A beginner can write down every recurring bill and still lose track of committed money. A utility payment may be scheduled but not yet posted, a subscription may try to charge a replaced card, and an annual renewal may never appear on a list built from only this month’s statements.

A useful monthly bills checklist for beginners tracks more than “paid” or “unpaid.” It shows whether the amount is known, the funding source is ready, payment has been initiated, the transaction has posted, and the biller has updated the account. The fillable and printable board below follows that path without becoming a full budgeting system.

What Should a Monthly Bills Checklist Include?

Record the bill name, type, expected and actual amounts, verification date, payment action date, due date, payment source, autopay status, and responsible person when relevant.

Also track whether the funding source is ready, payment was initiated, the transaction posted, and the biller updated the account. Here, paid means confirmed complete—not merely submitted or scheduled. One dependable monthly bill payment checklist should show what is due, when to act, where payment comes from, and what still needs confirmation.

A Bill Checklist Is Not a Monthly Budget

A bill checklist tracks obligations and payment status. A bill calendar shows when to act and when payments are due. A monthly budget determines whether income can cover bills, spending, and goals.

A balanced budget does not prove that an individual payment processed. Use this page for payment control and a separate routine to review the rest of your monthly budget.

What Belongs on the Checklist?

Fixed monthly bills

These usually stay similar each cycle. Examples include rent or mortgage, loan minimum payments, internet, a phone plan, monthly insurance, and childcare fees.

Variable monthly bills

These recur but change in amount. Electricity, water, heating, usage-based phone charges, and the required or planned credit-card payment shown on the current statement may belong here. Enter an estimate early, then replace it when the statement arrives.

Groceries, gasoline, dining out, and clothing are usually spending categories rather than bills unless they involve a recurring invoice, subscription, or required payment.

Non-monthly recurring bills

Annual insurance premiums, vehicle registration, professional memberships, software renewals, and semiannual fees belong on the master inventory even when they are not due this month.

A yearly bills checklist can help you separate monthly obligations from expenses that arrive only once or twice a year.

Build the Master List From Real Records

Review several months of bank and card activity, then check the previous 12 months for annual renewals. Search email for “statement,” “invoice,” “renewal,” and “payment due.” Include paper mail, account portals, app-store subscriptions, digital wallets, and memberships attached to older cards.

One month will not reveal every obligation. Build a master inventory first, then copy the bills relevant to the current month into your working checklist.

A paycheck budget template for beginners can help you assign bills before the rest of your money is used for flexible spending.

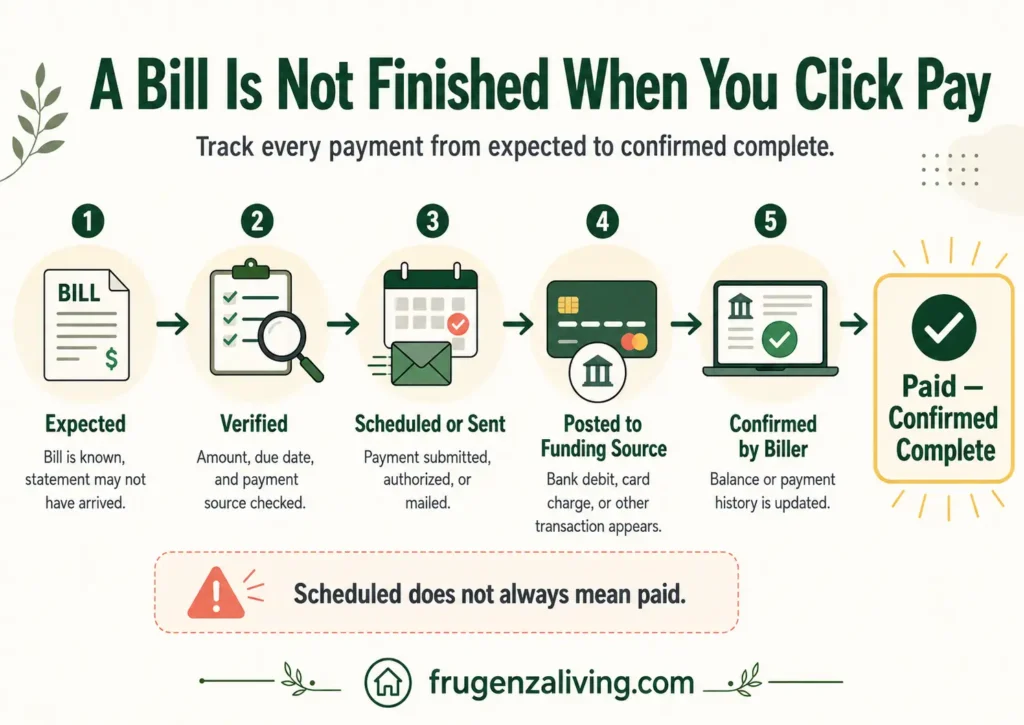

Do Not Use One “Paid” Box for Every Stage

A payment can move through five steps:

- Expected: The obligation exists, but the current statement or amount may not be available.

- Verified: The amount, due date, payment source, and method have been checked.

- Scheduled or sent: Payment has been initiated, authorized, or mailed.

- Posted to the funding source: The bank debit, card charge, or other transaction appears on the account used to pay.

- Confirmed by the biller: The biller credited the payment or updated the account balance or payment history.

Treat the bill as paid—confirmed complete only after the final two checks.

A confirmation page can make a bill look finished even while the transaction has not posted and the biller still shows it as pending. Separating “scheduled,” “posted,” and “confirmed” keeps that payment visible.

The fillable and printable monthly bill checklist below provides five detailed cards and five compact rows.

Monthly Bill Control Board

Use detailed cards for variable bills, autopay, shared responsibilities, or payments that need closer monitoring. Use compact rows for straightforward recurring bills.

This is a fillable manual worksheet. It does not calculate totals, save entries, submit information, or update the review fields automatically. Entries may disappear after a refresh or when you leave the page. Do not enter account numbers, card numbers, passwords, or other sensitive information.

To print the complete board, expand all five detailed cards, then use your browser’s Print command. Review the preview because browser layouts can differ.

Bill 1

Bill 2

Bill 3

Bill 4

Bill 5

Additional Bills 6–10

Use these compact rows for simple bills that do not need the full payment-path details above.

Manual Monthly Review

Complete this summary yourself after reviewing the detailed cards and compact rows.

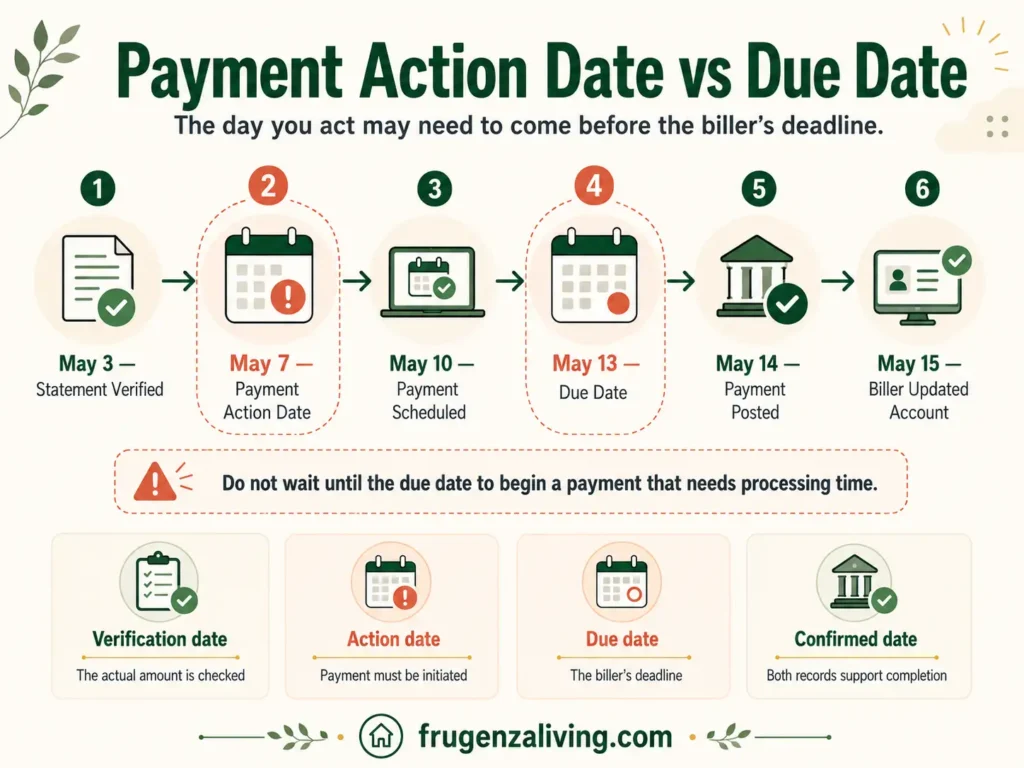

Use the Right Dates

Four dates can matter:

- Verification date: when the amount was checked.

- Payment action date: when you schedule, authorize, or send payment.

- Due date: the biller’s deadline.

- Confirmed date: when the funding-source record and biller account support completion.

Different payment methods use different processing times. The CFPB’s Bill Calendar Tool plans an action date before the due date. Check each biller’s instructions instead of assuming every method is immediate.

How to Use the Checklist During the Month

At the start of the month

Copy current obligations from the master inventory. Use detailed cards for variable bills, autopay, or shared responsibilities and compact rows for simpler bills. Add income dates and payment sources without entering account or card numbers.

Choose one weekly review day to add statements and check unfinished payments.

When a statement arrives

Replace the estimate with the actual amount. Record the verification date, check the payment source, and choose an action date that allows for processing.

After payment is initiated

Mark it scheduled or sent, but keep it open. Confirm that the transaction posted and the biller updated the account. Then record the confirmed date and a non-sensitive note.

Use Autopay Without Making It Invisible

Autopay reduces manual work but does not prove that a payment succeeded. For automatic debits from a bank account, the CFPB notes that an insufficient balance can lead to overdraft or nonsufficient-funds problems.

Card-funded autopay has different risks, including an expired card or declined transaction. Whatever the method, verify the amount, expected date, funding source, and final account update.

What If Bills and Paydays Do Not Line Up?

Add income dates to the bill calendar and find periods when bills exceed incoming cash. Contact the biller before the deadline and ask whether another due date is available; not every provider permits changes.

Confirm how a change affects the next statement. For allocation after income arrives, use a separate system to assign bills to the paycheck that will fund them.

Keep Non-Monthly Bills Visible

Annual and quarterly obligations should remain on the master inventory. If you are starting from $0 with 12 months to prepare for a $1,200 annual premium, setting aside $100 per month would reach that amount by the deadline.

That $100 is advance preparation, not part of this month’s paid-bill total unless the premium is actually due. If you are unsure what to include, review a simple budget categories list to identify fixed bills, variable expenses, debt payments, and subscriptions.

When There Is Not Enough Money for Every Bill

Contact providers early, ask about available arrangements, and check official assistance resources. Rules and consequences vary by bill type and location. Use the checklist to identify affected payments, but seek qualified local guidance for decisions involving serious housing, utility, legal, debt, or credit consequences.

Make “Paid—Confirmed Complete” the Final Check

A useful monthly bills checklist for beginners does not stop when you press a payment button. It shows whether the amount is verified, the funding source is ready, payment was initiated, the transaction posted, and the biller updated the account.

Review recent bank, card, email, and paper records. Add five complex bills to the detailed cards and up to five simpler bills to the compact rows. Give each one an action date and payment source, then keep it open until the final two checks are complete.

This article provides general educational information, not individualized financial, legal, debt, or credit advice. Payment processing times, contracts, grace periods, and consumer protections vary.

The ideas shared here come from real-life experience and practical habits that actually work.

→ Read more about Jeffi

- Annual Expenses Checklist With a Fillable Yearly Planner - July 1, 2026

- Monthly Bills Checklist for Beginners: Track Every Payment Clearly - June 29, 2026

- How Much Should You Save Each Week? Calculate Your Ideal Target - June 28, 2026