Budgeting feels much easier when the same paycheck arrives on the same schedule every month.

But if your income changes, budgeting can feel like trying to hit a moving target. One month looks comfortable. The next month feels tight. A big payment comes in, then nothing shows up for two weeks.

This can happen if you’re a freelancer, gig worker, contractor, commission-based employee, creator, seasonal worker, small business owner, or someone whose hours, tips, projects, or commissions change from month to month.

Learning how to budget irregular income is not about guessing your best month and hoping it works. It is about building your budget around a safer baseline, protecting your must-pay expenses, and using high-income months to support lower-income months.

This is general budgeting education, not professional financial advice. Tax rules vary by country, state, and personal situation, so consider speaking with a qualified tax professional if you need personal tax advice.

Quick Answer: How Do You Budget Irregular Income?

To budget irregular income, start with a conservative baseline income, list your minimum monthly expenses, prioritize bills and basic needs, separate tax money if needed, and build a cash flow buffer.

A variable income budget should use high-income months to prepare for low-income months instead of treating every extra dollar as free spending money.

Why Irregular Income Needs a Different Budget

A traditional budget often assumes your income is predictable.

That does not work well when your income changes every month.

With irregular income, your biggest challenge is not just how much you earn. It is when the money arrives. A high-income month can create a false sense of safety, while a low-income month can make normal bills feel stressful.

An irregular income budget should protect your lowest month, not celebrate your highest month.

That means your budget needs to answer a few practical questions:

- What is the safest income number to use?

- What must be paid every month?

- What happens when income is lower than expected?

- What should extra income do when a better month arrives?

Once those questions are clear, variable income starts to feel less random.

Irregular income becomes easier to handle when you start with a simple money management plan instead of guessing every month.

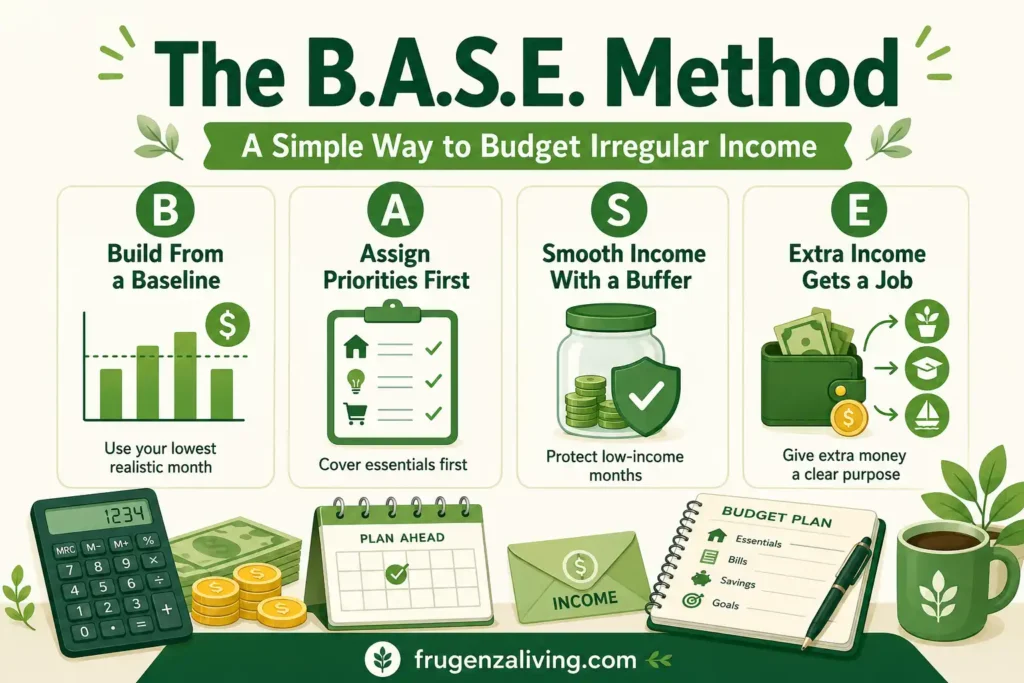

The Irregular Income Budget Rule

A simple way to budget with irregular income is to use the B.A.S.E. Method.

This method helps you avoid the feast-or-famine cycle where high-income months feel exciting, but low-income months feel stressful.

The goal is not to make your income perfectly predictable. The goal is to make your decisions more predictable.

Step 1: Find Your Baseline Income

The first step is choosing the income number your budget should use.

Do not start with your best month. Do not rely too heavily on your average month if your income swings a lot. Averages can hide cash flow gaps.

Instead, look at the last 6–12 months of income if you have that data. Then find your lowest normal month. This does not mean your worst emergency month. It means a conservative income number that could realistically happen again.

Example:

- Best month: $6,000

- Average month: $4,200

- Lowest normal month: $2,800

- Budget baseline: $2,800

In this case, the baseline income budget should start with $2,800.

When your income is unpredictable, it becomes even more important to split your income for budgeting before spending anything.

If you are new to freelancing, gig work, commission income, seasonal income, or fluctuating income, use the safest confirmed income number you have.

It is better to build a smaller budget and expand later than to build a large budget that collapses during a low-income month.

Step 2: Know Your Minimum Monthly Expenses

Next, find your minimum monthly expenses.

This is not your full lifestyle budget. It is your bare-bones budget: the amount you need to cover basic bills and essential needs during a low-income month.

Common minimum expenses include:

- Rent or mortgage

- Utilities

- Basic groceries

- Transportation

- Insurance

- Debt minimums

- Childcare

- Phone and internet

- Tax set-aside if self-employed

This number matters because it tells you how much income you need before spending becomes flexible.

If your baseline income is $2,800 and your minimum monthly expenses are also around $2,800, you do not have much room for extra spending during low months. That does not mean the budget is impossible. It means high-income months need to help create breathing room.

A monthly money review can help you update your budget based on what you actually earned.

Step 3: Build a Priority-Based Budget

When income is inconsistent, not every expense deserves the same protection.

Priority-based budgeting matters because essential expenses need to be covered before flexible spending.

A simple order can look like this:

- Tax set-aside if needed

- Housing

- Utilities

- Food

- Transportation

- Insurance

- Debt minimums

- Emergency buffer

- Flexible spending

- Wants or fun money

This does not mean fun money is bad. It just means it should not come before rent, taxes, food, or bills.

If taxes are already withheld from your paycheck, you can use that same priority line for your cash flow buffer, upcoming bills, or emergency savings instead.

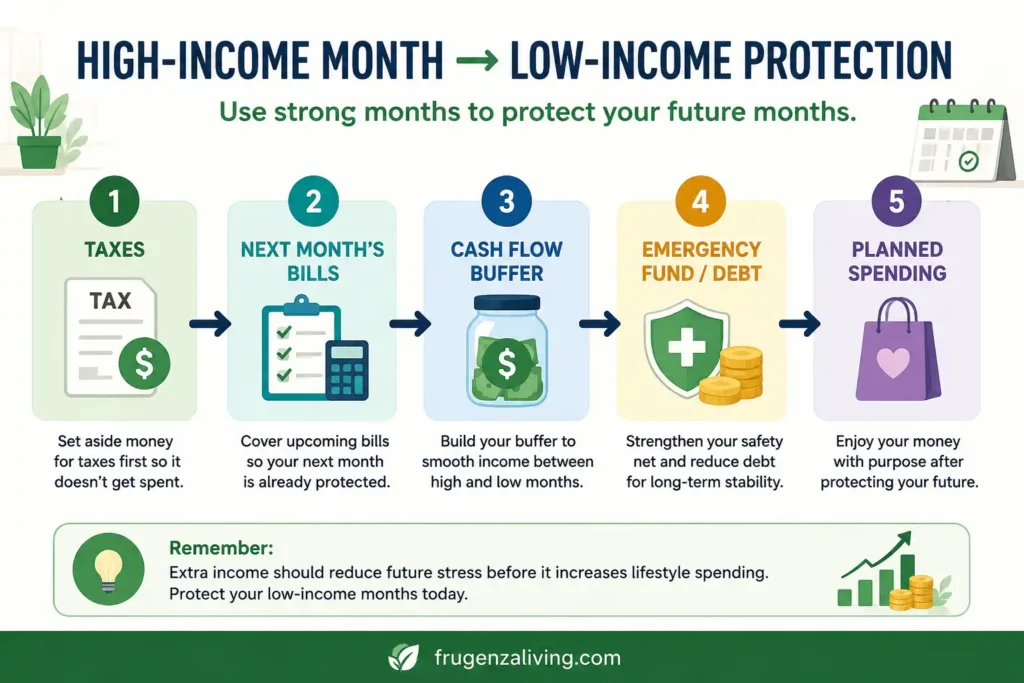

Step 4: Use High-Income Months to Protect Low-Income Months

High-income months are where irregular income budgeting becomes powerful.

When more money comes in, it is tempting to upgrade everything at once. But if next month could be much lower, extra income needs to protect your future cash flow first.

This is called income smoothing.

The idea is simple: use strong months to make weak months less stressful.

A good first goal is to build a cash flow buffer equal to one month of minimum expenses. If your income is extremely unpredictable, you may eventually want a larger irregular income savings buffer, such as two or three months of basic expenses.

This buffer has one job: to help you pay bills when income arrives late, drops suddenly, or comes in smaller than expected.

Step 5: Give Extra Income a Clear Order

Extra income should reduce future stress before it increases lifestyle spending.

That does not mean you can never enjoy a strong month. It means extra money needs an order.

This order helps you avoid spending a high-income month before it can protect a low-income month.

A simple payday budgeting routine can help you give every payment a clear purpose.

Step 6: Separate Tax Money Before You Spend

If taxes are not automatically withheld from your income, do not treat the full payment as spendable money.

This is especially important for freelancers, contractors, creators, small business owners, and self-employed workers. Tax set-aside for irregular income should happen early, not after the money has blended into daily spending.

A simple approach is to use a separate savings account for tax money. The exact amount depends on your income, location, business expenses, and tax situation, so it is smart to speak with a qualified tax professional if your situation is complex.

For U.S. readers, the IRS Self-Employed Individuals Tax Center can help you understand basic self-employment tax responsibilities.

Use an Income Holding Account if Your Income Swings a Lot

If your income changes sharply from month to month, an income holding account can make your budget calmer.

The idea is simple: income lands in one account first. Then you transfer a planned amount into your regular checking account for bills and spending.

For example, if your baseline budget is $2,800, you might pay yourself $2,800 from the holding account each month when possible. In high-income months, the extra money helps refill the holding account. In low-income months, the holding account helps cover the gap.

Think of it like paying yourself a steadier monthly “salary” from uneven income.

This does not work overnight. You may need to build the buffer slowly. But over time, it can make irregular income feel more like steady income.

What to Do in a Low-Income Month

A low-income month needs a different mode.

This is not the time to force your full lifestyle budget. Switch to your minimum monthly expenses and protect the most important bills first.

A simple low-income month budget might include:

- Pay essential bills first

- Pause non-essential spending

- Use the cash flow buffer only for planned essentials

- Delay wants if needed

- Avoid adding new debt when possible

- Review every time income arrives

The goal is not to panic. The goal is to protect the basics until income improves again.

Step 7: Review Your Budget Every Time Income Arrives

With irregular income, you cannot always wait until the end of the month to make decisions.

Each time money arrives, do a quick review:

- Do I need to set aside taxes?

- Are current bills covered?

- Are next month’s bills protected?

- Does the cash flow buffer need money?

- How much is actually safe for flexible spending?

Irregular Income Budget Example

Here is a simple example.

Baseline income: $2,800

Minimum monthly expenses:

- Housing: $1,100

- Utilities: $250

- Food: $450

- Transportation: $250

- Insurance: $180

- Debt minimums: $220

- Phone/internet: $120

- Tax set-aside: $230

Total minimum: $2,800

Now imagine a high-income month brings in $4,600.

Extra income: $1,800

A clear allocation could look like this:

- $400 to taxes

- $500 to next month’s bills

- $500 to cash flow buffer

- $250 to emergency fund or debt

- $150 to planned spending

This type of plan makes the high-income month useful instead of just exciting.

Common Mistakes When Budgeting Irregular Income

Watch for these common mistakes:

- Budgeting from your best month: This makes low-income months harder.

- Using average income too early: Average income can hide cash flow gaps.

- Forgetting taxes: Self-employed income may need tax money separated early.

- Treating extra income as free money: Extra income should protect future months first.

- Not knowing your minimum expenses: You need a bare-bones number before building a flexible budget.

- Mixing bill money and spending money: Separate labels or accounts can reduce confusion.

- Waiting until the end of the month: Irregular income needs a quick review whenever money arrives.

How This Is Different From a Monthly Budget Reset

Irregular income budgeting is a system for handling income that changes.

A monthly budget reset is different. It is a review process you use to adjust categories, bills, savings, and spending before a new month begins.

The two systems can work together. Your irregular income budget helps you decide what to do when income varies. Your monthly reset helps you adjust the plan based on what actually happened.

Final Thoughts: Make Irregular Income Feel Less Random

Budgeting irregular income is not about predicting every dollar perfectly.

It is about building a system that can handle uncertainty.

Start with a conservative baseline. Know your minimum expenses. Use a priority-based budget. Build a cash flow buffer. Separate taxes before spending. Give extra income a job before lifestyle spending grows.

You may not control when every dollar arrives, but you can decide what each dollar does when it gets there.

FAQ

How do you budget irregular income?

To budget irregular income, start with a conservative baseline income, list your minimum monthly expenses, prioritize bills and basic needs, separate taxes if needed, and use high-income months to build a cash flow buffer.

What income number should I use for an irregular income budget?

Use your lowest realistic monthly income, not your best month. If you have 6–12 months of income history, look for your lowest normal month and build your baseline budget from that number.

Should I use average income or lowest income to budget?

If your income changes a lot, the lowest realistic income is usually safer than the average. Average income can make your budget look fine on paper while still leaving you short during low-income months.

What should I do in a low-income month?

In a low-income month, switch to your minimum expenses, protect essential bills, pause non-essential spending, and use your cash flow buffer only for planned needs.

How much buffer do I need with irregular income?

A good first goal is one month of minimum expenses. If your income is very unpredictable, you may eventually want two or three months of minimum expenses as a cash flow buffer.

How do freelancers budget for taxes with irregular income?

Freelancers can budget for taxes by separating tax money as soon as income arrives. The right amount depends on your income, deductions, location, and tax situation, so a tax professional can help if your situation is complex.

The ideas shared here come from real-life experience and practical habits that actually work.

→ Read more about Jeffi

- How to Stop Buying Coffee Every Day Without Giving Up Coffee - July 25, 2026

- 8 Meals for One Without Leftovers—and How to Use the Rest - July 22, 2026

- 9 Cheap Dinners for One Person on a Budget That Feel Complete - July 20, 2026