You promise yourself this will be the week you spend less.

Then a stressful day happens. A sale email appears. Amazon, Target, or your favorite clothing store suddenly has a “limited-time deal.” You scroll online at night when you are already tired, and one small purchase feels harmless.

Then another one follows.

Later, you check your account and think, “Why did I do that again?”

If this sounds familiar, you are not alone. Learning how to stop overspending habits is not about shaming yourself or becoming someone who never spends money. Overspending often happens automatically. It is usually a repeated pattern, not proof that you are careless with money.

The goal is to understand the pattern before it turns into another purchase.

You can stop overspending by noticing your triggers, adding friction before buying, pausing non-essential purchases, replacing the emotional reward, and reviewing slip-ups without shame.

How Do You Stop Overspending Habits?

You stop overspending habits by identifying your spending triggers, pausing before purchases, removing easy payment options, creating a spending boundary, replacing shopping with another reward, and reviewing slip-ups without shame.

The goal is not to rely on perfect willpower. The goal is to interrupt the habit before spending becomes automatic.

For many people in the US or Europe, overspending does not always come from huge luxury purchases. It often comes from small everyday leaks: food delivery, coffee runs, Amazon orders, discount clothing, convenience store snacks, subscriptions, or weekend spending that was never really planned.

That is why small behavior changes can make a real difference.

What Counts as an Overspending Habit?

An overspending habit is not one random mistake.

It is a repeated pattern where spending keeps happening in a similar way, even when you already planned to do something different.

It may look like:

- buying when you feel stressed, bored, lonely, or tired

- spending more than planned again and again

- using shopping as a quick mood boost

- regretting purchases but repeating the same behavior

- telling yourself “just this once” several times a week

- buying things because they are on sale, not because you need them

One expensive week does not mean you have a permanent problem. Life happens. Emergencies happen. Busy seasons happen.

But if the same spending pattern keeps repeating, it is worth understanding what triggers it.

Overspending Is a Pattern, Not a Personality Flaw

Overspending often feels like a discipline problem.

But most of the time, it works more like a habit loop:

Trigger → Urge → Purchase → Relief → Regret → Repeat

The trigger might be stress, boredom, comparison, payday, weekend plans, or late-night scrolling. The urge says, “Buying this will make me feel better.” The purchase gives quick relief.

Then regret arrives later, especially if the item was unnecessary or the money was needed elsewhere.

That regret can create more stress. And stress can trigger more spending.

This is why overspending can feel so frustrating. You are not only fighting a purchase. You are fighting a loop.

The goal is not to become perfect. The goal is to interrupt the loop earlier.

The Stop-Overspending Loop

Use this simple system when you notice yourself repeating the same spending pattern:

This gives you a practical way to stop overspending without depending only on motivation.

Motivation changes. Your environment can be adjusted.

The first step is learning how to control your spending habits before they turn into automatic decisions.

Step 1: Find Your Overspending Triggers

You cannot fix a spending pattern you cannot see.

Start by identifying what usually happens before you overspend. This is where many people skip too quickly. They try to cut spending without understanding why the spending keeps happening.

Common emotional triggers include:

- stress

- boredom

- loneliness

- tiredness

- frustration

- feeling like you deserve a reward

Common environmental triggers include:

- sale emails

- shopping apps

- ads

- saved payment details

- online stores

- food delivery apps

- walking into stores without a list

Common timing triggers include:

- payday

- weekends

- late-night scrolling

- lunch breaks

- after a hard workday

- right after receiving stressful news

Common social triggers include:

- comparison

- trends

- friends spending freely

- wanting to keep up

- feeling behind in life

- seeing other people’s purchases online

If you are trying to learn how to stop shopping when bored, the first step is not banning shopping forever. It is noticing boredom before it turns into browsing.

If you want to know how to stop spending when stressed, look for the moment stress becomes an urge to buy something for quick relief.

For one week, write down four things after an unplanned purchase:

- What did I buy?

- What was I feeling?

- Where was I?

- Was I tired, bored, stressed, or comparing?

This exercise is not about judging yourself. It is about finding the moment where the habit begins.

Breaking the emotional spending cycle can make it easier to control purchases that offer temporary relief but create regret later.

Step 2: Add Friction Before You Buy

Overspending gets easier when buying is too easy.

One-click checkout, saved cards, shopping apps, and constant sale emails remove the pause between wanting something and buying it. Adding friction puts the pause back.

Try this:

- remove saved cards from shopping websites

- log out of shopping apps

- turn off one-click buying

- unsubscribe from sale emails

- turn off shopping notifications

- move shopping apps off your home screen

- use cash or debit for flexible spending

- avoid browsing stores when you are bored

- keep a buy-later list instead of buying immediately

Friction works because it gives your thinking brain time to return.

If you have to stand up, find your card, log in again, or wait until tomorrow, the purchase becomes less automatic. That small delay can save real money.

For example, cutting just three $18 impulse purchases per week can keep about $54 in your account. Over a month, that is roughly $216. Over a year, it becomes more than $2,500.

That does not mean every small purchase is bad. It simply shows how repeated automatic spending can quietly become a serious money leak.

You are not banning yourself from buying. You are making sure the purchase has to pass through a pause first.

You do not have to remove everything you enjoy; the goal is to spend less without feeling restricted.

The First Place to Add Friction

Do not try to fix every spending trigger at once.

Start with the place where you overspend most. That might be:

- shopping apps

- food delivery apps

- saved cards

- sale emails

- weekend plans

- late-night browsing

- one-click checkout

- subscription trials

Pick one.

If online shopping is the biggest problem, remove saved cards first. If food delivery is the problem, log out of the app or delete it from your home screen. If sale emails trigger purchases, unsubscribe from the stores that tempt you most.

One small friction point is easier to maintain than a strict rule you quit after three days.

One practical way to stop overspending is to control daily expenses effectively in your everyday routine.

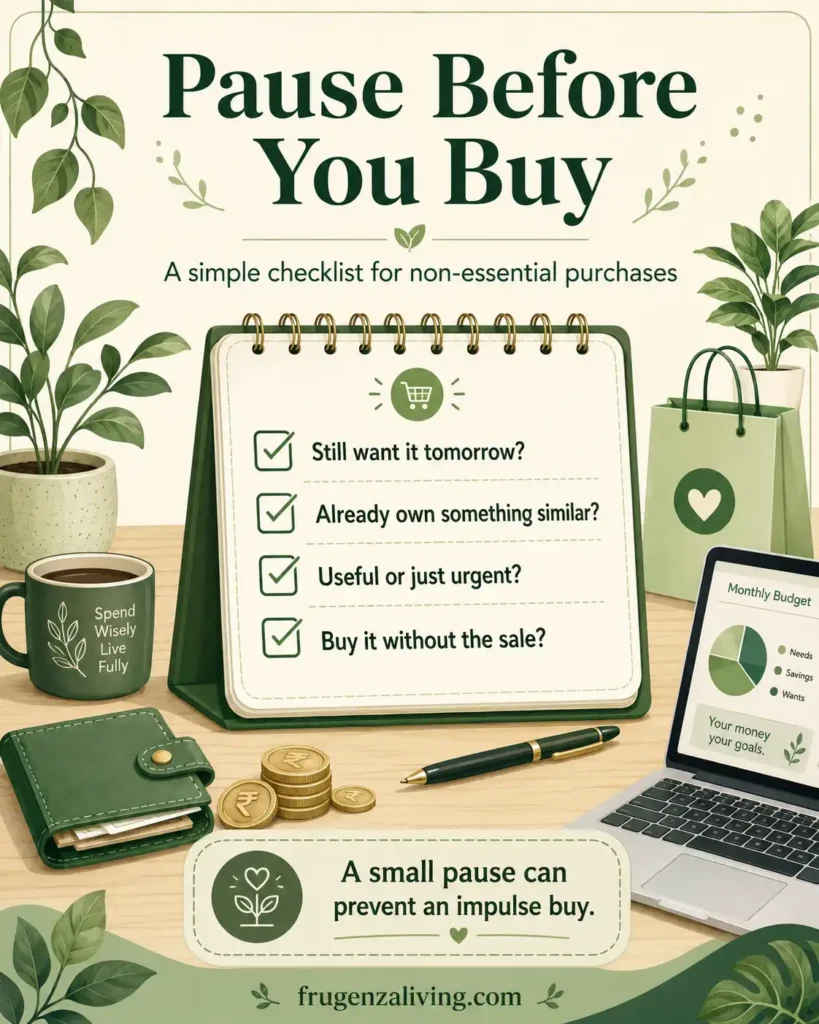

Step 3: Use a 24–48 Hour Pause Rule

The pause rule is simple:

When you want to buy something non-essential, wait 24–48 hours before purchasing it.

This is not the same as saying no forever. It is saying, “Not right now.”

Put the item on a buy-later list. Then ask:

- Do I still want this tomorrow?

- Do I already own something similar?

- Is this useful, or does it only feel urgent?

- Would I buy it without the sale?

- Will I still care about this next week?

- Is this purchase solving a real problem or just changing my mood?

Many wants fade once the emotion fades.

That is why the 24-hour rule for spending can be so helpful. It turns impulse buying into intentional buying.

For bigger purchases, use 48 hours or even a full week. The more expensive the purchase, the longer the pause should be.

You may still buy the item later. But if you buy it after a pause, the decision is usually calmer and more honest.

One of the easiest ways to stop overspending is to stop buying things you do not need before it becomes part of your routine.

Step 4: Replace the Reward, Not Just the Purchase

Overspending often gives a reward.

Not always a financial reward, but an emotional one. It might give comfort, excitement, relief, distraction, or a small feeling of control.

If you remove the purchase but ignore the emotion, the habit often comes back.

That is why replacement matters.

Instead of shopping when stressed, try:

- taking a short walk

- making tea or coffee at home

- listening to music

- taking a shower

- calling a friend

- journaling for five minutes

- cleaning one small space

- stretching

- reading a few pages

- stepping away from your phone

This is not about denying enjoyment. It is about giving yourself another way to feel better that does not create regret later.

The replacement does not need to be perfect. It only needs to interrupt the automatic path from emotion to purchase.

For example, if you usually shop at night because you feel drained, your replacement might be simple: charge your phone across the room, make tea, and watch one episode of something without browsing stores.

Small and realistic beats dramatic and impossible.

Step 5: Give Yourself a Planned Spending Boundary

Trying to spend nothing on fun can backfire.

When the plan feels too restrictive, it can create rebound spending. You stay strict for a few days, then suddenly spend more because you feel deprived.

A planned spending boundary gives you structure without making your life feel locked down.

For example, you might set:

- a weekly fun-money amount

- a monthly personal spending amount

- a cash envelope for flexible spending

- a separate debit card for non-essential purchases

- one planned treat per week

- a fixed limit for takeout or coffee

The point is not to spend freely. The point is to spend intentionally.

When you know there is a small amount you can use without guilt, you may feel less urge to rebel against your own plan.

This is especially helpful if strict saving plans usually make you overspend later.

If over-restriction causes rebound spending, how to save money without cutting everything can help you build a more balanced money-saving plan.

One common trigger is online shopping, so it helps to learn how to avoid impulse buying online before it becomes automatic.

A Simple Anti-Overspending Example

Here is what this can look like for someone who overspends on online shopping at night:

This is practical because it changes the environment around the habit.

You are not just telling yourself to “be better.” You are making overspending harder to repeat.

What to Do After You Overspend

You will not handle every purchase perfectly.

That is normal.

The important thing is what you do after overspending. Do not spiral. Do not punish yourself with extreme restriction. Do not say, “I already ruined it, so I might as well keep spending.”

Use this recovery loop instead:

Notice → Repair → Adjust → Continue

Notice what happened. Repair what you can. Return the item, cancel the order, or move money around if needed.

Then adjust one boundary. Maybe you need to unsubscribe, remove a saved card, avoid late-night browsing, or stop keeping a delivery app on your home screen.

Overspending once does not erase your progress. It gives you information about where the loop needs to be interrupted earlier.

What I Noticed After Treating Overspending Like a Habit Loop

When I treated overspending like a character flaw, shame made the cycle worse.

I would feel bad, try to be extremely strict, then eventually overspend again because the plan felt too heavy.

Things changed when I started looking for patterns.

I noticed when I was tired. I noticed when I was browsing without needing anything. I noticed how easy payment options made small purchases feel harmless.

Adding friction worked better than relying on willpower. Planned spending also helped because I no longer felt like every purchase was a failure.

Over time, learning to interrupt overspending habits became one of the foundations that helped me save over $15,000 in a year.

The biggest shift was not that I stopped wanting things. It was that I stopped buying at the peak of the urge.

It was not about becoming perfect. It was about catching the pattern earlier.

Common Mistakes When Trying to Stop Overspending

Relying Only on Willpower

Willpower is harder to use when you are tired, stressed, or emotionally drained. Change your environment too.

Deleting All Fun Spending

Strict plans can create rebound spending. Keep a small planned spending boundary so the plan feels realistic.

Ignoring Emotional Triggers

If stress or boredom causes spending, the trigger needs attention. The purchase is often only the surface behavior.

Keeping Saved Cards and Shopping Apps

If buying stays instant, overspending stays easy. Add friction before the purchase.

Not Reviewing What Happened

A quick review helps you learn the pattern. Without review, the same trigger may repeat next week.

Giving Up After One Slip

One overspending moment does not mean you failed. Adjust the system and continue.

How to Start Today

Do not start by changing your entire budget.

Start with your most repeated overspending moment.

Maybe it is ordering food after work. Maybe it is scrolling shopping apps at night. Maybe it is buying things on payday because the money finally feels available.

Pick one pattern and interrupt that one first.

Use this simple loop:

Notice → Pause → Add Friction → Replace

Notice one trigger. Pause one purchase. Remove one easy-buy option. Replace one shopping urge with something else.

That is enough for today.

You do not need to fix every spending habit at once.

If automatic spending happens throughout your day, frugal daily routine ideas can help you create small routines that reduce money leaks before they happen.

How This Fits Into Your Money-Saving System

This article focuses on breaking the overspending habit loop. It is not meant to replace your entire budget or savings plan.

If strict saving usually makes you rebel later, you may need a softer approach to saving money without cutting everything from your life.

If your biggest issue is that money disappears before you notice it, building a simple weekly saving routine can help you protect part of your income before impulse spending takes over.

For more repeatable changes, focus on frugal habits that actually save money instead of random tips that only work for a few days.

And if the emotional side of saving feels heavy, learning how to live frugally without feeling deprived can make the process easier to maintain.

Overspending control is one part of the system. Saving, frugal habits, and realistic routines help support it.

FAQ

How do I stop overspending habits?

You can stop overspending habits by identifying triggers, adding friction before purchases, using a 24–48 hour pause rule, replacing shopping with another reward, and reviewing slip-ups without shame. Focus on interrupting the habit loop before spending becomes automatic.

Why do I keep overspending even when I want to save?

You may keep overspending because spending has become linked to triggers like stress, boredom, tiredness, or comparison. Easy payment options and shopping apps can also make the habit automatic. The goal is to slow the process before the purchase happens.

How do I stop impulse buying online?

To stop impulse buying online, remove saved cards, unsubscribe from sale emails, log out of shopping apps, turn off one-click buying, and use a 24–48 hour waiting rule. These steps add friction and reduce automatic purchases.

What is the 24-hour rule for overspending?

The 24-hour rule means waiting at least one day before buying a non-essential item. Add the item to a buy-later list and decide later. Many impulse purchases feel less urgent after the emotion or excitement fades.

How do I stop spending money when stressed?

To stop spending money when stressed, notice the trigger before opening shopping apps or delivery apps. Replace the spending urge with a non-spending reset, such as walking, journaling, making tea, calling someone, or stepping away from your phone for a few minutes.

What should I do after overspending?

After overspending, avoid shame and use a recovery loop: notice what happened, repair what you can, adjust one boundary, and continue. Return or cancel the purchase if possible, then identify the trigger so you can interrupt it earlier next time.

Final Thought: You Do Not Need Perfect Discipline

Overspending is not fixed by hating yourself into better discipline.

It is fixed by catching the pattern earlier.

Start with one trigger. Add one pause. Remove one easy-buy option. Replace one shopping urge with something that still gives you relief without creating regret later.

Some weeks will be messy. That does not mean the system failed.

You do not need to become someone who never wants things.

You only need a better pause between the urge and the purchase.

The ideas shared here come from real-life experience and practical habits that actually work.

→ Read more about Jeffi

- Annual Expenses Checklist With a Fillable Yearly Planner - July 1, 2026

- Monthly Bills Checklist for Beginners: Track Every Payment Clearly - June 29, 2026

- How Much Should You Save Each Week? Calculate Your Ideal Target - June 28, 2026