Payday is supposed to feel like relief. But sometimes the money hits your account, bills go out, groceries still need to be bought, gas is low, and your balance already feels uncomfortable.

If that sounds familiar, you are not alone. Many people search for budgeting tips when broke after payday because the problem does not always feel like careless spending. Sometimes it feels like your paycheck disappears before you even get a chance to breathe.

You may still be paying your bills, but your usable money disappears too early.

The goal is not to build a perfect budget today. The goal is to stop the cash-flow panic, protect what matters most, and make your money last until the next payday.

Being broke after payday is often not a discipline problem. It is usually a cash-flow timing problem.

Editor’s note: This article is for general budgeting education only. It is not personalized financial, debt, tax, or investment advice. If you are behind on essential bills or debt payments, consider contacting your provider, lender, or a qualified nonprofit credit counselor.

Why You Feel Broke After Payday

If you feel broke right after payday, it usually comes from one or more pressure points.

Your fixed bills may be clustered too close to payday. Debt payments may take most of the paycheck before food, gas, or household basics are funded. Automatic subscriptions may quietly drain your account. Groceries and transportation may cost more than you planned.

For example, you might pay rent, a car payment, insurance, and two subscriptions within three days of payday. On paper, you “paid the bills.” In real life, you still need groceries, gas, medication, and basic household items before the next paycheck.

That gap is the broke-after-payday problem.

The problem is not always that you have no budget. Sometimes the budget ends on payday, but real life continues until the next paycheck. That is why you need a short-term reset, not another complicated spreadsheet.

If you often feel broke right after getting paid, the first step is learning how to organize money after payday before spending starts.

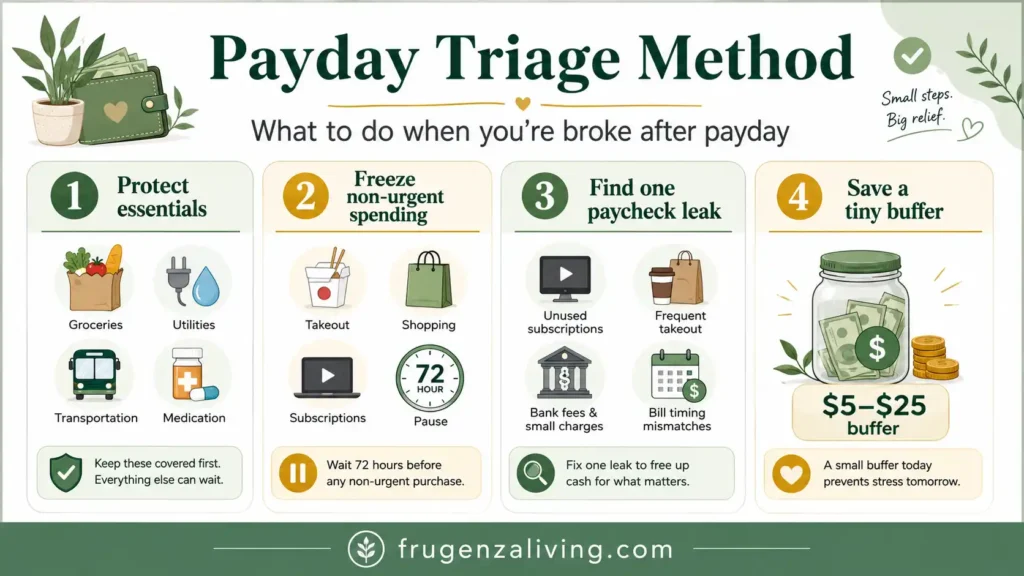

Budgeting Tips When Broke After Payday: Start With Triage

When money is tight, the first goal is not optimization. The first goal is stabilization.

That is where the Payday Triage Method helps.

Triage means you do not try to fix everything at once. You decide what needs attention first, what can wait, and what would create the most damage if ignored. When money is tight after payday, that order matters more than a perfect monthly budget.

The Payday Triage Method has four steps:

- Protect essentials.

- Pause non-urgent spending.

- Find one paycheck leak.

- Build a small next-payday buffer.

One way to stop feeling broke after payday is to split paycheck before spending instead of using one mixed balance.

Step 1: Protect the Next 7 Days First

When you are broke right after payday, do not start by planning the whole month. Start with the next 7 days.

Ask one question:

What must be covered before the next payday?

List the basics:

- food

- gas or transportation

- medication

- utilities due soon

- childcare or school needs

- bank fees or overdraft risks

- required minimum payments when essentials are already protected

If the next 7 days are not covered, your budget is still exposed. This does not mean long-term goals do not matter. It means survival expenses come first when money is tight.

Step 2: Create a Bare-Minimum Payday Plan

A bare-minimum payday plan is not your forever budget. It is a temporary plan for tight weeks.

Use the must-pay, must-eat, must-move framework.

This keeps your payday budget simple when your brain is already stressed.

If your paycheck disappears too quickly, a simple paycheck budget template can help you separate bills, savings, debt, and spending money.

Step 3: Use a 72-Hour Spending Freeze

A spending freeze does not have to be extreme. It just needs to be short and clear.

For the next 72 hours, pause takeout, online orders, payday reward purchases, new subscriptions, non-urgent upgrades, and convenience spending.

This is not punishment. It is breathing space.

The first few days after payday are when money can disappear fast. A short freeze helps you see what is actually left after essentials, instead of letting the paycheck leak through small purchases.

Step 4: Find One Paycheck Leak

Do not try to fix your entire budget at once. Find one leak this payday.

Your paycheck leak might be a bill timing leak, subscription leak, food leak, debt payment leak, overdraft fee leak, transportation leak, or emotional payday spending leak.

For example, if $60 of takeout happens every payday weekend, fixing that one leak may create more relief than trying to overhaul your entire budget.

If your problem is bill timing, ask whether one due date can be moved. If subscriptions are the issue, cancel one today. If groceries are the leak, plan three simple meals before shopping again.

One fixed leak is better than ten ideas you never use.

It becomes easier to stay in control when you divide your income for budgeting into bills, savings, debt, and flexible spending.

Step 5: Call Before You Miss a Payment

If you cannot cover an essential bill, call before the due date when possible.

You may be able to ask about a payment plan, due date change, short extension, hardship option, lower-cost plan, or downgrade.

Not every company will say yes, but asking early gives you more options than waiting until the payment is already missed.

If they offer an extension or payment plan, ask whether there are fees, interest, late marks, or service interruptions. Write down the date, the name of the representative, and the agreement details.

The Consumer Financial Protection Bureau offers resources for dealing with debt and understanding your rights if bills or collections become overwhelming.

The goal is not to avoid responsibility. The goal is to reduce damage and make a realistic plan.

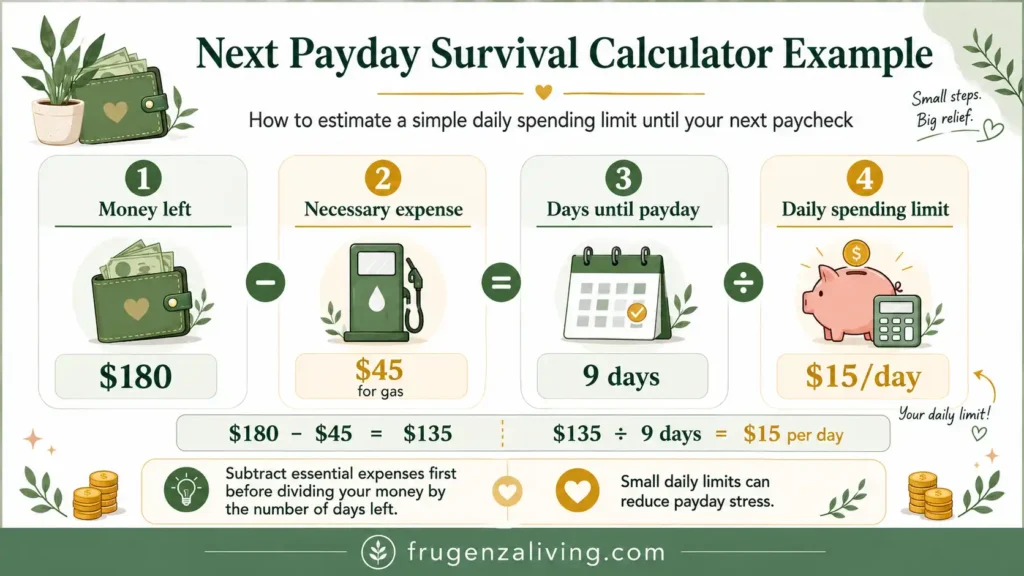

Step 6: Make Your Paycheck Last Until Next Payday

Once essentials are covered, divide your remaining money by the number of days until your next paycheck.

For example, if you have $180 left and 9 days until payday, your daily spending limit is $20. But if you need gas in three days, subtract that first.

So if gas will cost $45, the real math is:

$180 – $45 = $135

$135 ÷ 9 days = $15 per day

Use the calculator below to estimate your daily spending limit.

“`htmlNext Payday Survival Calculator

Use this simple calculator to estimate how much you can spend per day until your next payday.

This calculator is for general budgeting education only. Adjust the numbers based on your real bills, food, transportation, and essential needs.

You can also separate grocery money from bill money, use a no-spend list, cook from your pantry first, and keep a tiny untouched amount as a mini buffer.

Step 7: Build a Tiny Next-Payday Buffer

If you are broke after payday, saving 20% may not feel realistic right now.

Start smaller:

- $5 per payday

- $10 per payday

- $25 per payday

- leftover grocery money

- one skipped takeout meal

Even a small buffer can help reduce the chance that a minor expense becomes a bigger problem. The Consumer Financial Protection Bureau describes emergency savings as money set aside for unplanned expenses or financial emergencies.

A small buffer will not fix everything, but it can change the pattern. The goal is to arrive at the next payday with something left, even if it is small.

If you are not sure why your money disappears, start by learning how to track expenses easily for a few weeks.

What Not to Do When You Are Broke After Payday

Avoid these common mistakes.

Do not ignore bills and hope they disappear.

If you cannot pay, contact the provider early.

Do not use credit cards for comfort spending.

Credit cards may help in emergencies, but using them for emotional relief can make next payday harder.

Do not start a complex budget you cannot maintain.

When money is tight, simple is better.

Do not cancel every joy item and rebound-spend later.

Extreme restriction can backfire. Keep the plan realistic.

Do not compare your budget to someone else’s.

Your rent, income, debt, family size, and bills are not the same as theirs.

Do not rely on payday loans as a routine solution.

If you are considering a payday loan, pause and look for lower-cost options first, such as a payment plan, local assistance program, employer advance policy, credit union alternative, or nonprofit credit counseling. High-cost short-term borrowing can make the next payday even harder.

A Simple 7-Day Reset Plan When You Are Broke After Payday

Use this reset when payday already feels stressful.

Your rule might be simple: buy groceries before takeout, check bills before shopping, keep $10 untouched, or wait 72 hours before payday reward spending.

Where This Fits in Your Bigger Budget

This reset is for the moment when payday already feels tight.

Once the next 7 days are protected, choose one tool for the problem you keep repeating. If payday feels chaotic, build a simple payday routine. If you need structure, use a paycheck budget template. If bills are scattered across the month, a biweekly paycheck budget may help.

If daily spending is the leak, a cash envelope system can help. If predictable expenses keep hurting you, sinking funds may be the better next step.

Final Thoughts

Being broke after payday does not mean you failed. It means your money needs a better order.

Start with essentials. Pause non-urgent spending. Find one paycheck leak. Call before missing important payments. Then build a tiny buffer before the next payday, even if it is only $5.

The goal is not a perfect budget. The goal is to make the next payday less stressful than this one.

FAQ

Why am I broke after payday?

You may feel broke after payday because bills, debt payments, subscriptions, groceries, gas, and small payday purchases happen too close together. It is often a cash-flow timing problem, not just a discipline problem.

What should I pay first when I am broke after payday?

Pay essentials first: housing, utilities, food, transportation, medication, insurance, and required payments when possible. Non-urgent spending should wait until these are protected.

How do I budget when I have no money left after bills?

Start with a bare-minimum plan. Cover must-pay, must-eat, and must-move expenses first. Then look for one paycheck leak, such as subscriptions, food spending, fees, or bill timing.

How can I survive until next payday?

List what you have left, subtract any necessary expenses like gas or food, then divide the rest by the number of days until payday. Use a short spending freeze and pantry meals to stretch your money.

Should I save money if I am broke after payday?

Yes, but start very small. Even $5 to $25 per payday can help you build a tiny buffer and begin breaking the cycle of having nothing left before the next paycheck.

How do I stop being broke after every payday?

Protect essentials first, pause non-urgent spending for 72 hours, fix one paycheck leak at a time, and build a small next-payday buffer. Over time, connect this reset with a regular paycheck budget.

The ideas shared here come from real-life experience and practical habits that actually work.

→ Read more about Jeffi

- How to Split Bills Between Paychecks Without Overloading One Check - August 9, 2026

- Subscription Audit Checklist: Find and Review Every Recurring Charge - August 9, 2026

- How to Budget for Subscriptions Without Surprise Renewals - August 7, 2026