I didn’t realize how much I was overspending until I actually looked at it.

Not in a detailed spreadsheet way. Just… a quick glance at my bank app.

And yeah—nothing big stood out. No crazy purchases. Just small stuff. Food here, subscriptions there, random online buys I barely remembered.

That’s the tricky part.

If you’re trying to figure out how to reduce unnecessary spending, you’re probably not wasting money on obvious things. It’s the quiet, everyday spending that adds up—and somehow slips by unnoticed.

Let’s break this down in a way that actually works in real life.

The goal is not to become strict with every dollar or feel guilty every time you spend money.

The goal is to understand which purchases are helping your life and which ones are quietly draining your budget without giving much value back.

In this guide, you’ll learn how to reduce unnecessary spending by spotting emotional triggers, separating useful spending from wasteful spending, using simple pause rules, and replacing automatic purchases with more intentional choices.

You do not need to cut everything. You only need to stop spending without noticing.

What Is “Unnecessary Spending,” Really?

Unnecessary spending is money you spend out of habit, convenience, or impulse—without it adding real value to your life.

That doesn’t mean it’s “bad.”

It just means:

- You didn’t really plan it

- You didn’t fully need it

- You might not even remember it later

Reducing it doesn’t mean cutting everything.

It means:

Keeping what matters

Cutting what doesn’t

That’s it.

The Necessary vs. Unnecessary Spending Filter

Unnecessary Spending Decision Map

Not every non-essential purchase is bad. Use this simple map to decide what to keep, what to reduce, and what to remove so you can spend more intentionally without feeling restricted.

Keep

Keep purchases that support your health, work, relationships, peace of mind, or daily stability.

Reduce

Reduce purchases you enjoy but buy too often, such as takeout, snacks, coffee, convenience items, or online shopping.

Remove

Remove expenses you barely use, forgot about, or only keep out of habit, such as unused subscriptions or random fees.

Common Spending Triggers and Better Replacements

Not every non-essential purchase is unnecessary. A small coffee with a friend, a helpful shortcut during a busy week, or something that improves your health, work, or relationships can still have real value.

The problem is not spending money on anything enjoyable. The problem is spending money automatically without asking whether it still matters.

Before buying something, ask three simple questions: Do I need this now? Will I still care about this purchase next week? Does this fit my current budget or am I just reacting to stress, boredom, or convenience?

If the purchase adds value and fits your budget, it may be worth keeping. If it only gives a quick feeling but creates regret later, it is probably unnecessary spending.

This filter helps you reduce waste without turning your life into a strict no-spend challenge.

Why You Keep Spending More Than You Should

To be honest, overspending isn’t really about money.

It’s about behavior.

1. Emotional Triggers

You’re tired. Stressed. Bored.

So you:

- Order food

- Scroll and buy something small

- Treat yourself “just this once”

I’ve done this more times than I’d like to admit.

2. Convenience Habits

Convenience is expensive.

- Delivery instead of cooking

- Pre-made food instead of groceries

- Quick purchases instead of thinking

It feels small in the moment. But it adds up fast.

3. Lifestyle Creep

This one’s subtle.

As your income (or comfort level) grows, your spending quietly grows too.

You don’t notice it—until things feel tight again.

If you want a structured approach, this frugal living guide for beginners covers everything step by step.

The Spending Trigger Map

One of the easiest ways to reduce unnecessary spending is to identify what usually happens right before you spend.

Most unnecessary purchases have a trigger. You may spend when you are tired, stressed, bored, rushed, hungry, lonely, or scrolling online without a plan.

For example, tired spending often turns into takeout. Bored spending often turns into online shopping.

Rushed spending often turns into convenience purchases. Stress spending often turns into small “treat yourself” purchases that feel good for a moment but do not actually solve the problem.

Instead of blaming yourself, start noticing the pattern. Ask yourself: “What was I feeling before I bought this?”

Once you understand the trigger, you can create a better replacement. If tired nights lead to delivery, keep two easy backup meals at home. If scrolling leads to shopping, remove shopping apps from your home screen or wait 24 hours before buying.

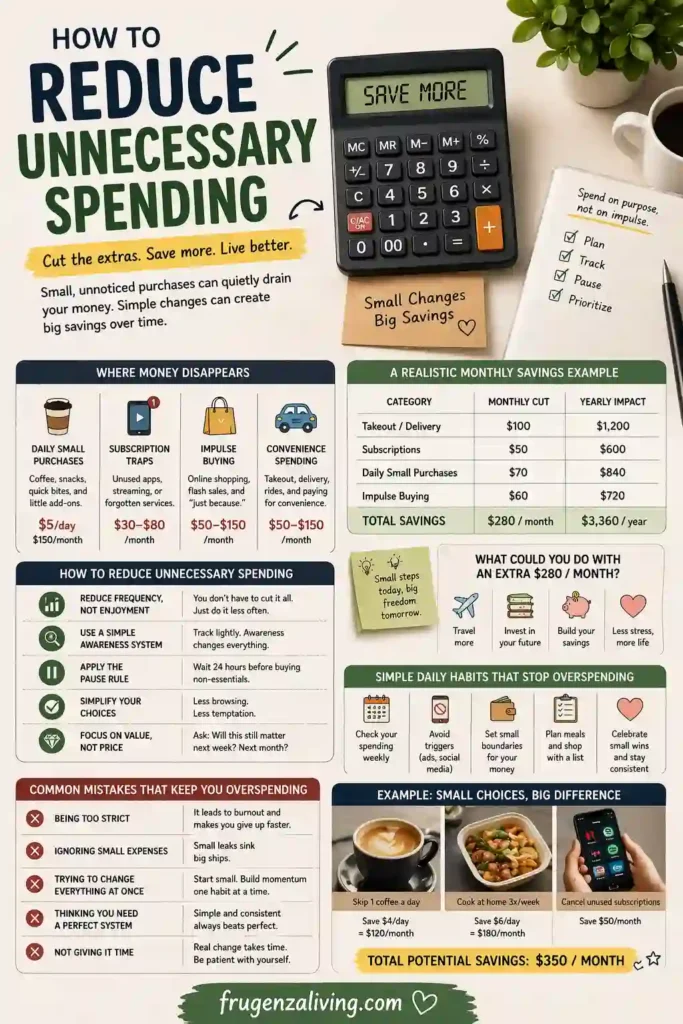

Where Unnecessary Spending Usually Happens

You’ve probably done this without thinking.

Most unnecessary spending isn’t obvious.

Common areas:

- Small daily purchases

Coffee, snacks, little extras - Subscription traps

Streaming, apps, services you forgot about - Impulse buying

Especially online—just a few clicks - Convenience spending

Takeout, delivery, “I don’t feel like cooking” moments

Individually, these feel harmless.

Together? They quietly drain your budget.

The easiest place to start is with repeated spending, not one-time purchases. A single small purchase is rarely the real problem.

The bigger problem is a habit that repeats every day, every week, or every month without adding enough value.

Look for expenses that show up again and again: delivery fees, snacks, app subscriptions, random online orders, convenience food, small upgrades, and items you buy because they are on sale. These are the purchases that can quietly turn into a serious budget leak over time.

A helpful rule is this: if you do not remember buying it, do not use it often, or would not choose it again today, it may be unnecessary spending.

How to Reduce Unnecessary Spending Without Feeling Restricted

This is where things usually go wrong.

People try to cut everything at once—and it backfires.

So instead, let’s keep this realistic.

Try these instead:

- Reduce frequency, not enjoyment

Still order takeout—just not as often - Use light awareness (not strict tracking)

Check your spending once a week

That alone changes behavior - Apply the “pause rule”

Before buying something, wait a bit

You’ll be surprised how often the urge disappears - Simplify your choices

Less browsing = less spending - Focus on value, not price

Ask: “Is this actually worth it for me?”

A simple budgeting method can help you avoid unnecessary purchases.

To be honest, most of my unnecessary spending stopped when I simply started noticing it.

Not controlling it. Just noticing. For example, learning how to reduce grocery spending can immediately lower your expenses.

Replace, Don’t Just Remove

Cutting unnecessary spending works better when you replace the habit instead of only removing it. If you only tell yourself “stop spending,” you may feel restricted. But if you create an easier replacement, the habit becomes more realistic.

If you order takeout because you are tired, replace it with a simple emergency meal at home. If you buy things online when you are bored, replace the habit with a saved wishlist and a 24-hour waiting rule.

If you spend money when you feel stressed, replace the purchase with a low-cost reset like a walk, shower, journaling, or making a cup of coffee at home.

This matters because unnecessary spending is often emotional or automatic. A replacement habit gives your brain another option before money leaves your account.

A Realistic Monthly Savings Example

Let’s make this concrete.

Say you adjust a few habits:

- Takeout: save $100/month

- Subscriptions: save $50/month

- Small daily purchases: save $70/month

- Impulse buying: save $60/month

👉 Total: ~$280/month

👉 In a year: over $3,300

And that’s without extreme budgeting.

Just small changes. One of the first steps is to reduce your daily expenses and identify small leaks in your budget.

Simple Daily Habits That Stop Overspending

This is where things start to feel easier.

Not big changes. Just repeatable habits.

Try this:

- Weekly spending check (5–10 minutes)

Just look. No pressure - Avoid your triggers

If scrolling leads to spending… scroll less - Set small boundaries

Example: no random purchases during weekdays - Stick to a simple routine

Same meals, same shopping habits - Ask one simple question:

👉 “Do I actually need this right now?”

I’ve noticed this adds up quickly. Not just in savings—but in control.

This becomes easier when you learn how to stop wasting money in your daily life.

The Part Most People Ignore: Awareness

Here’s something that changed everything for me.

I stopped trying to control my spending.

And started trying to understand it.

Once you see patterns, things get easier.

You don’t need discipline for everything.

You just need awareness.

A 7-Day Spending Awareness Challenge

If you do not want to track every expense forever, try a simple 7-day spending awareness challenge.

For one week, check your spending once a day and write down only three things: what you bought, why you bought it, and whether it was worth it.

At the end of the week, look for patterns. Did you spend when you were tired? Did online browsing lead to purchases?

Did convenience spending show up more than once? Did any subscription or small charge surprise you?

This challenge is useful because it focuses on awareness, not guilt. You are not trying to judge every purchase.

You are trying to understand which spending habits are worth keeping and which ones are quietly draining your money.

Common Mistakes That Keep You Overspending

I made all of these at some point.

1. Being Too Strict

Cutting everything feels powerful… for a few days.

Then it gets exhausting.

2. Ignoring Small Expenses

This is usually the biggest issue.

Small spending feels invisible—but it’s not.

3. Trying to Change Everything at Once

Too many changes = overwhelm.

4. Thinking You Need a Perfect System

You don’t.

Simple works better.

5. Not Giving It Time

This isn’t instant.

But it does get easier. Over time, you’ll naturally learn how to adjust your lifestyle without feeling restricted.

How This Connects to Bigger Money Habits

Reducing unnecessary spending isn’t just one habit.

It connects to everything else:

- Saving money on groceries

You buy less, waste less - Budgeting basics

You become more aware of your money - Reducing monthly bills

You start questioning what you really need - Simple money habits

Everything becomes easier to manage

It all builds on itself.

FAQ: How to Reduce Unnecessary Spending

What is unnecessary spending?

Unnecessary spending is money spent on things that don’t add real value and are often driven by habits, convenience, or impulse.

How can I stop unnecessary spending quickly?

Start by becoming aware of your daily spending and reducing small purchases instead of cutting everything at once.

Do I need to track every expense?

No. A simple weekly check is usually enough to build awareness and improve habits.

Why do I keep overspending even when I try to stop?

Because overspending is often linked to habits and emotions, not just lack of discipline.

Can I still enjoy life while cutting spending?

Yes. The goal is balance—keeping what matters while removing what doesn’t.

Final Thoughts

Learning how to reduce unnecessary spending is not about becoming perfect with money. It is about noticing the purchases that happen automatically and deciding which ones still deserve space in your life.

Start small. Review one week of spending, cancel one thing you do not use, pause one impulse purchase, or replace one convenience habit with an easier low-cost option.

Small changes are easier to repeat, and repeated changes are what create real progress.

You do not need to cut everything to take control of your money. You only need to spend more intentionally, reduce what does not matter, and keep building awareness one decision at a time.

The ideas shared here come from real-life experience and practical habits that actually work.

→ Read more about Jeffi

- How to Split Bills Between Paychecks Without Overloading One Check - August 9, 2026

- Subscription Audit Checklist: Find and Review Every Recurring Charge - August 9, 2026

- How to Budget for Subscriptions Without Surprise Renewals - August 7, 2026