely to spend money when they are mentally tired or stressed. It’s not about lack of discipline—it’s about reduced cognitive capacity to evaluate choices.

That’s why many people spend more at night, on weekends, or during stressful periods. The brain is simply trying to conserve energy, and spending becomes the easiest option.

The Pattern Most People Miss (Lifestyle Inflation in Real Life)

Spending rarely increases all at once.

It creeps.

- slightly better meals

- faster delivery

- more subscriptions

Over time, these become your “normal.”

This is lifestyle inflation.

And it doesn’t feel like a problem—until you realize your expenses have quietly increased without any clear reason.

In many cases, income increases slightly, and spending follows immediately. Without awareness, this pattern repeats for years, making it harder to build savings or an emergency fund.

Set Your Personal Lifestyle Standard

A budget-friendly lifestyle becomes easier when you decide what “normal” should look like before your spending decides it for you.

Without a personal lifestyle standard, small upgrades can quietly become expectations. A nicer delivery option, a faster service, a premium subscription, or a more expensive weekend routine can start to feel normal even when it does not truly improve your life.

Your lifestyle standard is not a strict budget. It is a simple idea of what feels enough for your current season.

For example, you might decide that most meals come from home, takeout is planned instead of random, entertainment stays simple during busy months, and upgrades only happen when they solve a real problem.

This matters because lifestyle inflation often happens when there is no boundary between “nice to have” and “normal.” A budget-friendly lifestyle works better when you choose your normal on purpose.

Budget Friendly Lifestyle Tips That Actually Make a Difference

1. Reducing Takeout Frequency Instead of Eliminating It

Cutting everything doesn’t work.

Reducing frequency does.

From experience, going from 4 takeout meals to 2 per week saved around $90–$120 monthly without feeling restrictive.

More importantly, it removed the feeling of “restriction,” which is often what causes people to give up entirely.

The goal is to live cheaply and comfortably without feeling like you’re missing out.

2. The 72-Hour Rule (That Actually Works in Real Life)

Impulse buying usually feels urgent.

Waiting 72 hours removes that urgency.

One month of applying this avoided about $110 in unnecessary purchases.

Most items weren’t even remembered after a few days.

A big part of this lifestyle is learning how to reduce your living costs over time.

This simple delay creates distance between emotion and action, which is where better decisions happen.

3. The Real Trigger: Browsing, Not Buying

Most purchases don’t start with need.

They start with browsing.

Scrolling through apps creates exposure, and exposure creates desire. That’s how modern platforms are designed.

Removing that one habit reduced spending more than any budgeting method. Maintaining a budget-friendly lifestyle is easier with a simple budgeting approach.

4. Repeating Meals to Reduce Grocery Waste

Trying to eat “perfectly” led to wasted groceries.

Repeating simple meals worked better.

Less waste. Less stress. Lower cost.

It also reduces decision fatigue, which indirectly lowers the chances of ordering food impulsively.

5. Utility Awareness (Without Obsessing)

Leaving lights on. Half-load laundry. Long showers.

None feel expensive.

But they’re consistent.

After a few months of small adjustments, utility bills stopped increasing.

The goal isn’t perfection—it’s awareness. Even a slight shift in daily behavior can stabilize costs over time.

6. Using Budgeting Apps Like PocketGuard or YNAB for Awareness

Strict budgeting felt restrictive.

Tracking felt different.

Tools like:

- PocketGuard

- YNAB

- basic banking apps

helped reveal patterns.

Not to control spending, but to understand it.

Even checking transactions every few days can create awareness that changes behavior naturally. Many people don’t need a perfect budget—they just need visibility.

7. Avoiding “Small Upgrades” That Add Up

Faster delivery. Premium add-ons.

Each one is small.

But repeated often, they quietly raise your cost of living.

These are often the hardest to notice because they are framed as “improvements,” not expenses.

8. Avoiding Financial Decisions When Mentally Tired

Spending decisions made at night or after work are often less intentional.

Reducing decision-making during those moments helps control spending.

9. Focusing on One Expense Category at a Time

Trying to fix everything at once leads to burnout.

Focusing on one category—like takeout or subscriptions—creates better results.

This becomes easier when you build effective frugal habits that actually work in your daily routine.

Create Upgrade Rules Before You Want an Upgrade

Small upgrades are easier to control when you create rules before you want them. In the moment, an upgrade usually feels harmless.

Faster shipping, premium versions, larger portions, better seats, app add-ons, and small convenience fees all seem reasonable because each one feels minor.

A simple upgrade rule gives you a pause without making life feel restrictive. You might decide to upgrade only if the item saves meaningful time, solves a repeated problem, replaces something you truly use, or still feels worth it after a waiting period.

If the upgrade only feels good because it is available right now, it may not need to become part of your lifestyle.

This helps protect your budget without removing every comfort. You are not banning upgrades. You are making sure upgrades stay intentional instead of becoming automatic.

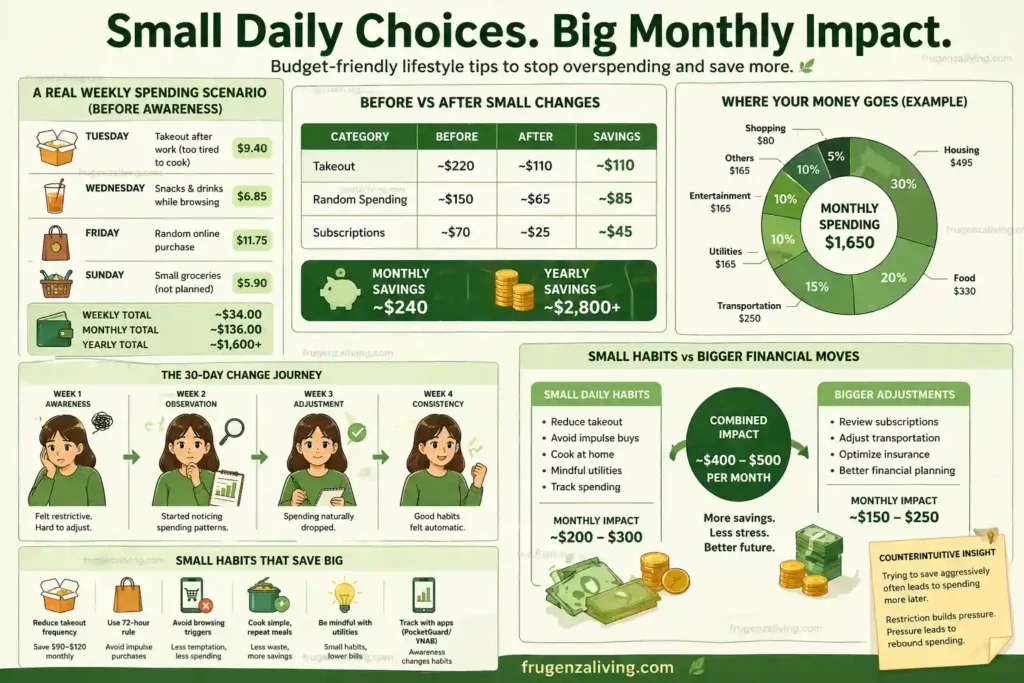

A Real Weekly Spending Pattern (Before Awareness)

- Tuesday night → $9.40 takeout (too tired to cook)

- Wednesday → $6.85 snacks

- Friday → $11.75 random online item

- Sunday → $5.90 groceries

Weekly total: about $34

Monthly: around $136

Yearly: over $1,600

Nothing extreme.

Just consistent.

And consistency is what makes the biggest difference over time.

And also, this frugal living guide for beginners explains how to build a budget-friendly lifestyle step by step.

Before vs After Small Changes

| Category | Before | After | Savings |

|---|---|---|---|

| Takeout | ~$220 | ~$110 | ~$110 |

| Random spending | ~$150 | ~$65 | ~$85 |

| Subscriptions | ~$70 | ~$25 | ~$45 |

Monthly savings: around $240

Yearly: around $2,800+

These changes didn’t come from strict control.

They came from reducing automatic behavior.

What Happened After 30 Days

Week 1 → felt restrictive

Week 2 → started noticing patterns

Week 3 → spending naturally dropped

Week 4 → habits felt automatic

The most important shift happened in awareness, not discipline.

Once spending patterns became visible, decisions started changing without forcing them.

Counterintuitive Insight

Trying to save aggressively often leads to spending more later.

Because restriction builds pressure.

And pressure leads to rebound spending.

A more flexible approach is often more sustainable and more effective over time.

Small Habits vs Bigger Financial Moves

| Type | Monthly Impact |

|---|---|

| Daily habits | ~$200–$300 |

| Bigger adjustments | ~$150–$250 |

Combined impact: around $400–$500 per month

That’s often enough to build an emergency fund faster or reduce financial stress significantly.

A Simple System That Actually Works

Instead of budgeting:

- reduce automatic spending

- increase intentional decisions

That’s it.

If you want to reduce living costs, this works better than strict rules.

And if your main issue is behavior, learning how to stop wasting money matters more than cutting everything.

FAQ

What is a budget friendly lifestyle?

A way of living that focuses on intentional spending while maintaining comfort.

How can I live on less without feeling restricted?

Reduce frequency instead of eliminating everything.

What should I cut first?

Frequent small expenses.

Is frugal living hard?

Only when you try to change everything at once.

How much can I save?

Around $150–$400 monthly for most people.

Final Thoughts

A budget-friendly lifestyle is not about living with constant restriction. It is about choosing a version of normal that your money can support without creating pressure every month.

Start by noticing where your lifestyle has become more expensive without your permission.

Then set a few simple boundaries: when you order takeout, when you upgrade, when you shop, and what kind of comfort actually matters to you. These boundaries do not have to be strict. They only need to make your choices more intentional.

The goal is not to spend less on everything. The goal is to stop letting convenience, stress, scrolling, and small upgrades define your lifestyle for you.

When you choose your lifestyle standard on purpose, saving money becomes less about discipline and more about living in a way that actually fits your life.

The ideas shared here come from real-life experience and practical habits that actually work.

→ Read more about Jeffi

- How to Split Bills Between Paychecks Without Overloading One Check - August 9, 2026

- Subscription Audit Checklist: Find and Review Every Recurring Charge - August 9, 2026

- How to Budget for Subscriptions Without Surprise Renewals - August 7, 2026