You try to budget, promise yourself you will check your spending, and then life gets busy.

A bill comes out earlier than expected. Groceries cost more than planned. You forget to move money to savings. By the time you finally look at your account, the month already feels messy.

That is why learning how to build a simple financial routine matters.

The problem is not always that you do not know what to do with money. Many people already know they should budget, save, track spending, and pay bills on time.

The harder part is turning those tasks into a routine you can actually repeat.

A simple financial routine is not about perfection. It is about small money check-ins that keep you aware before things get chaotic.

What Is a Simple Financial Routine?

A simple financial routine is a repeatable set of money habits that helps you check income, bills, spending, savings, and goals on a regular schedule.

It can include a daily money glance, a weekly money reset, a payday routine, and a monthly budget review.

The goal is not to spend hours managing money. The goal is to create a rhythm that helps you notice problems early, make small adjustments, and stay consistent.

If you are learning how to build a simple financial routine, start with small actions you can repeat on normal busy weeks.

For beginners, a financial routine for beginners should feel small, repeatable, and easy to restart after a messy week.

A good personal finance routine is not built around perfect motivation. It is built around habits that still work during regular life.

Small routines are easier to maintain when they support simple money habits you can repeat daily.

Financial Plan vs. Financial Routine: What’s the Difference?

A financial plan tells your money where to go.

A financial routine helps you keep checking whether the plan is still working.

For example, a plan might say, “Save $100 this month.” The routine is checking your account, moving the money after payday, and reviewing whether that amount was realistic.

A plan might say, “Spend less on eating out.” The routine is looking at your recent spending once a week before the month gets out of control.

This difference matters because many people create a plan once, then never return to it.

A financial routine keeps the plan alive.

If you are still learning the basics of making a budget, the routine is what helps you return to the plan consistently instead of forgetting about it after one week.

A financial routine works better when it follows a simple money management plan you can repeat each month.

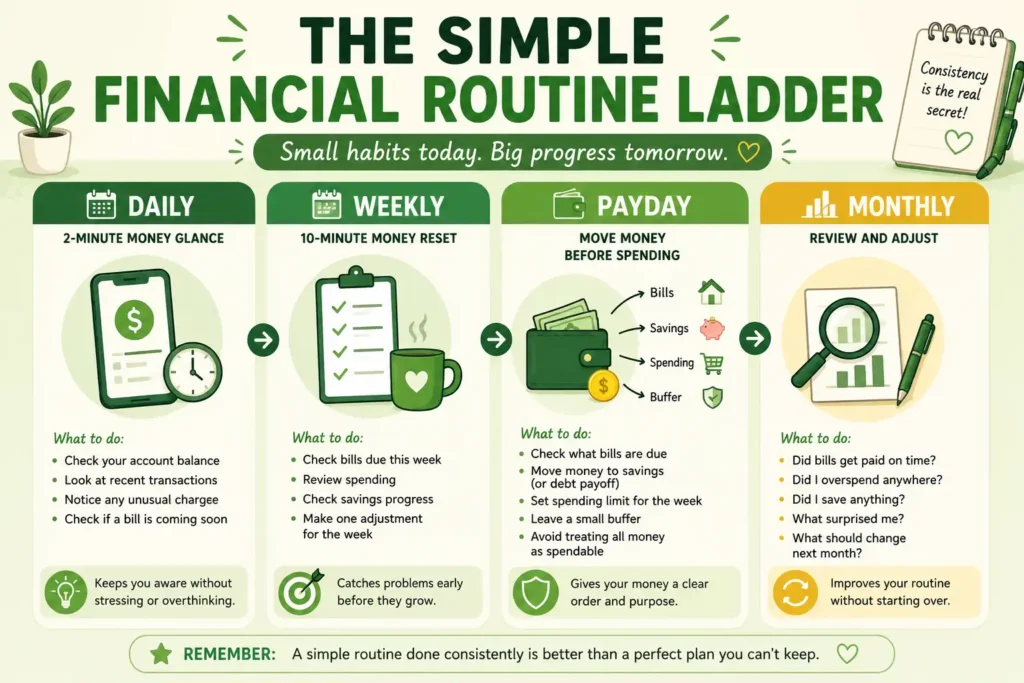

The Simple Financial Routine Ladder

A simple money routine works best when it has layers. You do not need to do everything every day.

Think of it like a routine ladder:

This ladder keeps your routine realistic. You are not trying to manage every detail every day.

You are simply checking the right things at the right time.

Step 1: Start With a 2-Minute Daily Money Glance

A daily money routine does not need to be intense.

You are not tracking every penny or judging every purchase. You are just staying aware.

A 2-minute money glance can include:

- checking your account balance

- looking at recent transactions

- noticing any unusual charge

- checking if a bill is coming soon

That is enough.

The goal is awareness, not anxiety. If checking your account daily makes you stressed, start with every other day or three times a week.

It can help to attach this habit to something you already do, like morning coffee, lunch break, or checking your calendar.

For example:

After you make coffee, open your banking app for two minutes.

That small habit keeps money visible without taking over your day.

Step 2: Create a 10-Minute Weekly Money Reset

A weekly money routine is where your financial routine starts becoming useful.

Once a week, take 10 minutes to check what happened and what needs attention.

During a weekly budget check-in, look at:

- bills due this week

- flexible spending left

- recent purchases

- savings progress

- anything that needs adjusting

You can do this on Sunday night, Monday morning, or payday evening. The exact day matters less than the repeat.

A weekly money reset helps you catch problems while they are still small.

If groceries ran high, you can make a simpler meal plan for the next few days. If you spent more than expected on eating out, you can slow down before the weekend.

This is how you stay consistent with money without waiting until the end of the month to panic.

Step 3: Build a Payday Routine

Payday is when your financial routine matters most.

When money arrives, it is easy to feel like you have more room than you really do. But some of that money may already belong to rent, utilities, debt payments, groceries, or savings goals.

Use this simple payday routine:

- Check what bills are due before your next payday.

- Move a small amount to savings or debt payoff.

- Set your flexible spending limit for the week.

- Leave a small buffer if possible.

- Avoid treating the full balance as spendable.

This is where the idea of pay yourself first can help. It simply means setting aside money for savings or goals before the rest disappears into daily spending.

It does not have to be a huge amount.

Even $10 or $20 moved on payday can build the habit of protecting future money.

A payday routine gives your money an order before the week gets busy.

Your routine should include a simple way to track your expenses so you know where your money is going.

Step 4: Do a Monthly Money Review

A monthly money routine gives you the bigger picture.

Once a month, look back and ask:

- Did bills get paid on time?

- Did I overspend in one category?

- Did I save anything?

- What expense surprised me?

- What should change next month?

This is not a time to shame yourself.

It is a time to learn.

Maybe your grocery estimate was too low. Maybe a subscription renewed. Maybe your flexible spending limit was unrealistic. Maybe you actually did better than you thought.

A monthly budget review helps your financial routine improve instead of becoming something you restart from zero every month.

A financial routine becomes stronger when you use a payday budgeting template every time money comes in.

A Simple Financial Routine Example for One Week

Here is what a simple financial routine might look like in real life.

Monday morning: Do a 2-minute balance check. Look at recent transactions and make sure nothing looks unusual.

Friday after payday: Check upcoming bills, move a small amount to savings, and set your weekly spending limit.

Sunday evening: Do a 10-minute weekly reset. Review spending, check what bills are due, and adjust the week ahead.

Last day of the month: Look at what worked, what felt hard, and what needs to change next month.

That is it.

You do not need a complicated routine to manage money consistently. You need a rhythm that keeps you from avoiding your finances for too long.

Simple Financial Routine Checklist

Use this checklist if you want the routine in one place:

- Daily: Check your balance and recent transactions.

- Weekly: Review bills, spending, and savings progress.

- Payday: Pay bills, move savings, and set spending limits.

- Monthly: Review what worked and adjust next month.

- Busy week: Do the minimum version instead of quitting.

This financial routine checklist keeps your money management routine simple without turning it into a second job.

The Minimum Version for Busy Weeks

Some weeks will be messy.

You might be tired, busy, traveling, sick, or just mentally full. That does not mean your financial routine has to disappear.

Use a minimum version.

When you do not have energy for the full routine, do only this:

- check your balance

- check the next bill

- avoid spending money already needed for bills

- move even $5 to savings if possible

This keeps the habit alive.

A simple financial routine should have a small version you can still do on hard weeks. Otherwise, one busy week can turn into a full month of avoidance.

The minimum version is not failure.

It is how the routine survives real life.

How to Make the Routine Stick

The easiest routine is one connected to something you already do.

This is sometimes called routine stacking.

Instead of saying, “I will manage my money more,” attach the task to a specific moment.

For example:

- after morning coffee, check your account

- after payday deposit, move savings

- Sunday evening, do a weekly reset

- after grocery shopping, update spending

- after paying rent, check upcoming bills

Keep the routine short at first. Use one app, one notebook, or one spreadsheet. Do not build a system so complicated that you avoid it.

If daily checking feels too much, start with weekly.

If weekly feels too much, start with payday.

Consistency grows when the routine feels small enough to repeat.

What to Do If You Miss the Routine

You will miss the routine sometimes.

That is normal.

Missing one check-in does not mean you failed. It just means you return to the smallest version.

Use this recovery loop:

Notice → Restart small → Adjust the reminder → Continue

If you missed the weekly reset, do a 5-minute version today.

If you forgot to save, move a smaller amount next payday.

If a bill surprised you, add it to your calendar.

If daily checking made you anxious, reduce it to a few times a week.

The goal is not to punish yourself into consistency. The goal is to make the routine easier to return to.

My Simple Financial Routine

I stopped waiting until something felt wrong to check my money.

That was a big shift.

Before, I would avoid looking when I felt unsure. Then I would feel more stressed because I had no idea what was happening.

What helped was building a small routine instead of trying to become perfect overnight.

I checked my account regularly. I gave payday an order. I moved some money before spending freely. I reviewed the week before it got too messy.

This simple routine became one of the habits that helped me save over $15,000 in a year.

Your numbers may look different, but having a routine can still make your money feel less chaotic.

For me, the real win was not having the perfect budget.

It was no longer avoiding my money until something went wrong.

How This Fits Into Your Budgeting System

A simple financial routine works best when it supports your broader budgeting system.

If you still need the bigger structure first, a simple money management plan for beginners can help you organize income, bills, spending, and future money.

If you are not sure where your money goes, learning how to track expenses easily can make this routine more accurate.

If you want a clearer category setup, a simple budget categories list can help you decide what to review each week.

If you need a realistic example, a monthly budget example for a single person can show how income and expenses might be divided.

FAQ

What is a simple financial routine?

A simple financial routine is a repeatable set of money habits that helps you check income, bills, spending, savings, and goals regularly. It can include a daily money glance, weekly reset, payday routine, and monthly review.

How do I build a simple financial routine?

Start small. Do a 2-minute money glance, schedule a 10-minute weekly reset, create a payday routine, and review your money once a month. The goal is to make money management repeatable, not perfect.

How often should I check my money?

You can check your money daily, weekly, and monthly depending on what feels manageable. A simple starting point is a 2-minute balance check a few times a week and a 10-minute weekly money reset.

What should I do every payday?

On payday, check upcoming bills, move a small amount to savings or debt payoff, set your flexible spending limit, and leave a small buffer if possible. Avoid treating the full balance as spendable.

What is a weekly money reset?

A weekly money reset is a short check-in where you review recent spending, upcoming bills, flexible spending left, and savings progress. It helps you catch problems before the month ends.

How do I stay consistent with budgeting?

Stay consistent by keeping the routine small, attaching it to an existing habit, and using reminders. If you miss a week, restart with a shorter version instead of quitting the routine completely.

What if I miss my financial routine?

If you miss your financial routine, restart small. Check your balance, look at the next bill, adjust one thing, and continue. Missing one routine does not mean you failed.

Final Thought: Make Money Management Repeatable

A simple financial routine does not need to be perfect.

It needs to be easy enough to repeat when life is busy.

Small check-ins, payday habits, and weekly resets can make money feel less chaotic. You do not have to fix everything at once.

Start with one small routine.

Then let consistency do the work.

The ideas shared here come from real-life experience and practical habits that actually work.

→ Read more about Jeffi

- Annual Expenses Checklist With a Fillable Yearly Planner - July 1, 2026

- Monthly Bills Checklist for Beginners: Track Every Payment Clearly - June 29, 2026

- How Much Should You Save Each Week? Calculate Your Ideal Target - June 28, 2026