Saving money helps, but it can still feel confusing when a bill or surprise expense appears. Should the money come from a sinking fund or an emergency fund? Is a car repair a true emergency, or should it have been planned for?

Understanding sinking fund vs emergency fund matters because using emergency savings for predictable expenses can leave you exposed when a real financial emergency happens.

A simple way to think about it is this: a sinking fund protects your emergency fund from predictable expenses.

Editor’s note: This article is for general budgeting education only. It is not personalized financial, debt, tax, or investment advice. Use the examples as a starting point and adjust based on your income, bills, household needs, and financial priorities.

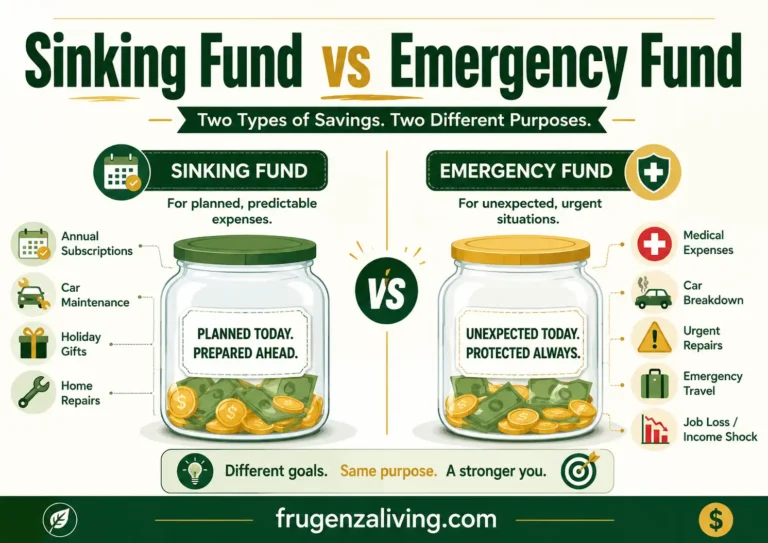

A sinking fund is for planned or predictable expenses, while an emergency fund is for unexpected financial shocks. Use a sinking fund for annual bills, holidays, routine car maintenance, and planned repairs. Use an emergency fund for urgent surprises like job loss, emergency travel, major medical costs, or a sudden essential repair.

What Is a Sinking Fund?

A sinking fund is money you set aside gradually for a known or expected expense. It usually has a specific name, target amount, and rough deadline.

Examples include annual insurance premiums, car registration, holiday gifts, planned home repairs, appliance replacement, pet checkups, and routine car maintenance.

A sinking fund is not only for fun goals. It is also useful for predictable expenses that often feel like emergencies simply because they were not planned.

What Is an Emergency Fund?

An emergency fund is a cash reserve for unplanned expenses or financial emergencies.

The Consumer Financial Protection Bureau describes emergency savings as money set aside for unplanned expenses or financial emergencies.

Emergency fund examples include job loss, sudden medical costs, urgent car repair, emergency home repair, emergency travel, or temporary income loss.

Your emergency fund should be accessible, but not mixed with everyday spending. It also should not be locked somewhere that makes urgent access difficult.

The easiest way to avoid confusion is to learn the sinking fund basics before deciding which expenses belong in each fund.

Sinking Fund vs Emergency Fund: The Core Difference

The core difference is simple:

A sinking fund is for costs you can see coming.

An emergency fund is for costs you did not expect.

Another way to say it:

Emergency fund = financial shock absorber.

Sinking fund = budget pressure release valve.

Sinking Fund vs Emergency Fund

For planned, expected, or predictable expenses.

Examples: holidays, annual bills, routine car maintenance, school costs, and planned repairs.

For unexpected financial shocks or urgent needs.

Examples: job loss, urgent medical costs, sudden essential repairs, and emergency travel.

A few common sinking fund categories can help you separate planned costs from true emergencies.

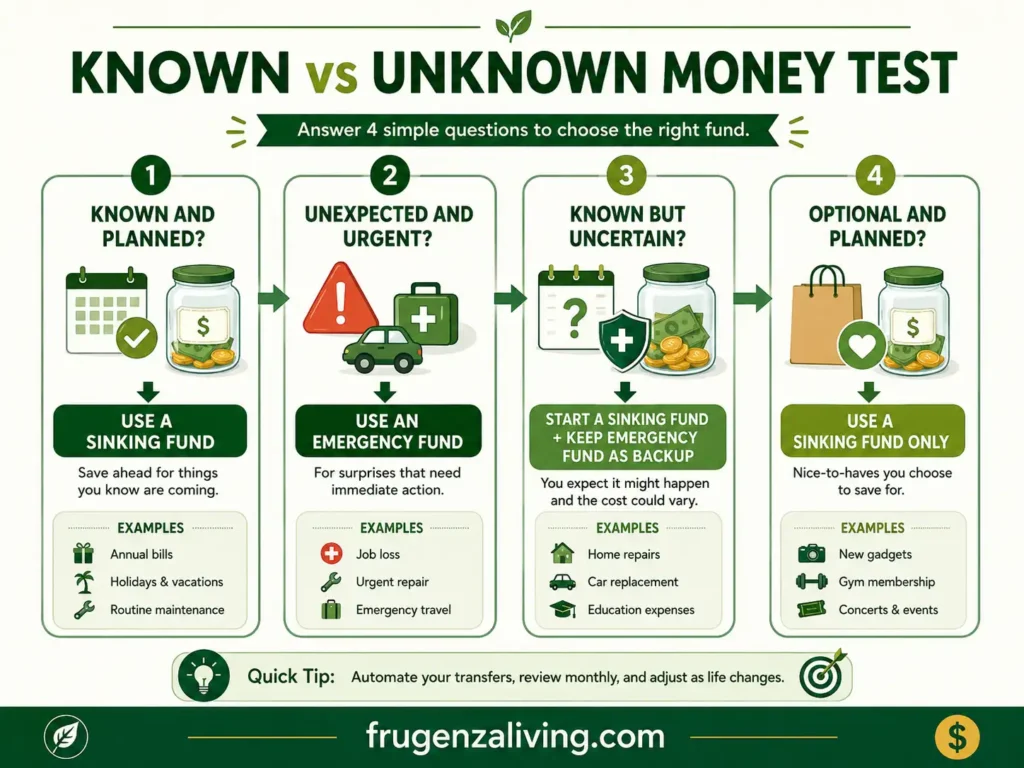

The Known vs Unknown Money Test

Many expenses feel urgent because they were not planned. But not every stressful expense is a true emergency.

Use the Known vs Unknown Money Test before deciding which fund to use:

- Did I know this expense was coming?

- Is it tied to a date, season, or deadline?

- Is it optional or required?

- Is it urgent and necessary?

- Would using emergency savings leave me exposed?

If the expense is known and has a deadline, use a sinking fund. If it is sudden, necessary, and disruptive, your emergency fund may be appropriate. If the expense is known but the amount is uncertain, start a sinking fund and keep emergency savings as backup.

If you only remember one rule, use this: planned and optional expenses belong in a sinking fund; sudden and necessary expenses may belong in your emergency fund.

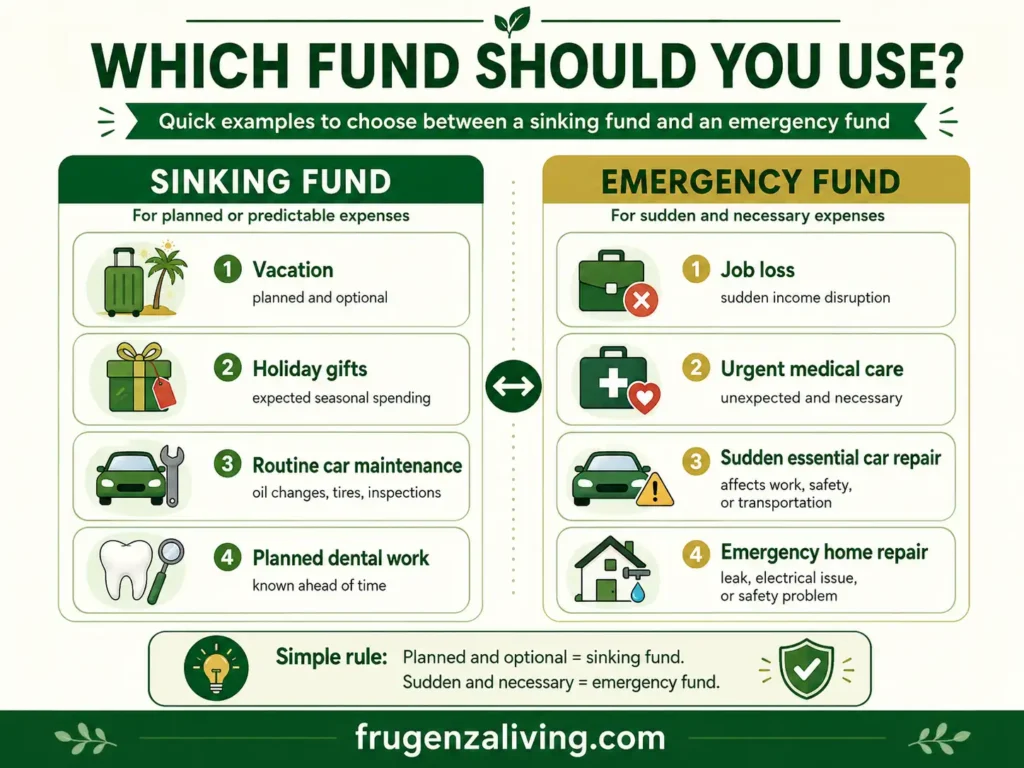

Which Fund Should You Use?

Gray-Area Examples That Confuse People

Some expenses are not perfectly planned or perfectly unexpected. The key question is whether the bill was expected, urgent, and necessary—not simply whether it feels stressful.

Car repair: Routine maintenance, tires, and inspections should be sinking fund expenses. A sudden repair that affects work, safety, or essential transportation may require emergency savings.

Medical bill: A planned appointment or dental procedure can be a sinking fund. Sudden urgent care may be an emergency fund expense.

Home repair: Planned maintenance belongs in a sinking fund. A sudden leak, electrical issue, or safety problem may need the emergency fund.

Pet care: Routine checkups can be sinking funds. A sudden emergency vet visit may need emergency savings.

A smart extra paycheck plan can give your emergency fund or sinking funds a helpful boost without disrupting your normal budget.

Which Should You Build First?

If you have no emergency savings at all, start with a small emergency starter fund first.

Use the First $500 Rule as a flexible starter target, not a universal rule. If $500 is too much right now, start smaller. The point is to create basic protection before adding too many sinking fund categories.

Then, start one or two tiny sinking funds for expenses you know are coming soon.

For example, if you have $100 to save this month and car insurance is due soon, you might split it between a starter emergency buffer and the car insurance sinking fund.

A simple beginner order is: starter emergency buffer, urgent sinking fund, bill cushion, then a larger emergency fund over time.

Understanding the difference between sinking funds and emergency savings can help you organize sinking funds clearly without creating too many accounts.

How Much Should Go Into Each Fund?

For an emergency fund, start with a small starter amount, then build toward a larger cushion based on essential expenses, income stability, household size, and job situation.

For a sinking fund, use this formula:

Total cost ÷ months or paychecks before the deadline = amount to save

If car insurance is $600 and due in 6 months, save $100 per month or about $25 per week. This turns a large future expense into small planned deposits.

Your monthly savings target may need to cover both emergency savings and sinking funds rather than going into one general account.

Where Should You Keep Sinking Funds and Emergency Funds?

Keep your emergency fund accessible, but separate from daily spending. A regular savings account, high-yield savings account, or separate bank account may work, depending on what is available to you.

Sinking funds can be kept in savings buckets, subaccounts, labeled accounts, spreadsheet categories, or digital envelopes. Avoid keeping all savings in one checking account with no labels.

Common Mistakes to Avoid

Using emergency savings for predictable annual bills. If you know the bill comes every year, build a sinking fund.

Having too many sinking funds at once. Start with the most urgent categories.

Saving for vacations while having no emergency buffer. Fun goals are valid, but basic protection should come first.

Forgetting to refill emergency savings. If you use the emergency fund, rebuild it. Pause optional sinking funds until your starter buffer is back in place.

If an emergency involves debt collections, eviction risk, medical billing, or legal consequences, consider contacting the provider, lender, landlord, or a qualified nonprofit counselor before making a decision.

Final Thoughts

A sinking fund and emergency fund are not the same thing, but they work best together.

A sinking fund prepares for costs you can see coming. An emergency fund protects you from financial shocks you did not expect.

If you are unsure which one to use, ask whether the expense was known, urgent, necessary, and predictable. That simple question makes the sinking fund vs emergency fund decision much easier.

FAQ

What is the difference between a sinking fund and emergency fund?

A sinking fund is for planned or predictable expenses, while an emergency fund is for unexpected financial shocks.

Do I need both a sinking fund and emergency fund?

Yes. A sinking fund helps with predictable expenses, while an emergency fund protects you from unexpected problems.

Should I build a sinking fund or emergency fund first?

If you have no emergency savings, start with a small emergency buffer first. Then begin one or two small sinking funds for expenses coming soon.

Is car repair a sinking fund or emergency fund?

Routine car maintenance should be a sinking fund. A sudden essential repair may be an emergency fund expense.

Is a medical bill a sinking fund or emergency fund?

It depends. Planned care can be a sinking fund. Sudden urgent care or an unexpected medical bill may require emergency savings.

Can I keep my sinking fund and emergency fund in the same account?

You can, but it is safer to separate them with labels, savings buckets, subaccounts, or a clear tracking system.

The ideas shared here come from real-life experience and practical habits that actually work.

→ Read more about Jeffi

- How to Split Bills Between Paychecks Without Overloading One Check - August 9, 2026

- Subscription Audit Checklist: Find and Review Every Recurring Charge - August 9, 2026

- How to Budget for Subscriptions Without Surprise Renewals - August 7, 2026