Knowing you should save money is easy. Knowing exactly how much of each paycheck should go to bills, savings, debt, spending, and future expenses is harder.

That is why a paycheck breakdown percentage can help. Instead of waiting to see what is left at the end of the pay period, you give your paycheck a clear direction as soon as it arrives.

But your percentage plan should be a starting dial, not a strict rule.

The popular 50/30/20 rule can be useful, but it does not fit every income, rent payment, debt load, family size, or cost of living. A realistic paycheck breakdown should match your actual take-home pay, not an ideal budget that only works on paper.

Editor’s note: This article is for general budgeting education only. It is not personalized financial, debt, tax, or investment advice. Use these paycheck percentages as flexible starting points and adjust them based on your real bills, income, and priorities.

What Is a Paycheck Breakdown Percentage?

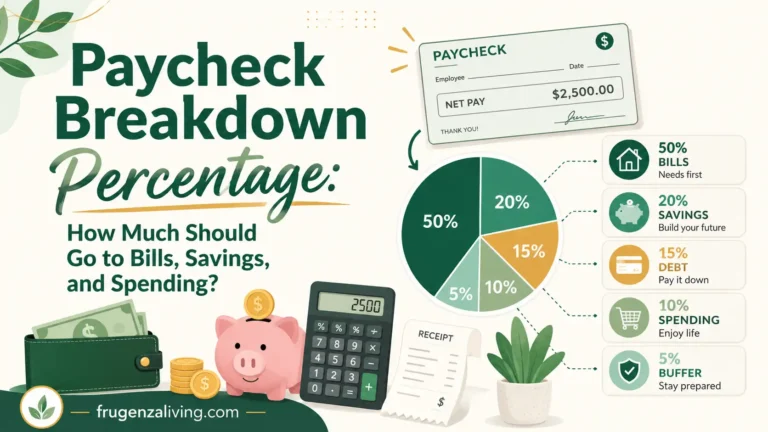

A paycheck breakdown percentage is a way to divide your take-home pay into categories before the money disappears.

For example, instead of saying, “I will save whatever is left,” you might decide that every paycheck gets divided into essentials, savings, debt payoff, lifestyle spending, and a buffer.

Use your after-tax income, also called take-home pay. This is the money that actually reaches your bank account after taxes and paycheck deductions.

A simple paycheck percentage plan might look like this:

- 50% essentials

- 20% savings and debt

- 20% flexible spending

- 10% buffer or future expenses

But if your bills are high, a 60/20/10/10 or 70/10/10/10 split may be more realistic. The goal is not to copy a rule perfectly. The goal is to make sure every paycheck has a job.

A paycheck breakdown percentage is easier to use when you already know how to split income for budgeting across bills, savings, debt, and spending.

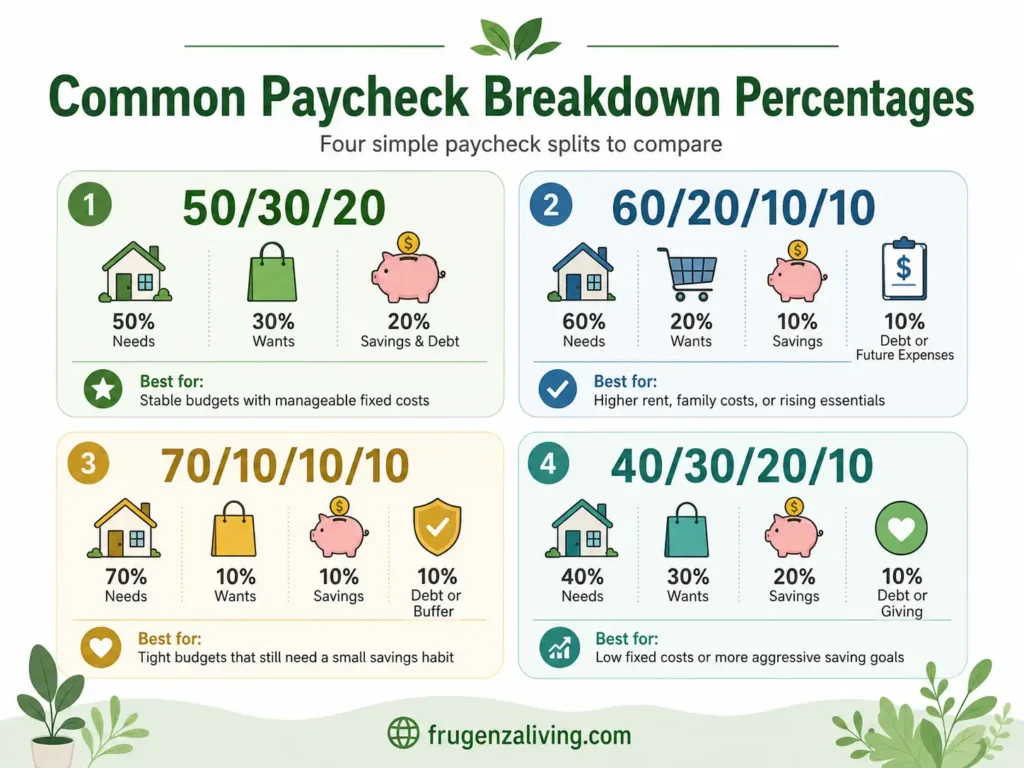

Why 50/30/20 Does Not Work for Everyone

The 50/30/20 rule is popular because it is simple: 50% for needs, 30% for wants, and 20% for savings and debt.

For many people, that is a helpful starting point.

But it does not work perfectly for everyone.

If you live in a high-rent area, support a family, have childcare costs, carry high-interest debt, or earn a lower income, your needs may take more than 50% of your paycheck. That does not mean you failed. It means your paycheck breakdown percentage needs to reflect reality.

A budget that looks perfect but fails every payday is not useful.

The Take-Home Reality Method

Instead of forcing your paycheck into one popular rule, start with what your take-home pay must actually cover.

That is the idea behind the Take-Home Reality Method.

This method is useful because it does not shame you for having high bills. It helps you build a paycheck percentage plan you can actually follow.

If your paycheck disappears quickly, a percentage-based breakdown can show whether too much money is going to flexible spending.

Common Paycheck Breakdown Percentages

There is no single best way to split your paycheck. Use these models as starting points, then adjust them to your real life.

After choosing your percentages, a paycheck budget template can help you turn those numbers into an actual plan.

Paycheck Breakdown Percentage Calculator

Use this calculator to test different paycheck percentage plans based on your take-home pay.

Paycheck Breakdown Percentage Calculator

Enter your take-home paycheck amount and choose a percentage plan to see how much should go to bills, savings, debt, spending, and buffer money.

This calculator is for general budgeting education only. Adjust the numbers based on your real bills, income, debt, and savings goals.

A Realistic Paycheck Breakdown for Saving Money

If your main goal is to save money from every paycheck, the most important category is your savings floor.

A savings floor is the smallest percentage you can save consistently. It may be 20%, but it might also be 10%, 5%, or even 1–3% while money is tight.

A realistic paycheck breakdown might look like this:

- 50–60% essentials

- 5–20% savings

- 5–15% debt payoff

- 10–25% lifestyle spending

- 5–10% buffer or sinking funds

Essentials include housing, utilities, groceries, transportation, insurance, phone, childcare, and required bills. If this category is above 60%, keep wants lower and protect a small savings habit.

Savings does not have to start at 20%. If 20% feels impossible, start with 5%. If even 5% is too much, start with 1–3%. For example, 3% of a $1,200 paycheck is $36. That may not feel huge, but it is better than waiting for a perfect month to start saving. The Consumer Financial Protection Bureau describes emergency savings as money set aside for unplanned expenses or financial emergencies.

Debt payoff may need 5–15% of your paycheck if high-interest debt is adding pressure. This is general education, not personal financial advice.

Lifestyle spending includes takeout, entertainment, shopping, hobbies, and nonessential purchases. A clear cap gives you room to enjoy money without letting wants absorb the entire paycheck.

Buffer or sinking funds help with expenses that do not happen every payday, such as car maintenance, annual bills, holidays, school costs, medical co-pays, and home repairs.

Your paycheck breakdown becomes more accurate when you know your average monthly income from biweekly pay.

Paycheck Breakdown Percentage for Low Income

If your income is tight, the goal is not to force a perfect budget percentage. The goal is to protect essentials, save something small, and reduce one pressure point at a time.

A low-income paycheck breakdown might look like this:

- 70% essentials

- 5% savings floor

- 5–10% debt or required payments

- 10% lifestyle or household basics

- 5–10% buffer

If essentials take 80% or more, do not use that as a reason to give up. Start with the smallest repeatable savings floor and focus on one pressure point: lowering one bill, reducing one fee, pausing one unused subscription, or building a $10–$25 cushion.

Small progress still counts when money is tight.

If weekly pay feels hard to control, a weekly paycheck breakdown can show how much should go to bills, savings, and spending.

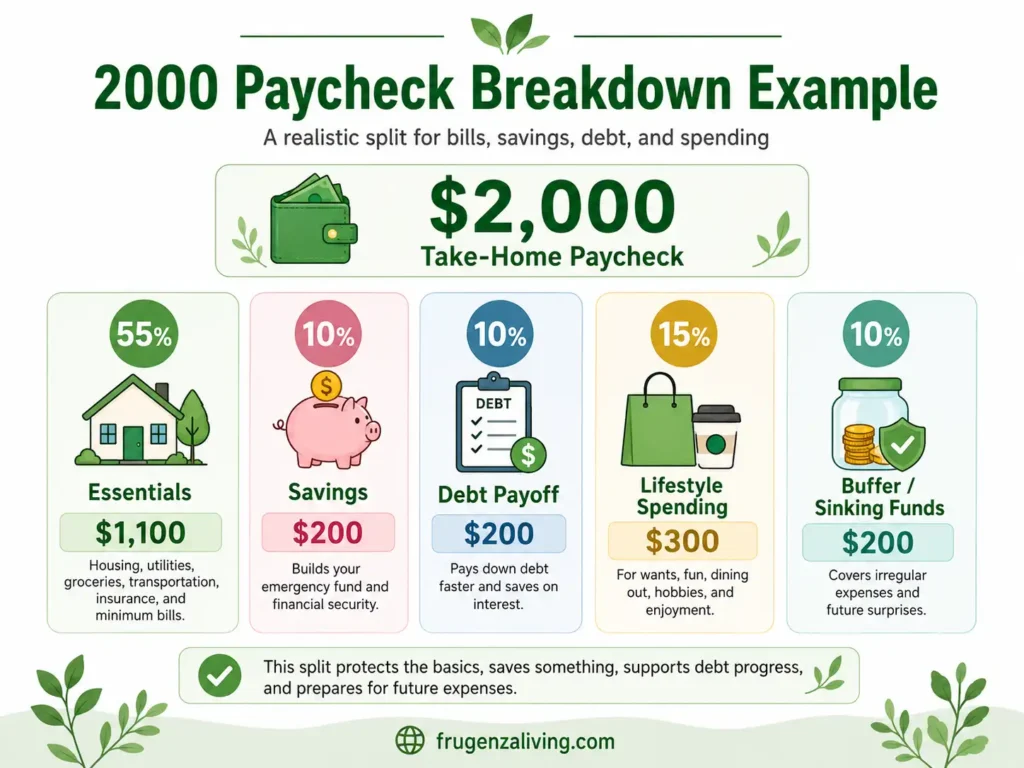

Example: Paycheck Breakdown Percentage for a $2,000 Paycheck

Here is a realistic example for someone who wants structure but cannot force a perfect 50/30/20 split.

This split protects the basics, saves something, makes debt progress, allows some flexible spending, and prepares for future expenses.

The 3 Reality Tests Before Choosing Percentages

Before choosing a paycheck percentage plan, run these three quick tests.

- The Rent Test: If housing and utilities already take 35–40% or more of your take-home pay, do not force 30% wants. Lower wants first and protect a small savings floor.

- The Savings Floor Test: If you cannot save 20%, choose a repeatable number. A 3% savings habit that happens every paycheck is better than a 20% goal you skip every month.

- The Leak Test: If your paycheck disappears even when the percentages look fine, separate lifestyle spending and buffer money. The problem may be category mixing, not income.

How to Adjust Your Paycheck Percentages

Your paycheck breakdown should change when your pressure points change.

If bills take more than 60% of your paycheck, reduce wants first before cutting savings to zero. If high-interest debt is growing, shift more toward debt temporarily. If you have no emergency fund, protect a small savings floor.

Mistakes to Avoid With Paycheck Percentage Breakdowns

Avoid these common mistakes:

- Using gross income instead of take-home pay. Your budget should match the money you actually receive.

- Forcing 50/30/20 when bills are too high. A realistic plan is better than a perfect rule you cannot follow.

- Saving only what is left over. Savings should have a planned percentage, even if it starts small.

- Forgetting irregular expenses. Annual bills, repairs, holidays, and medical costs need a place in your paycheck plan.

- Giving wants too much room. Lifestyle spending needs a cap so small purchases do not absorb the paycheck.

Where This Fits in Your Bigger Budget

This article helps you choose percentage targets. A paycheck budget template helps you turn those targets into exact bill payments and category amounts.

If you are paid biweekly, a biweekly paycheck budget can help you time those categories around each payday. If future expenses keep surprising you, sinking funds can give those expenses a place before they become emergencies. If daily spending is hard to control, cash envelopes can help limit flexible categories.

Choose the tool that solves your biggest problem first.

Final Thoughts

The best paycheck breakdown percentage is the one that fits your real take-home pay and helps you save consistently.

Start with a realistic split. Protect essentials. Choose a savings floor. Cap lifestyle spending. Adjust debt, savings, and future expenses based on your pressure points.

A flexible paycheck percentage plan is better than a perfect rule you cannot follow.

FAQ

What is a good paycheck breakdown percentage?

A good starting paycheck breakdown is 50% needs, 20% savings and debt, 20% flexible spending, and 10% buffer or future expenses. If bills are high, a 60/20/10/10 or 70/10/10/10 split may be more realistic.

What percentage of my paycheck should go to savings?

A common goal is 20%, but many people need to start smaller. If 20% is not realistic, try 5% or even 1–3% and increase it over time.

Should I use 50/30/20 for every paycheck?

Not always. The 50/30/20 rule is useful, but it may not fit high rent, low income, childcare, heavy debt, or irregular expenses. Use it as a starting point, not a strict rule.

What percentage of paycheck should go to bills?

Many people aim to keep essential bills around 50–60% of take-home pay. If bills take more than that, reduce lifestyle spending first and keep at least a small savings floor when possible.

What percentage of my paycheck should go to rent?

Many people try to keep rent or housing below 30% of take-home pay, but that is not realistic for everyone. If housing and utilities are above 35–40%, reduce wants first, protect essentials, and keep a small savings floor when possible.

How do I split my paycheck if money is tight?

If money is tight, try a 70/10/10/10 split: 70% needs, 10% wants, 10% savings, and 10% debt or buffer. Adjust based on your real bills and priorities.

Should paycheck percentages be based on gross or net income?

Use net income, or take-home pay, for paycheck percentages. This gives you a more accurate plan because it is based on the money you actually receive.

The ideas shared here come from real-life experience and practical habits that actually work.

→ Read more about Jeffi

- How to Split Bills Between Paychecks Without Overloading One Check - August 9, 2026

- Subscription Audit Checklist: Find and Review Every Recurring Charge - August 9, 2026

- How to Budget for Subscriptions Without Surprise Renewals - August 7, 2026