Saving 20% sounds precise until one person counts retirement deductions and an employer match, while another counts only cash transferred after payday.

So, how much should you save each month? Use a percentage as a benchmark, then balance what your goals require against what your cash flow can support. Savings already happening through payroll also matter.

How Much Should You Save Each Month?

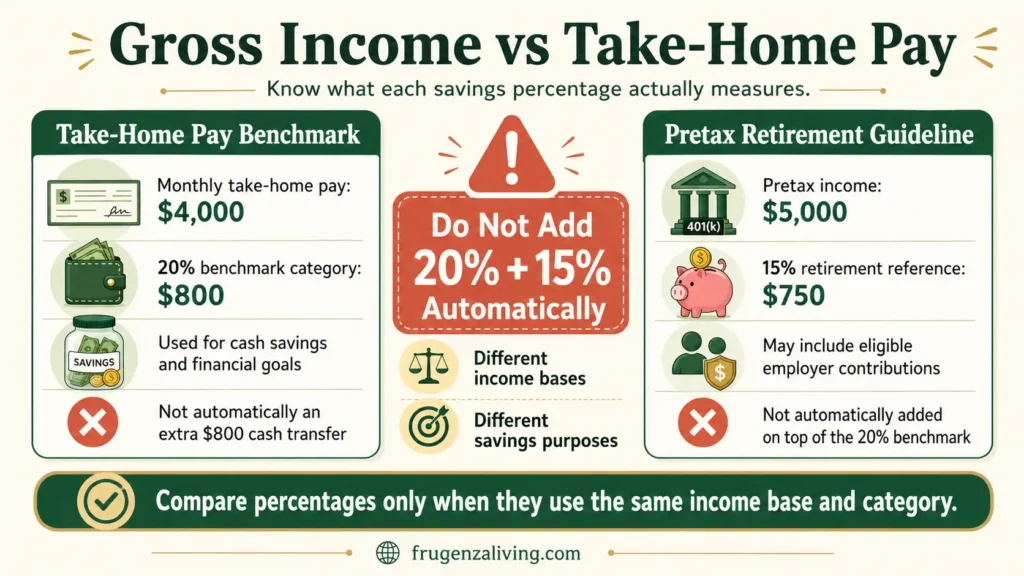

A common budget rule assigns 20% of take-home pay to savings and debt payments. For someone bringing home $4,000, that entire category would equal $800. It does not automatically mean transferring an additional $800 to cash savings, especially when extra debt payments or other qualifying amounts already use part of that category.

Use the percentage as a comparison point. Calculate what one goal requires, then compare it with the money available after realistic spending. Choose an amount that can remain saved.

Should You Save From Gross or Take-Home Pay?

A Consumer Financial Protection Bureau rule of thumb allocates 50% of take-home pay to needs, 20% to savings and debt payments, and no more than 30% to wants. It also allows room for a personal rule that better fits your situation.

For this article, focus on the savings portion. Minimum debt payments remain obligations, while extra principal payments can be tracked separately.

Retirement guidelines may use a different income base. Under its stated retirement-planning assumptions, Fidelity’s retirement savings guideline suggests working toward roughly 15% of pretax income, including eligible employer contributions. Your appropriate retirement rate may differ. This is not an additional 15% that should automatically be added to a take-home-pay benchmark.

Do not add percentages until you know both the income base and the category each percentage measures.

Cash savings may be measured against take-home pay. Retirement savings are often measured against pretax income. Those percentages do not combine cleanly unless they are recalculated using one consistent denominator.

Decide What Counts as Savings

Define the categories before calculating a total:

- Cash emergency savings: Accessible money for unexpected financial shocks.

- Goal-specific cash savings: Money reserved for a defined target or deadline.

- Employee retirement contributions: Long-term savings deducted from pay.

- Employer retirement contributions: Retirement savings tracked separately because they do not reduce take-home pay and may be subject to plan rules.

- Extra debt principal: Payments above the required minimum that may improve net worth but are not accessible cash savings.

Moving money between savings accounts does not create new savings. Minimum debt payments remain obligations.

Keep cash and retirement rates separate for monthly decisions. If you calculate a combined rate for personal tracking, use one clearly stated income base throughout and do not count the same contribution twice.

A realistic savings number should come after you allocate monthly income to necessities, not before.

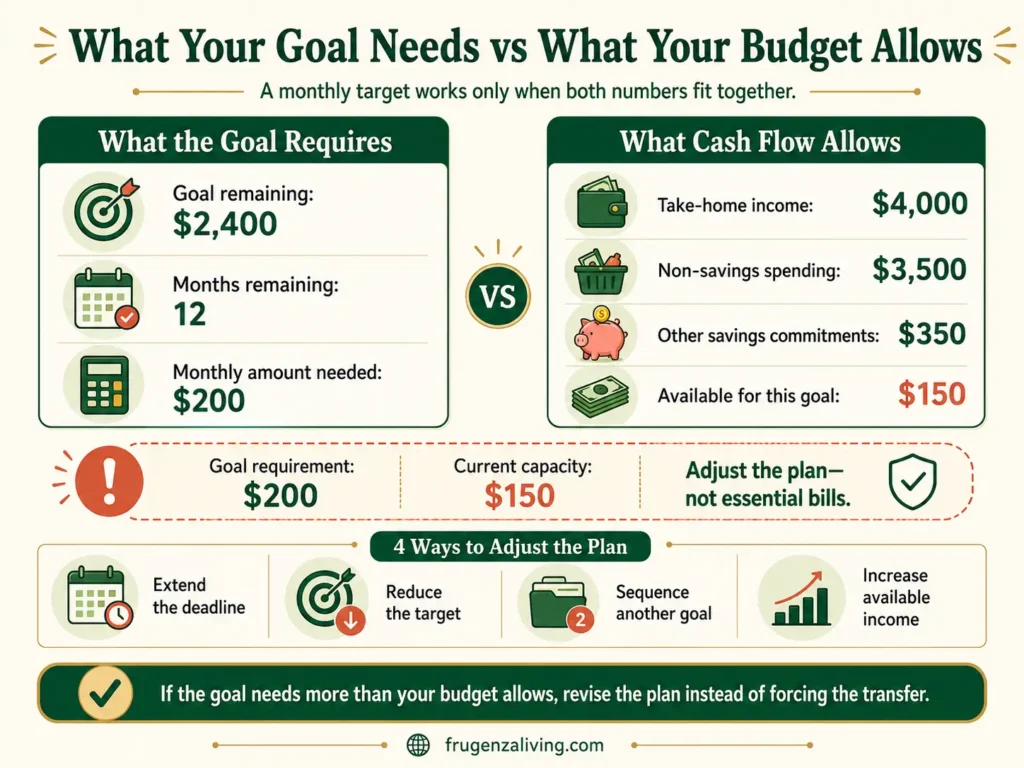

Calculate What One Goal Requires

For a goal with a target and deadline, use:

Monthly Amount Needed = (Goal Amount − Amount Already Saved) ÷ Months Remaining

Consider this illustrative example:

- Goal: $3,000

- Already saved: $600

- Time remaining: 12 months

- Monthly amount needed: $200

The calculation shows what the target and deadline require, not what your budget can support. If $200 does not fit, extend the timeline, reduce or sequence the goal, increase income, or revisit nonessential spending without neglecting required bills.

Use the worksheet below for a cash goal funded from take-home pay. Track payroll retirement contributions separately because they use a different income base.

Build a Monthly Savings Target That Fits

Enter your numbers directly and calculate each result using the formula shown. This fillable worksheet does not calculate automatically.

The worksheet does not submit or save your entries. Values may disappear if you refresh or leave the page, so copy your final numbers into your notes.

Benchmark

Take-Home Pay × (Reference Percentage ÷ 100) = Benchmark Category Amount

Enter 20 for 20%. This is a comparison point, not automatically a new cash transfer.

What This Goal Requires

Amount Still Needed ÷ Months Remaining = Monthly Amount Needed

What Cash Flow Allows for This Goal

Take-Home Income − Non-Savings Spending − Other Post-Paycheck Savings Commitments = Amount Available for This Goal

Include only transfers paid from take-home pay for other goals. Exclude payroll retirement deductions, employer contributions, and the contribution for the goal calculated above.

Choose the Starting Contribution

A new contribution to this goal should not exceed the amount available for this goal unless you reduce another commitment.

If the amount your goal requires fits within that limit, use it. If it does not, revise the timeline, target, income plan, or competing priorities rather than forcing the transfer.

Choose an amount that can remain saved without creating a shortage elsewhere.

Compare the Goal With Your Cash-Flow Capacity

Use recent spending rather than the budget you wish you followed. The CFPB recommends reviewing checking and credit-card history from several months and including less frequent costs so the estimate reflects real behavior.

For relatively stable finances, a three-month average can smooth out an unusual month.

Keep non-savings spending separate from transfers already going to savings. In the worksheet, “other post-paycheck savings commitments” means transfers from take-home pay for goals other than the one currently being calculated. Do not enter payroll retirement deductions or employer contributions because those amounts are not being paid from the take-home income shown in the card.

A new contribution to the current goal should stay at or below the amount available for that goal unless another commitment changes.

You can also convert your monthly savings target into a realistic weekly savings amount that fits each payday.

What If Your Savings Capacity Is Below 20%?

Twenty percent is a benchmark, not a pass-or-fail score.

Saving 5% or 10% may be a realistic current starting point when housing, childcare, medical costs, minimum debt payments, or other obligations leave little room. A fixed dollar amount may also be easier to manage than a percentage.

The test is whether the transfer leaves required bills covered and advances a goal without creating another shortage. Increase it after income rises or another obligation ends.

For a broader method of dividing an entire paycheck among bills, spending, savings, debt, and buffer, see how to compare common paycheck percentages.

Do Retirement Contributions and Employer Matches Count?

Your own retirement contributions are long-term savings, including amounts deducted before the paycheck reaches checking. An employer contribution may count when measuring total retirement saving, subject to plan rules, but it is not cash available for current expenses or emergencies.

Keep the rates separate when making monthly decisions. Cash savings and retirement savings serve different purposes and may use different income bases. If you calculate a combined rate for personal tracking, use one clearly stated income base and do not count the same contribution twice.

Planned future expenses and financial shocks also require different cash strategies. A dedicated comparison can help separate planned expenses from genuine emergencies.

When Should the Amount Change?

Your savings amount is a working decision, not a permanent identity. Give it a review date and reconsider it when:

- income changes;

- a goal is completed;

- housing, insurance, or childcare costs change;

- emergency savings are used;

- a new employer benefit begins;

- a recurring debt or other obligation ends.

A review prevents an outdated transfer from continuing after its assumptions have changed.

A Brief Note for Irregular Income

When income varies, use a conservative baseline from a normal lower-income month instead of the best month. Set a manageable base contribution, then save a chosen share of income above that baseline. Reviewing several months can help identify the range, while a dedicated system can help you build a budget around variable income.

Choose an Amount That Can Remain Saved

Compare three numbers: the benchmark you are considering, the amount one active goal requires, and the amount your current cash flow allows for that goal.

Calculate the monthly requirement, review several months of real spending, and use available cash-flow room as the ceiling. If the required amount is too high, change the assumptions rather than creating a transfer that repeatedly returns to checking.

This article provides general educational information, not individualized financial, tax, investment, or debt advice. The right amount depends on your income, obligations, benefits, goals, and local rules.

The ideas shared here come from real-life experience and practical habits that actually work.

→ Read more about Jeffi

- Annual Expenses Checklist With a Fillable Yearly Planner - July 1, 2026

- Monthly Bills Checklist for Beginners: Track Every Payment Clearly - June 29, 2026

- How Much Should You Save Each Week? Calculate Your Ideal Target - June 28, 2026