Bills have a way of creeping up quietly. One month feels manageable, then suddenly everything costs more—groceries, subscriptions, even basic utilities. And somehow, your paycheck doesn’t stretch as far as it used to.

If you’ve been trying to figure out how to cut monthly expenses, you’re probably not looking for extreme solutions. You just want something realistic. Something you can actually stick with.

Let’s break this down in a way that makes sense in real life—not in a perfect world.

Cutting monthly expenses does not mean removing every comfort from your life.

It means looking at your recurring costs, spotting the expenses that no longer give enough value, and making small adjustments that are easy to maintain.

In this guide, you’ll learn how to cut monthly expenses by reviewing fixed and flexible bills, reducing repeated money leaks, lowering convenience spending, and building simple habits that help your paycheck stretch further without making your life feel restricted.

What Does “Cutting Monthly Expenses” Actually Mean?

Cutting monthly expenses means reducing ongoing costs in a way that still allows you to live comfortably—without feeling restricted or burned out.

It’s not about removing everything you enjoy.

It’s about:

- Spending with more awareness

- Reducing what doesn’t matter

- Keeping what actually adds value

There’s a big difference between:

- Extreme saving → cutting everything

- Smart reduction → adjusting habits

The second one is what actually works long-term.

The Monthly Expense Audit Method

Monthly Expense Audit Map

Cutting monthly expenses becomes easier when you know which bills to keep, reduce, remove, or review. Use this simple audit map to lower your costs without cutting the things that truly matter.

Keep

Keep expenses that protect your health, work, safety, housing, transportation, basic food, and financial stability.

Reduce

Reduce expenses you still value but spend too much on, such as groceries, takeout, entertainment, or convenience spending.

Remove

Remove expenses you barely use, forgot about, or only keep out of habit, such as unused subscriptions or duplicate services.

Review

Review bills that may be negotiable, such as phone plans, internet, insurance, utilities, memberships, and recurring charges.

20-Minute Monthly Expense Reset

Before cutting anything, do a simple monthly expense audit. The goal is not to judge every purchase.

The goal is to understand which bills are necessary, which ones can be reduced, and which ones are quietly draining your budget.

Start by dividing your expenses into three groups: fixed, flexible, and forgotten. Fixed expenses include rent, insurance, phone bills, debt payments, and basic utilities.

Flexible expenses include groceries, takeout, transportation habits, entertainment, and daily spending.

Forgotten expenses include subscriptions, memberships, free trials, auto-renew services, and small charges you rarely notice.

This method works because not every expense should be treated the same way. Some bills need protection.

Some need adjustment. Some need to be canceled completely.

Once you know which category each expense belongs to, cutting monthly expenses becomes much less overwhelming.

Why Your Monthly Expenses Feel So High

Before cutting anything, it helps to understand why things feel expensive in the first place. Before cutting bigger bills, it helps to reduce your daily expenses so you can free up extra cash immediately.

Rising Cost of Living

Prices go up slowly… until you notice everything feels expensive at once.

Groceries, rent, transport—it all adds up.

Lifestyle Creep

As income or comfort increases, spending follows.

You don’t notice it happening, but suddenly:

- Better groceries

- More subscriptions

- More convenience spending

One important habit is to stop wasting money on unnecessary purchases.

Convenience Habits

This one hits hard.

Busy day? You order food.

Too tired? You buy something quick.

Convenience saves time—but costs money. If you want a step-by-step overview, this frugal living guide for beginners shows how all these changes fit together.

Where Most Monthly Expenses Come From

Most people don’t realize how predictable their spending actually is.

Here’s a simple breakdown:

- Housing / Rent → largest fixed expense

- Food / Groceries → flexible but often underestimated

- Subscriptions → small individually, big combined

- Transportation → fuel, rides, maintenance

- Daily Spending → coffee, snacks, impulse buys

None of these are “bad.”

But they’re the easiest places to adjust.

Fixed vs Flexible Monthly Expenses

One reason monthly expenses feel hard to cut is that some bills are easier to change than others.

Fixed expenses are the costs that are harder to reduce quickly, such as rent, insurance, minimum debt payments, and basic utilities.

Flexible expenses are the costs you can usually adjust faster, such as groceries, takeout, subscriptions, entertainment, personal spending, and small daily purchases.

If you want quick progress, start with flexible expenses first. Cancel one unused subscription, reduce takeout by one meal per week, set a simple grocery limit, or pause unnecessary online shopping.

These changes may look small, but they can create breathing room quickly.

Fixed expenses still matter, but they often require bigger decisions, such as negotiating bills, switching providers, refinancing, moving, or changing transportation.

Flexible expenses are usually the best place to start when you want to lower monthly costs without making a major lifestyle change

How to Cut Monthly Expenses Without Feeling Miserable

This is where most advice gets unrealistic.

You don’t need to cut everything. You just need to adjust.

Reduce Frequency Instead of Eliminating

Cutting something completely rarely lasts.

Example:

- Takeout 4x/week → 2x/week

Why it works:

You still enjoy it, just with better control.

A big part of lowering your monthly bills is learning how to reduce unnecessary spending that often goes unnoticed.

Simplify Recurring Spending

Recurring expenses are often ignored.

Look at:

- Subscriptions

- Memberships

- Auto-renew services

Why it works:

Small monthly charges = big yearly impact.

Start With Recurring Expenses First

Recurring expenses are powerful because they repeat whether you think about them or not. A single subscription may not feel expensive, but several small subscriptions can quietly take money from your budget every month.

Start by checking every automatic payment on your bank statement or credit card. Look for streaming services, apps, memberships, cloud storage, delivery subscriptions, software tools, and free trials that became paid plans.

Then ask one simple question: “Would I sign up for this again today?”

If the answer is no, cancel it. If the answer is maybe, pause it for one month if possible.

Cutting recurring expenses is one of the easiest ways to lower monthly bills because you save money again and again without needing daily discipline.

Audit Subscriptions Honestly

Be real with yourself.

If you haven’t used it in weeks, you probably don’t need it.

Why it works:

Instant savings without changing your lifestyle.

Switch to Lower-Cost Alternatives

You don’t always need to cut—sometimes just switch.

Examples:

- Store brands instead of premium

- Cooking instead of delivery

Why it works:

Same function, lower cost.

Control Small Daily Expenses

This is where money quietly disappears.

Coffee, snacks, small online purchases.

Why it works:

Small changes here have a big combined effect.

You’ll see better results when you combine this with a beginner-friendly budgeting plan.

Use Awareness Instead of Strict Budgeting

You don’t need to track everything.

Just check your spending weekly.

Why it works:

Awareness alone changes behavior. These strategies are especially useful if you’re trying to save money on a low income.

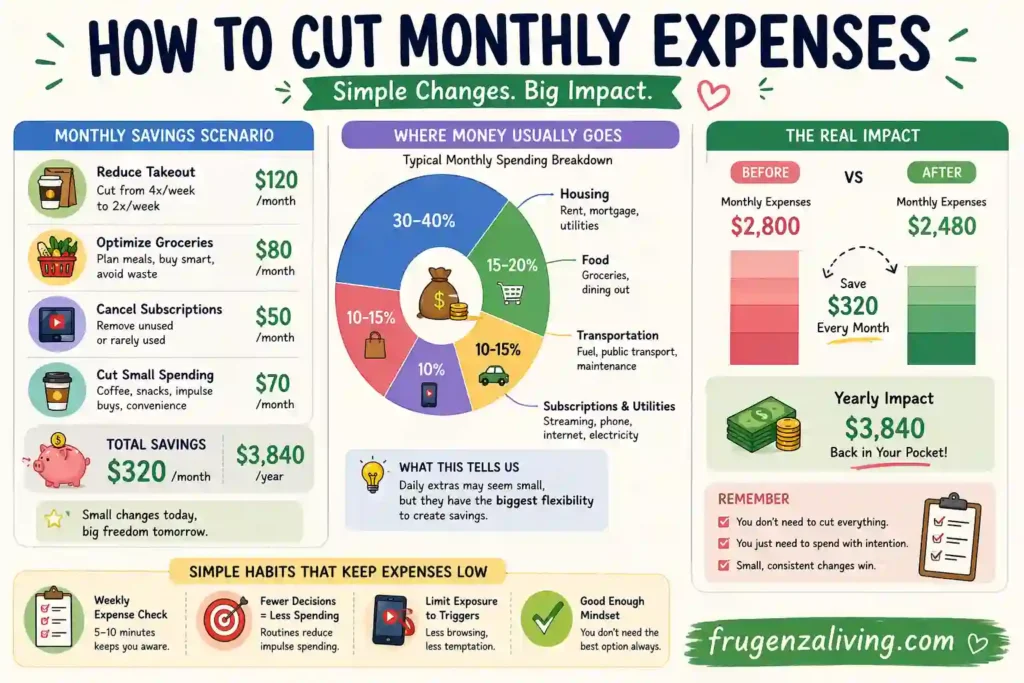

A Realistic Monthly Savings Scenario

Let’s combine a few small changes:

- Reduce takeout → save $120/month

- Adjust groceries → save $80/month

- Cancel subscriptions → save $50/month

- Cut daily small spending → save $70/month

Total: around $320/month

Yearly: nearly $4,000

That’s not extreme.

That’s just being slightly more intentional. This becomes even more effective when you focus on how to reduce your overall living costs.

A Simple Breakdown of Where Money Usually Goes

Most people don’t need complex data.

A rough estimate already explains a lot.

Typical monthly spending might look like:

- Housing: ~30–40%

- Food: ~15–20%

- Transport: ~10–15%

- Subscriptions & utilities: ~10%

- Daily extras: ~10–15%

Here’s the interesting part:

The “daily extras” category is often the most flexible

It’s also the most ignored

That’s where most unnecessary spending happens.

Not big purchases—small repeated ones.

Over time, you’ll naturally learn how to live on less money without sacrificing your comfort.

Simple Habits That Keep Expenses Low

This is what actually keeps things under control long-term.

Not big changes—just small routines.

Weekly Expense Check

5–10 minutes is enough.

No stress. Just awareness.

Fewer Decisions = Less Spending

Simple routines reduce impulse decisions.

Same meals, same stores, same habits.

Limit Exposure to Spending Triggers

Less browsing means less temptation.

Keep a “Good Enough” Mindset

You don’t need the best option every time.

These habits don’t feel intense. That’s why they work.

Common Mistakes When Trying to Cut Expenses

Being Too Extreme

Cutting everything feels powerful… until it becomes exhausting.

Changing Everything at Once

Too many changes = burnout.

Ignoring Small Expenses

This is where most money leaks happen.

Expecting Instant Results

Savings build gradually, not overnight.

Final Thoughts

Learning how to cut monthly expenses does not mean you need to overhaul your entire life. Most of the time, the best results come from small adjustments that are easy to repeat.

Start with one category. Review one bill. Cancel one unused subscription. Reduce one spending habit that happens too often. Set one simple limit for groceries, takeout, or personal spending.

These changes may not feel dramatic, but they become powerful when they repeat every month.

The goal is not perfection. The goal is to make your money go further while keeping the parts of your life that actually matter.

When you cut expenses with intention instead of pressure, saving money becomes much more sustainable.

The ideas shared here come from real-life experience and practical habits that actually work.

→ Read more about Jeffi

- How to Split Bills Between Paychecks Without Overloading One Check - August 9, 2026

- Subscription Audit Checklist: Find and Review Every Recurring Charge - August 9, 2026

- How to Budget for Subscriptions Without Surprise Renewals - August 7, 2026