There was a time when my income barely covered the basics.

Every month felt the same. Money came in, bills got paid, and somehow there was almost nothing left. It wasn’t about spending recklessly. It was just tight. Too many fixed costs, too little room to adjust.

At that point, most advice didn’t help. “Just save more.” “Cut unnecessary expenses.” It sounded simple, but it didn’t match reality.

That’s when I started thinking differently. Instead of focusing on saving, I focused on how to manage money with low income, and that shift made things feel more stable, even before my income changed.

Why Managing Money Feels Harder on a Low Income

Managing money becomes more challenging when your margin is small.

With a higher income, small mistakes don’t matter much. Overspend a little, and you can recover next month. But with a low income, every decision has weight. A small miscalculation can affect your entire week.

Fixed expenses take up a large portion of income, leaving very little flexibility.

There is also a psychological factor that often gets ignored. Research on scarcity mindset shows that when people operate under financial pressure, their cognitive bandwidth decreases, making it harder to make optimal decisions.

This often leads to short-term choices, even when long-term thinking would be better.

You can explore this concept further here:

The Shift That Changes Everything (Management vs Saving)

One of the biggest mindset changes was understanding this:

Saving is the result.

Management is the process.

When income is low, focusing too much on saving creates pressure. It makes you feel like you’re failing, even when you’re doing your best.

This becomes easier when you strengthen your financial foundation with simple budgeting basics.

Money management focuses on control instead:

- where money goes

- when it goes

- how decisions are made

Once I focused on managing flow, things became more predictable.

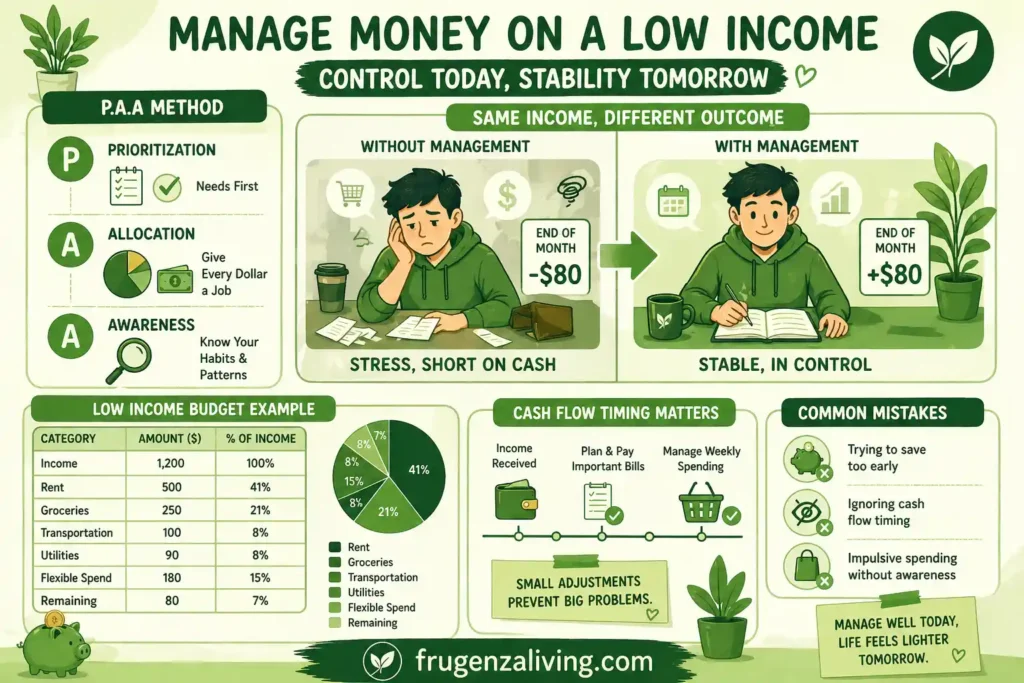

The P.A.A Method (Prioritization, Allocation, Awareness)

Instead of using complex systems, I started relying on a simple framework I now call:

The P.A.A Method

- Prioritization → what must be paid first

- Allocation → how money is distributed

- Awareness → understanding patterns

This approach works especially well if you’re learning how to save money on a low income in a realistic way.

Step-by-Step: How to Manage Money on a Low Income

Step 1: Know Your “Survival Number”

A Survival Number is the absolute minimum amount of money required to cover essential living costs for one month, including rent, basic food, and utilities.

The first time I calculated this number, it changed how I viewed money completely.

Instead of guessing, I had a clear baseline. I knew exactly how much needed to be protected before anything else.

Step 2: Separate Needs vs Flexible Needs

Not all “needs” are fixed.

Groceries, for example, are necessary, but the amount can vary. The same applies to transportation and utilities.

I started dividing expenses into:

- fixed needs

- flexible needs

This gave me control without making the system complicated.

Many beginners struggle until they understand how to track expenses easily in a simple way.

Step 3: Control Cash Flow Timing

Timing turned out to be more important than I expected.

There were months when I technically had enough money but still struggled because of when expenses were due. Bills stacked early, while income came later.

This makes it easier to manage everyday spending without feeling overwhelmed.

Adjusting timing—even slightly—helped reduce that pressure.

Step 4: Avoid Financial Blind Spots

Before I paid attention, money often disappeared without a clear reason.

It wasn’t large purchases. It was small, repeated spending triggered by habits—especially when I was tired or stressed.

Once I became aware of those patterns, I didn’t need strict rules. Awareness alone started changing my behavior.

The real challenge isn’t starting, but learning how to stay consistent with a budget over time.

Step 5: Build Stability Before Saving

This was the hardest lesson.

Trying to save too early created frustration. What worked better was building stability first:

- bills paid consistently

- fewer surprises

- controlled weekly spending

Once that foundation was stable, saving became easier and more natural.

Managing money becomes much easier when you improve your financial habits that support your decisions.

Find Your Cash-Flow Gap Before It Happens

Knowing your monthly total is useful, but it does not always show when money will become tight. You may earn enough to cover the month overall and still struggle during the days between a large bill and your next paycheck.

To find the gap, look only at the next 14 days. Write down your current available balance, the dates income will arrive, every bill due during that period, and the minimum amount needed for food and transportation. Then calculate the estimated balance after each expense.

For example, your two-week plan might look like this:

- Starting available balance: $420

- Rent due on the 3rd: −$300

- Groceries and transportation until payday: −$90

- Estimated amount before the next paycheck: $30

The important number is not only the $420 you started with. It is the lowest point your balance is expected to reach. That is your cash-flow gap warning.

Once you can see the difficult period in advance, you have more options. You may delay flexible spending, divide grocery money by week, move a non-essential purchase, or ask whether a bill’s due date can be changed. The goal is to make the tight days visible before they become an emergency.

Repeat this short check whenever income arrives or a major bill changes. With a low income, a two-week view can sometimes be more useful than a perfect monthly budget because it shows exactly when your money needs the most protection.

A Real-Life Example (Low Income Budget Flow)

Here’s a realistic example:

| Category | Amount ($) |

|---|---|

| Income | 1,200 |

| Rent | 500 |

| Groceries | 250 |

| Transportation | 100 |

| Utilities | 90 |

| Flexible Spend | 180 |

| Remaining | 80 |

This isn’t about perfection. It’s about understanding flow.

What to Do When the Numbers Still Do Not Work

Sometimes careful budgeting is not enough. If basic housing, food, utilities, medication, transportation, and required payments cost more than the income available, the problem is not a lack of discipline. It is a real shortfall.

When this happens, stop trying to make every category look balanced and protect the expenses that keep you safe and able to function.

Start with housing, basic food, essential utilities, medication, and transportation needed for work or necessary appointments.

The exact order may depend on your circumstances, but essential stability should come before optional spending or an unrealistic savings target.

Next, contact service providers, lenders, landlords, or billing departments before a payment is missed when possible.

Ask whether they offer a different due date, temporary payment plan, hardship arrangement, reduced-cost plan, or another option that changes the timing or size of the payment. Make notes about who you contacted, what was offered, and the date of the next required action.

Also check whether your household qualifies for local food, utility, transportation, healthcare, housing, or income-support programs. Using temporary assistance is not a budgeting failure. It can protect essential needs while you work on a longer-term solution.

Be cautious about solving a recurring shortfall with expensive short-term borrowing. A loan may cover one difficult week while creating a larger required payment later.

Before borrowing, calculate the full repayment amount and ask whether the next paycheck can realistically cover both normal essentials and the new payment.

A budget is useful because it reveals the gap clearly. It cannot create money that is not there. When the numbers do not work, the responsible next step is to protect essentials, communicate early, use available support, and prevent one shortage from creating several additional fees or debts.

Common Mistakes When Managing Money on a Low Income

Focusing on saving too early often creates pressure.

Ignoring timing leads to avoidable stress.

And small impulsive decisions can have a bigger impact than expected.

What Actually Makes the Biggest Difference

The biggest shift didn’t come from cutting expenses aggressively.

It came from understanding behavior.

Most unnecessary spending happened when I was tired, not when I was careless. Once I noticed that pattern, I could adjust it.

That insight made more difference than any strict budgeting rule.

How to Stay Financially Stable (Even Without High Income)

Stability isn’t about having more money.

It’s about having control.

When you understand your priorities, timing, and habits, things start to feel manageable—even if your income doesn’t change.

FAQ: How to Manage Money with Low Income

What is the best way to manage money on a low income?

The best approach is to focus on controlling cash flow, prioritizing essential expenses, and maintaining awareness of spending habits. Instead of trying to save immediately, creating financial stability first helps build a stronger foundation for long-term money management.

Should I try to save money if my income is very low?

Saving is important, but it should not be the first focus when income is limited. Building stability, such as covering essential expenses and avoiding financial stress, makes saving more sustainable and realistic over time.

How can I avoid running out of money before the end of the month?

Paying attention to cash flow timing and breaking spending into smaller periods can help prevent shortages. Adjusting when bills are paid and monitoring weekly spending creates better control without needing a complex system.

Is budgeting useful with a low income?

Yes, but it should be simplified. Instead of detailed tracking, focusing on key priorities, flexible expenses, and spending awareness makes budgeting more practical and easier to maintain.

Ending

Managing money on a low income isn’t about perfection.

It’s about control.

Once you understand where your money goes, when it goes, and why it goes, things become less overwhelming.

And that’s where real progress begins.

The ideas shared here come from real-life experience and practical habits that actually work.

→ Read more about Jeffi

- How to Split Bills Between Paychecks Without Overloading One Check - August 9, 2026

- Subscription Audit Checklist: Find and Review Every Recurring Charge - August 9, 2026

- How to Budget for Subscriptions Without Surprise Renewals - August 7, 2026