Dividing a $300 monthly savings goal by four gives you $75 per week. But saving $75 for 52 weeks produces $3,900—not the $3,600 annual total implied by $300 per month. The problem is that an average month contains about 4.33 weeks, not four.

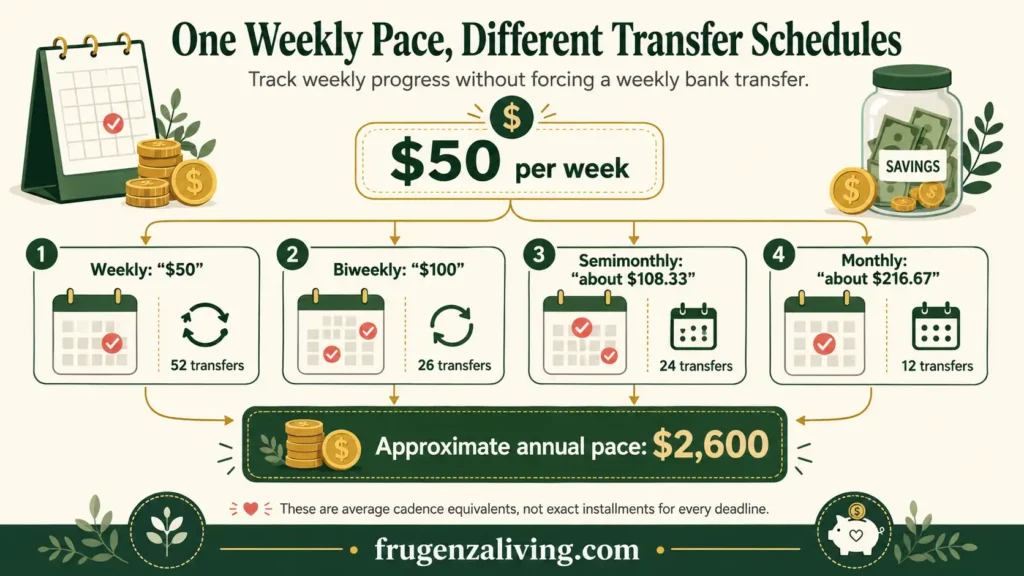

So, how much should you save each week? For a defined goal, subtract what you have already saved and divide the amount remaining by the actual weeks left. Then compare that pace with what your budget can support. A weekly target is a tracking pace; your bank transfer can still happen weekly, biweekly, semimonthly, or monthly.

How Much Should You Save Each Week?

The most useful answer is the amount required by one specific goal and deadline:

Weekly Amount Needed = (Goal Amount − Amount Already Saved) ÷ Weeks Remaining

This goal-and-weeks calculation follows the same basic approach used in the CFPB Savings Plan Tool.

If you are converting an existing monthly target, multiply it by 12 and divide by 52. If the resulting pace would interfere with essential bills or force you to move money back to checking, use a lower amount and adjust the deadline or target.

You do not need to transfer money every week. A $50 weekly pace can be funded as $100 every two weeks, about $108.33 twice per month, or about $216.67 monthly.

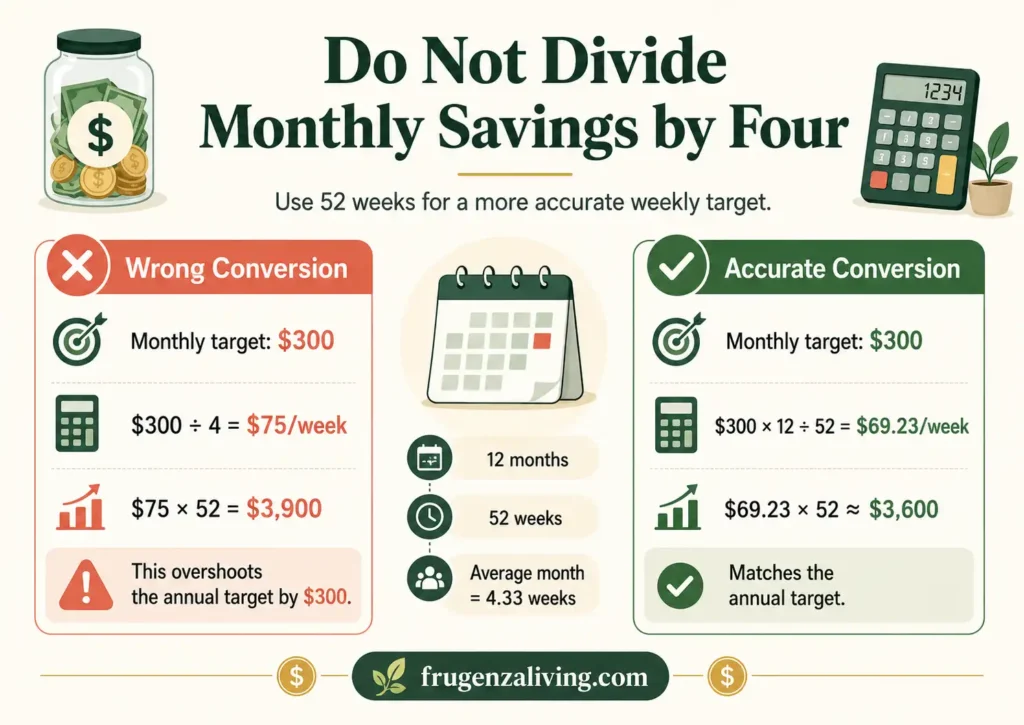

Do Not Divide a Monthly Savings Target by Four

For budgeting purposes, a year is usually treated as 52 weekly periods. Twelve four-week months would contain only 48 weeks, so dividing a monthly target by four creates a faster pace than the original plan requires.

Use:

Weekly Equivalent = Monthly Target × 12 ÷ 52

For an illustrative $300 monthly target:

- Accurate weekly equivalent: about $69.23

- Monthly target divided by four: $75

- $75 saved for 52 weeks: $3,900

- Intended annual target: $3,600

The difference is $300 over the year. Dividing by four can create an intentional cushion, but it is not an exact conversion.

Multiply your weekly amount by 52 and divide by 12 to estimate a more realistic monthly savings amount.

Calculate the Weekly Pace for One Goal

Suppose your goal is $2,000, you have already saved $500, and the deadline is 30 weeks away.

($2,000 − $500) ÷ 30 = $50 per week

Use the actual weeks remaining before the deadline. Do not automatically divide by 52 unless the goal is exactly one year away.

The result tells you what the deadline requires; it does not prove that $50 is affordable. If the amount is slightly uneven, keep the pace accurate and round the final contribution instead of inflating every weekly transfer.

Find Your Weekly Savings Pace

Enter numbers without currency symbols or commas. Results are displayed in U.S. dollars.

Results are estimates for a cash savings goal and exclude interest, investment growth, taxes, and account fees. Cadence equivalents preserve approximately the same annual pace; for a fixed deadline, divide the remaining amount by the actual transfers scheduled before that date. Calculations happen in your browser. Entries are not submitted or stored and may disappear after refresh.

A Weekly Target Does Not Require Weekly Transfers

A weekly target measures pace. Transfer frequency describes when money moves.

Using a $50 weekly pace:

- Weekly: $50

- Biweekly: $100

- Semimonthly: about $108.33

- Monthly: about $216.67

Using a savings percentage from each paycheck can make your target adjust naturally when your income changes.

These are average cadence equivalents that preserve roughly the same $2,600 annual pace. They are not guaranteed installments for a fixed deadline because the number of paydays or transfer dates before that deadline may differ.

Choose timing that matches your pay schedule and cash flow. The CFPB savings booklet recommends choosing a contribution frequency that fits your needs, such as weekly, monthly, or once per paycheck.

Check Whether the Weekly Pace Fits

The goal formula measures deadline pressure, not affordability. Compare the required pace with what normally remains after essential bills, realistic spending, and existing savings commitments.

A weekly target is not sustainable if it repeatedly has to return to checking before the next transfer.

If the required pace is too high, change the deadline, reduce or sequence the target, identify additional income, or lower another nonessential commitment.

When at least 13 weeks remain, use a quarterly checkpoint:

Checkpoint = The lower of Remaining Amount or Weekly Target × 13

If the deadline is sooner, the total remaining amount becomes the final checkpoint. At $50 per week, a full 13-week checkpoint is $650.

What If You Miss a Weekly Savings Target?

Do not automatically double the following transfer. That may turn one missed week into a new cash-flow problem.

Recalculate:

Revised Weekly Target = Remaining Amount ÷ Remaining Weeks

Then decide whether the revised amount still fits. If not, extend the deadline, reduce the target, or make a one-time contribution only when extra money is genuinely available.

The CFPB’s savings materials encourage you to continue after a missed week and reconsider the goal or timeline when the weekly amount repeatedly does not fit.

Is a 52-Week Savings Challenge the Same Thing?

No. A 52-week challenge is a behavioral exercise, often built around deposits that increase over time. It can make saving feel more engaging, but it does not calculate what a specific goal and deadline require.

If you need $1,500 in 30 weeks, divide the remaining goal by those 30 weeks. A challenge that starts with very small deposits may leave the largest contributions until the end, when they could be hardest to afford.

Use a challenge for motivation; use a goal-based weekly amount for deadline planning.

Should You Save a Percentage of Weekly Income?

A percentage can work when weekly take-home income is stable:

Weekly Take-Home Pay × Chosen Savings Percentage = Weekly Savings Amount

Choosing the percentage itself belongs to your broader plan. First decide your overall monthly savings target, then use this article to convert it into a weekly pace.

If You Are Paid Weekly or Your Income Changes

Tracking a weekly pace is not the same as building a complete weekly-pay budget. You can time the actual transfer for payday while using the weekly amount as a progress measure. For bills and paycheck allocation, build a full budget around weekly paychecks.

When income varies, use a conservative capacity based on a normal lower-income period rather than the best week.

Use the Weekly Number as a Pace, Not a Rule

Your weekly savings amount should connect a real goal, a real deadline, and a realistic budget. It does not require a weekly bank transfer, and it should be recalculated when the deadline or cash flow changes.

Choose one goal, subtract what is already saved, count the actual weeks remaining, and calculate the pace before scheduling a transfer.

This article provides general educational information, not individualized financial, investment, tax, or debt advice.

The ideas shared here come from real-life experience and practical habits that actually work.

→ Read more about Jeffi

- Annual Expenses Checklist With a Fillable Yearly Planner - July 1, 2026

- Monthly Bills Checklist for Beginners: Track Every Payment Clearly - June 29, 2026

- How Much Should You Save Each Week? Calculate Your Ideal Target - June 28, 2026