If you’ve ever tried to make a budget and got stuck asking, “What categories should I even include?” you’re not alone.

That one question can make budgeting feel harder than it needs to be.

Some people create too many categories: coffee, snacks, toiletries, apps, clothes, gifts, gas, eating out, hobbies, home items, and ten more. At first, it looks organized. But after a while, it becomes exhausting to maintain.

A budget should make your money clearer, not turn your life into a spreadsheet.

That’s why this guide focuses on a simple budget categories list that beginners can actually use.

This is not a full budgeting system. It is not a zero-based budgeting method. It is not a monthly income breakdown.

It is a simple guide to help you decide which budget categories belong in your budget, which ones are optional, and which ones you can ignore until you actually need them.

What Is a Simple Budget Categories List?

A simple budget categories list is a basic set of groups used to organize your money, usually including essentials, flexible lifestyle spending, and future money categories like savings or debt payments.

For beginners, the best budget categories are broad, easy to understand, and simple enough to use every month.

Before You Build Your Budget Category List

Before adding categories, keep this in mind:

- Start with broad categories first

- Split categories only when they become confusing

- Avoid tracking every tiny purchase separately

- Choose categories that match your real life

Your budget does not need to look impressive.

It needs to be usable.

Before organizing categories, it’s helpful to understand how to start budgeting in a simple way.

The Best Budget Categories Are the Ones You Actually Use

A good budget does not need more categories.

It needs the right categories.

When I first started budgeting, I made the mistake of adding too many categories. It looked organized on paper, but I stopped using it because it was too much to maintain.

That is a common beginner problem.

A structured approach like zero-based budgeting can make your categories more meaningful.

You try to track everything perfectly, then the budget becomes a chore. After a few weeks, you stop checking it.

Simple budget categories work better because they reduce friction.

For example, you may not need separate categories for coffee, snacks, fast food, and restaurants. You can start with one broader category like “Dining Out” or “Food Outside Home.”

You can always split it later if it becomes a problem.

The goal is not to track every dollar perfectly.

The goal is to make your money easier to understand.

The 3 Main Types of Budget Categories

Most personal budget categories fit into three simple groups.

If you want simple budget categories for beginners, start with essentials, lifestyle, and future money before adding optional categories.

1. Essentials

Essentials are expenses you need to live and keep your basic life running.

This usually includes housing, groceries, utilities, transportation, insurance, and important bills.

These categories usually come first because they protect stability.

2. Lifestyle

Lifestyle categories are flexible.

They include things like dining out, entertainment, hobbies, subscriptions, shopping, and personal spending.

These are not always bad expenses. They just need visibility so they do not quietly take over your budget.

3. Future Money

Future money categories help you prepare for what comes next.

This includes savings, emergency fund, debt payments, irregular expenses, annual fees, gifts, repairs, and future goals.

Many beginners forget this group, but it is one of the most important parts of a realistic budget.

Once you define categories, the next step is to split your income into categories properly.

Quick Budget Category Snapshot

Here is the simplest way to think about your budget categories:

- Essentials: things you must pay

- Lifestyle: things you can adjust

- Future Money: things you prepare for

- Optional: things you add only if needed

This quick snapshot keeps your budget simple without making it incomplete.

Simple Budget Categories List for Beginners

Here is a simple budget categories list you can use as a starting point:

| Category Type | Budget Category | What It Covers |

|---|---|---|

| Essentials | Housing | Rent, mortgage, property fees, basic housing costs |

| Essentials | Groceries | Food, basic household groceries, everyday meals |

| Essentials | Utilities | Electricity, water, gas, trash, internet |

| Essentials | Transportation | Gas, public transit, parking, basic travel costs |

| Essentials | Insurance / Bills | Insurance, phone bill, required payments |

| Lifestyle | Dining Out | Restaurants, coffee, takeout, food delivery |

| Lifestyle | Entertainment | Movies, events, games, activities |

| Lifestyle | Subscriptions | Streaming, apps, memberships, digital tools |

| Lifestyle | Personal Spending | Clothes, hobbies, small wants, personal items |

| Future | Savings | Short-term or long-term saving goals |

| Future | Emergency Fund | Money for unexpected expenses |

| Future | Debt Payments | Credit cards, loans, extra debt payoff |

| Future | Irregular Expenses | Gifts, repairs, annual fees, medical costs |

This is enough for most beginners.

You can add more later, but you do not need to start with a complicated setup.

Essential Budget Categories You Probably Need

Essential budget categories are the foundation of your budget.

These are the categories that protect your basic needs.

Housing

Housing usually includes rent, mortgage, property costs, or shared living expenses.

For most people, this is the largest category.

Keep it simple. You do not need to split every small housing-related cost at first. Start with one housing category unless you need more detail later.

Groceries

Groceries cover the food you buy for home.

This category is different from dining out or delivery. Keeping groceries separate helps you see how much you spend on food you actually prepare.

If grocery spending feels unclear, you can later split it into groceries and household supplies. But beginners can keep it simple at first.

Utilities

Utilities may include electricity, water, gas, trash, and internet.

Some people include phone bills here too, while others put phone bills under “Bills.”

Either is fine.

The important thing is choosing one place and staying consistent.

Transportation

Transportation covers the cost of getting around.

That might include gas, public transit, parking, rideshare, basic car maintenance, or train passes.

If you own a car, you may eventually add a separate car maintenance category. But if you want easy budget categories, transportation can stay broad in the beginning.

Insurance / Bills

This category can include required monthly payments like insurance, phone bills, minimum debt payments, or other fixed bills.

Some people prefer separating insurance from bills.

But for beginners, grouping them together can make the budget easier to manage.

To see how categories work in real life, you can follow a simple budget example for one person.

Lifestyle Budget Categories You Can Keep Flexible

Lifestyle categories are not “bad.”

They simply need visibility.

This is where many budgets get messy because small flexible purchases add up quietly.

Dining Out

Dining out includes restaurants, coffee, takeout, and delivery.

If you often wonder where your money goes, this is one category worth keeping visible.

You do not need to separate coffee from restaurants unless that detail helps you make better decisions.

Entertainment

Entertainment covers fun activities.

Movies, games, events, concerts, hobbies, or weekend activities can go here.

This category helps you enjoy your money without pretending fun spending does not exist.

Subscriptions

Subscriptions are easy to forget because they renew automatically.

Streaming services, apps, memberships, cloud storage, and paid tools can go in this category.

Keeping subscriptions separate helps you spot services you no longer use.

Personal Spending

Personal spending is a flexible category for small wants.

This may include clothes, self-care, hobbies, small shopping, books, or personal items.

If your lifestyle spending feels too scattered, this category keeps things manageable.

Hobbies

Hobbies can be separate if they are a regular part of your spending.

For example, fitness, photography, crafts, gaming, or sports may deserve their own category if they affect your monthly money.

If not, keep them under personal spending.

Categories also help you apply realistic ways to save money every month more effectively.

Future Money Categories Most Beginners Forget

Future money categories are where a budget becomes more realistic.

Many beginners only plan for expenses they pay every month. Then a non-monthly cost appears, and the budget feels broken.

That is why future categories matter.

Savings

Savings should have its own category.

Even if the amount is small, naming it helps you treat saving as part of your plan.

If your goal is building consistency, you can connect this with realistic ways to save money every month.

Emergency Fund

An emergency fund is money set aside for unexpected costs.

This might include medical bills, urgent repairs, job loss, or sudden travel.

You do not need to build it overnight. Just having the category reminds you that emergencies should not depend only on leftover money.

Debt Payments

Debt payments should be visible.

This may include credit cards, loans, student debt, or extra payments beyond the minimum.

If you are using a method like zero-based budgeting for beginners, debt can become one of the “jobs” you assign money to. But in this article, the focus is simply knowing that debt deserves a clear category.

Irregular Expenses

Irregular expenses are costs that happen sometimes, but not every month.

Examples include:

- car repairs

- birthday gifts

- holidays

- annual fees

- medical costs

- clothing replacement

- school costs

- home repairs

This is one of the most forgotten beginner budget categories.

Adding it makes your budget feel more like real life.

Annual Fees

Annual fees are easy to ignore because they do not show up often.

But they can still surprise you.

Software renewals, memberships, insurance payments, professional fees, or yearly subscriptions may belong here.

You can keep annual fees inside irregular expenses unless they become large enough to need their own category.

Optional Budget Categories You May Add Later

Not every category belongs in every budget.

Some categories are useful only if they fit your life.

| Optional Category | When to Add It | Keep or Skip? |

|---|---|---|

| Pets | You have regular pet food, vet, or grooming costs | Keep if pets are part of your monthly expenses |

| Medical | You have regular medication, appointments, or health costs | Keep if health expenses are frequent |

| Clothing | You buy clothes often or need work/school outfits | Keep if it helps control shopping |

| Travel | You save for trips or visit family often | Keep if travel is planned |

| Home Supplies | You buy cleaning supplies, toiletries, or household items often | Keep if groceries feel too mixed |

| Education | You pay for courses, books, school, or learning tools | Keep if education is a real expense |

| Giving / Donations | You donate regularly or support family/community | Keep if it matters to your values |

Optional categories should make your budget clearer.

If they make it harder, skip them for now.

A Simple Budget Category Setup You Can Copy

Here is a simple setup you can copy into a notebook, spreadsheet, or budgeting app.

| Main Category | Subcategories | Notes |

|---|---|---|

| Essentials | Housing, groceries, utilities, transportation, bills | Start here first because these protect basic stability |

| Lifestyle | Dining out, entertainment, subscriptions, personal spending | Keep flexible and adjust when needed |

| Future Money | Savings, emergency fund, debt, irregular expenses | Helps prepare for later instead of reacting later |

| Optional | Pets, medical, travel, clothing, education, giving | Add only if these fit your real life |

This setup is simple enough to use, but complete enough for most beginners.

If you need realistic numbers for each category, a monthly budget example for single person can help. But for now, focus on choosing categories that actually belong in your life.

How Many Budget Categories Should You Have?

Most beginners can start with 8–12 budget categories.

That is usually enough to understand your money without making the system overwhelming.

A simple beginner list might include:

- Housing

- Groceries

- Utilities

- Transportation

- Bills

- Dining Out

- Entertainment

- Subscriptions

- Personal Spending

- Savings

- Debt

- Irregular Expenses

You can add more later if something feels unclear.

For example, if “Personal Spending” becomes too broad, you might split it into clothing and hobbies.

But do not split categories just to look organized.

Use this rule:

If a category helps you make better decisions, keep it. If it creates stress, simplify it.

Common Mistakes When Choosing Budget Categories

Choosing budget categories sounds simple, but beginners often make a few common mistakes.

Using Too Many Categories

Too many categories can make budgeting feel heavy.

If your budget takes too long to update, you may stop using it.

Start broad.

Copying Someone Else’s Budget Exactly

Someone else’s budget may not match your life.

A person with kids, pets, debt, or a car will need different categories than someone living alone.

Use examples as a guide, not as a rule.

Forgetting Irregular Expenses

This is one of the biggest mistakes.

If you forget non-monthly costs, your budget may look fine until something unexpected happens.

Irregular expenses deserve a place.

Separating Every Tiny Purchase

You probably do not need separate categories for coffee, snacks, apps, takeout, and small shopping right away.

Group similar spending first.

Split later only if needed.

Creating Categories That Do Not Match Real Life

Your budget should reflect how you actually spend.

If you never travel, you do not need a travel category yet.

If you spend on medical costs every month, you probably do need a medical category.

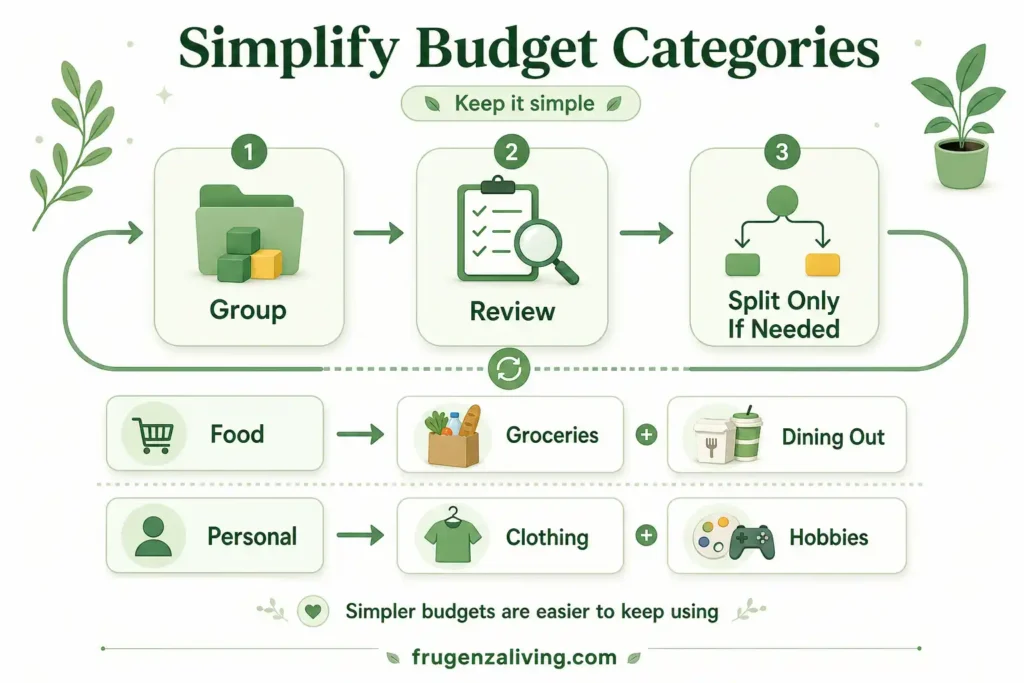

How to Simplify Your Budget Categories Over Time

A budget category list should not be frozen forever.

You can simplify it as you learn more about your spending.

Use this loop:

Group → Review → Split Only If Needed

Group similar spending first.

Review where money feels unclear.

Split a category only if it helps you make better decisions.

For example, start with “Food.”

Later, if needed, split it into “Groceries” and “Dining Out.”

Start with “Personal.”

Later, if needed, split it into “Clothing” and “Hobbies.”

The simpler your budget feels, the more likely you are to keep using it.

Once I stopped overcomplicating my categories and stuck to the basics, my money finally started to accumulate. That simple shift in visibility became one of the starting points that helped me save over $15,000 in a single year.

It was not magic.

It was just a system I could actually maintain.

When to Update Your Budget Categories, Not Just Your Numbers

Most budgeting advice tells you to review your spending numbers every month.

That is useful.

But there is a different kind of review that people almost never do: looking at whether the categories themselves still match your life.

Your budget categories are built around the version of your life that existed when you first created them.

When that version of your life changes, the categories can start working against you.

Here are three moments when your category list probably needs a structural update, not just a number adjustment:

When a major fixed expense disappears. If you finish paying off a debt, that monthly category does not automatically become free money. Without a new job assigned to it, the budget absorbs it silently into spending. The right move is to rename or redirect that category immediately — to savings, emergency fund, or the next debt — before the habit of spending it forms.

When your transportation situation changes. A person who stops driving and switches to public transit will have a “Car Maintenance” category sitting empty for months. An empty category is misleading. It makes the budget look like it has room that does not actually exist. Removing or merging outdated categories keeps the picture accurate.

When your income source changes. Moving from a salary to freelance work, or adding a side income, changes which categories matter most. A salaried employee might not need an “Irregular Income” buffer. A freelancer probably does. The categories need to reflect how money actually arrives, not just how it leaves.

The rule here is practical:

If a category has been empty or unchanged for three consecutive months, treat it as a signal. Either it no longer belongs in your budget, or it belongs in a different place.

Categories are not permanent labels.

They are tools. And tools that no longer fit the job should be replaced, not kept out of habit.

How This Fits Into Your Budgeting System

This article is only about choosing simple budget categories.

If you want realistic numbers, use a monthly budget example for single person.

If you want a method for assigning every dollar, zero-based budgeting for beginners can help.

If you do not know your actual spending yet, learning how to track expenses easily can give you clearer data.

And if you need the bigger beginner overview, simple budgeting for beginners can help you understand how all the pieces fit together.

The category list is just one part of the system.

But it is an important one because it gives your budget structure.

FAQ

What are simple budget categories?

Simple budget categories are broad groups that organize your money without making budgeting complicated. Common examples include housing, groceries, utilities, transportation, bills, dining out, entertainment, savings, debt payments, and irregular expenses. Beginners should start with broad categories and split them only when needed.

What categories should be in a beginner budget?

A beginner budget should usually include essentials, lifestyle spending, and future money categories. Essentials include housing, groceries, utilities, transportation, and bills. Lifestyle includes dining out, entertainment, subscriptions, and personal spending. Future money includes savings, emergency fund, debt payments, and irregular expenses.

How many budget categories should I have?

Most beginners should start with about 8–12 budget categories. This is enough to understand where money goes without making the budget overwhelming. If a category helps you make better decisions, keep it. If it creates stress, combine it with another category.

What budget categories do people forget?

People often forget irregular expenses, annual fees, medical costs, gifts, clothing replacement, car repairs, and emergency fund contributions. These expenses may not happen every month, but they still need a place in your budget so they do not feel like surprises.

Should I use detailed or simple budget categories?

Simple budget categories are usually better for beginners because they are easier to maintain. Detailed categories can be useful later, but too much detail can make budgeting stressful. Start broad, review your spending, and split categories only when the extra detail helps.

Conclusion

Budget categories should make your money easier to understand.

They should not make budgeting feel harder.

Start broad. Keep the list simple. Add detail only when it helps.

You do not need a perfect category system to begin.

You just need categories that match your real life.

Because a good budget does not need more categories.

It needs categories you can actually use.

The ideas shared here come from real-life experience and practical habits that actually work.

→ Read more about Jeffi

- How to Split Bills Between Paychecks Without Overloading One Check - August 9, 2026

- Subscription Audit Checklist: Find and Review Every Recurring Charge - August 9, 2026

- How to Budget for Subscriptions Without Surprise Renewals - August 7, 2026