Payday feels good until the money starts disappearing faster than expected.

One bill comes out. Then groceries. Then a subscription you forgot about. Then a few small purchases that did not feel like a big deal at the time. Before long, your paycheck feels smaller than it should.

Learning how to budget after payday is not about making life feel strict. It is about giving your money an order before spending begins.

A simple payday routine helps you decide what needs to happen first: bills, savings, debt, spending limits, buffer money, and leftover cash.

This is general budgeting education, not professional financial advice. If you are dealing with serious debt, missed payments, or legal financial issues, consider speaking with a qualified financial counselor.

Quick Answer: What Should You Do After Payday?

After payday, check your real take-home pay, list the bills due before your next payday, pay or set aside money for those bills, move savings or debt money early, then set a spending limit for groceries, gas, household items, and personal spending.

A good payday routine gives every dollar a job before you start spending from your paycheck.

Why Money Disappears Fast After Payday

Payday can create a false sense of comfort.

Your bank balance looks higher than usual, so it is easy to feel like you have more spending room than you actually do. But that balance may already include money needed for rent, utilities, subscriptions, debt payments, groceries, transportation, or automatic payments.

Most payday problems start when spending happens before planning.

The issue is not always your income. Sometimes, the real problem is the order. If flexible spending comes first, bills and savings have to survive on whatever is left. That is when budgeting starts to feel stressful.

A better after payday budget plan starts with this rule:

Do not treat your full bank balance as spending money.

Some of that money already has a job.

The First 30 Minutes After Payday

The first 30 minutes after payday can decide how stressful the next week or two feels.

You do not need to build a complicated system. You just need a short pause before spending.

Here is what to do first after getting paid:

- Open your bank account.

- Check the real deposit amount.

- Compare it with what you expected.

- List bills due before your next payday.

- Pause non-essential spending until the plan is done.

This is the payday freeze rule: for the first few minutes after payday, freeze non-essential spending. Do not order food, shop online, or make impulse purchases until bills, savings, and spending limits are set.

Think of this as your same-day payday budget routine. You still get to spend money, but only after you know what is actually safe to spend.

If your paycheck is higher than expected because of overtime, tips, or bonuses, do not immediately treat all of it as extra. Give the extra money a job first. It can go toward savings, debt, a bill coming soon, or a small planned treat.

A simple payday budget template can make it easier to organize your income right after it arrives.

What to Do With Your Paycheck After Payday

A strong payday budget starts with the right order.

You can think of your paycheck like a line of priorities. The money that protects your life and bills goes first. Flexible spending comes after that.

A simple payday money order looks like this:

- Bills due before next payday

- Rent or mortgage set-aside

- Debt minimums

- Savings or sinking funds

- Flexible spending

- Buffer

- Planned fun money

This does not mean you can never enjoy your money. It just means you stop spending from the wrong pile.

If you get paid every two weeks, learning how to budget biweekly paychecks can help your money last until the next payday.

Step 1: Check Your Real Take-Home Pay

The first step in any payday budget is to check the money that actually arrived.

Do not budget from your gross pay. Gross pay is the amount before taxes, insurance, retirement contributions, and other deductions. Your budget should start with take-home pay because that is the money you can actually use.

If your income changes from paycheck to paycheck, use the real deposit amount. If it is lower than expected, adjust before spending. If it is higher than expected, avoid treating the extra as free money too quickly.

A simple after payday budget plan starts with one number:

How much money actually landed in your account?

Once you know that, you can decide what the paycheck needs to do.

Step 2: Pay or Set Aside Bills First

Bills should come before flexible spending.

Start with bills that are due before your next payday. If the bill is due soon, pay it now. If it is not due yet but will be due before the next paycheck, set the money aside so it does not get mixed with spending money.

Common bills may include:

- Rent or mortgage

- Utilities

- Phone

- Internet

- Insurance

- Minimum debt payments

- Subscriptions

Autopay can be helpful, but only if the money is ready before the payment hits. If you use autopay, your payday routine should include checking which automatic payments are coming before your next paycheck.

A strong payday plan should feel like a payday money routine, not a stressful task you rebuild from zero each time.

Step 3: Move Savings and Debt Money Early

Savings often disappear when you wait until the end.

That does not mean you need to save a large amount from every paycheck. The point is to move something before the paycheck gets absorbed by everyday spending.

You might move money toward:

- Emergency savings

- Sinking funds

- Extra debt payments

- A planned future expense

Even a small amount can help if it is consistent. For example, moving $25 or $50 on payday is often easier than hoping the same amount is still there later.

Debt works the same way. Minimum payments should be planned early. Extra debt payments can come after bills and basic needs are covered.

After payday, it also helps to follow a monthly budget reset routine so your money stays organized beyond the first week.

Step 4: Set a Payday Spending Limit

After bills, savings, debt, and buffer money, you can decide what is actually available for spending.

This is where many people get payday budgeting wrong. They look at the bank balance and assume that is the amount they can spend. But the real spending amount is what remains after important jobs are covered.

Use this formula:

Available spending = paycheck – bills – savings – debt – buffer

For example:

- Paycheck: $1,800

- Bills: $950

- Savings and debt: $250

- Buffer: $100

- Available spending: $500

That $500 is the amount available for groceries, gas, household items, personal spending, and other flexible categories.

Example Payday Routine for a $1,800 Paycheck

Here is how the routine might look in real life.

Your paycheck arrives: $1,800

Before spending anything:

- Pay or set aside bills: $950

- Move savings and debt money: $250

- Protect a small buffer: $100

- Use the remaining amount for flexible spending: $500

That means the $1,800 in your bank account is not $1,800 of spending money. Only $500 is available for groceries, gas, household items, and personal spending.

This is the difference between seeing money and managing money.

Step 5: Decide Your “Do-Not-Spend-Yet” Money

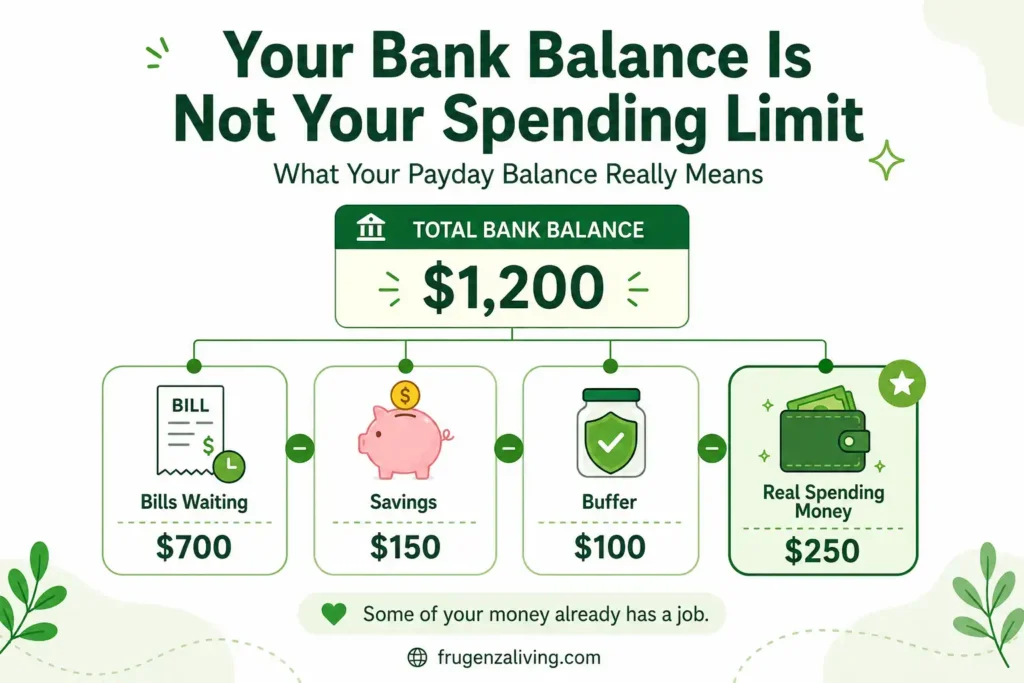

Your bank balance is not your spending limit.

This is one of the most important payday budgeting rules. Some money in your account may already belong to bills, savings, debt, or upcoming automatic payments.

To avoid confusion, mentally label your money:

- Bills waiting

- Savings waiting

- Spending money

- Buffer

For example, if your account shows $1,200 after payday, that does not mean you have $1,200 to spend. If $700 is already needed for bills, your real spending money is much lower.

This simple mindset can prevent a lot of accidental overspending.

Step 6: Plan Small Fun Money Without Breaking the Budget

A payday routine should not make you feel punished.

If your budget only covers bills and restrictions, you may quit after a few pay cycles. Planned fun money can help you stay consistent.

This might be $20, $30, $50, or another amount that fits your situation. The key is that it should come after bills, basic needs, savings, and buffer money.

Fun money is not the problem. Unplanned fun money is usually what breaks the budget.

When you plan it ahead of time, you can enjoy it without wondering if you just spent the electric bill.

If payday always feels messy, a money management plan for beginners can help you make clearer decisions.

Step 7: Review Before the Next Payday

A good payday routine does not end on payday.

A few days before your next paycheck, take 10 minutes to review what happened.

Ask yourself:

- Were all bills paid or set aside?

- Did any category go over budget?

- What surprised me?

- What should change next payday?

- Is there leftover money to roll over, save, or use as a buffer?

This review helps your next payday budget become more accurate. You are not trying to be perfect. You are learning your real spending pattern.

The 3-Account Payday Split

If one checking account makes your money feel confusing, try separating it into three simple places.

You do not need fancy accounts to start. You can use separate bank accounts, digital envelopes, or clear labels in your banking app.

A simple 3-account payday split can look like this:

- Bills account: money for rent, utilities, debt minimums, insurance, and subscriptions.

- Spending account: money for groceries, gas, household items, personal spending, and planned fun money.

- Savings or buffer account: money for emergency savings, sinking funds, and small surprises.

This makes your payday routine easier because your spending money is separated from money that already has another job.

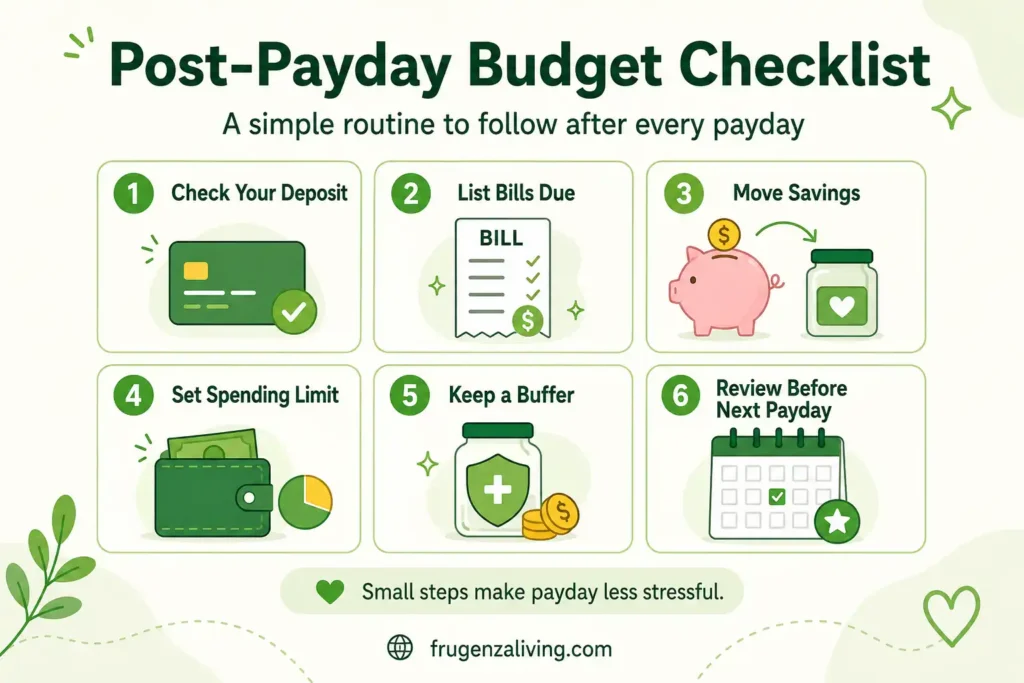

Post-Payday Budget Checklist

Use this checklist after every payday:

- Check your real deposit.

- List bills due before next payday.

- Pay or set aside bill money.

- Move savings or debt money early.

- Set your payday spending limit.

- Keep a small buffer.

- Give leftover money a job.

- Review before the next payday.

This routine should be simple enough to repeat. If it takes too long, you may avoid it. Start with the basics and improve it over time.

Common Mistakes After Payday

Even a good payday budget can break if a few habits repeat.

Watch for these common mistakes:

- Spending before checking bills: Bills should come before flexible spending.

- Using bank balance as spending money: Your balance may include money already assigned to bills.

- Waiting to save what is left: Savings often disappear if they are not moved early.

- Forgetting subscriptions: Small auto-payments can drain the budget quietly.

- Making the routine too complicated: A payday routine should be simple enough to repeat.

- Ignoring the next payday date: Your plan should last until the next paycheck arrives.

How This Is Different From a Paycheck Budget Template

This article is about your routine after payday.

A paycheck budget template is the worksheet you use to write the numbers down. A payday routine is the order you follow when the money arrives.

Final Thoughts: Budget Before Payday Money Disappears

Learning how to budget after payday is not about making money feel stressful. It is about giving your paycheck a simple order before spending begins.

Start by checking your real deposit. Then pay or set aside bills, move savings or debt money, set a spending limit, keep a small buffer, and decide what leftover money should do.

The routine does not need to be perfect. It just needs to happen before the money disappears into random purchases.

Payday feels better when the money already knows where to go.

FAQ

What should I do first after payday?

The first thing to do after payday is check your real take-home pay and list the bills due before your next paycheck. Do this before non-essential spending so your money has a clear plan.

How do I budget after getting paid?

To budget after getting paid, pay or set aside bills first, move savings or debt money early, set a spending limit for flexible expenses, keep a small buffer, and give leftover money a job.

Should I pay bills right after payday?

You should pay or set aside money for bills that are due before your next payday. If a bill is not due yet but will come before your next paycheck, keep that money protected.

How much money should I keep for spending after payday?

Your spending money should be what remains after bills, savings, debt, and buffer money. Use the formula: paycheck minus bills, savings, debt, and buffer equals available spending.

How do I stop overspending after payday?

Pause before spending, check your bills first, set a payday spending limit, and avoid treating your full bank balance as spending money. Planned fun money can also help reduce impulse spending.

The ideas shared here come from real-life experience and practical habits that actually work.

→ Read more about Jeffi

- How to Stop Buying Coffee Every Day Without Giving Up Coffee - July 25, 2026

- 8 Meals for One Without Leftovers—and How to Use the Rest - July 22, 2026

- 9 Cheap Dinners for One Person on a Budget That Feel Complete - July 20, 2026