When I first tried budgeting, I thought the problem was discipline.

I downloaded an app, set categories, and promised myself I would track everything. For the first three days, it worked. By the end of the week, I stopped checking. By the second week, I had no idea where my money went.

That experience made one thing clear: most budgeting advice doesn’t fail because it’s wrong. It fails because it’s too rigid for real life.

If you’re just starting, what you need isn’t a perfect system. You need a simple one that you can actually stick to.

Why Budgeting Feels Hard for Beginners

Budgeting feels difficult not because the concept is complicated, but because the execution often is.

At the beginning, most people try to control everything at once. Every expense is tracked, categorized, and limited. It sounds productive, but it quickly becomes exhausting. After a long day, even opening a budgeting app can feel like too much effort.

There’s also a psychological factor that many beginners don’t realize: decision fatigue. Research in behavioral economics shows that when mental energy is low, people tend to choose convenience over control. That’s why overspending often happens at night or during stressful periods.

In my own case, I realized most “budget failures” didn’t happen randomly. They happened after work, when I was tired and less likely to think carefully.

What “Simple Budgeting” Actually Means

Simple budgeting isn’t about tracking every cent perfectly.

It’s about creating a system that works even when you’re busy, tired, or distracted.

A simple budget should:

- be easy to maintain

- allow flexibility

- focus on awareness rather than perfection

Instead of trying to control every dollar, the goal is to understand your patterns and make small adjustments over time.

A good starting point is learning how to manage your daily spending before building a full budget.

Start With a Minimum Viable Budget

Your first budget does not need twenty categories. It only needs enough information to stop your money from feeling completely unplanned.

Start with four numbers: your take-home income, fixed bills, flexible essentials, and the amount left for savings and personal spending.

Fixed bills include expenses such as rent, insurance, debt payments, and regular utilities. Flexible essentials include groceries, transportation, household needs, and other costs that change from month to month.

After subtracting those expenses, decide how much of the remaining money can be saved and how much can be spent without creating problems later. This amount becomes your safe-to-spend number.

A minimum viable budget is useful because it gives you direction without requiring you to predict every purchase. Once this basic version works, you can add more detail only where it is genuinely helpful.

Build Your First Budget in 60 Seconds

Enter four simple numbers to estimate how much money is left for personal spending after your essentials and savings goal are protected.

Your monthly numbers

Use take-home income—the amount that actually reaches your bank account.

Your first-budget result

Estimated safe-to-spend amount

$0

This is what remains after fixed bills, flexible essentials, and your savings goal.

How to calibrate this budget next month

Do not try to make every week perfect. Let the first version show how your money behaves.

Check which categories were accurate and which estimates were too low or too high.

Adjust the unrealistic numbers while keeping the budget simple enough to use again.

Your numbers are calculated only in your browser and are not stored by this tool.

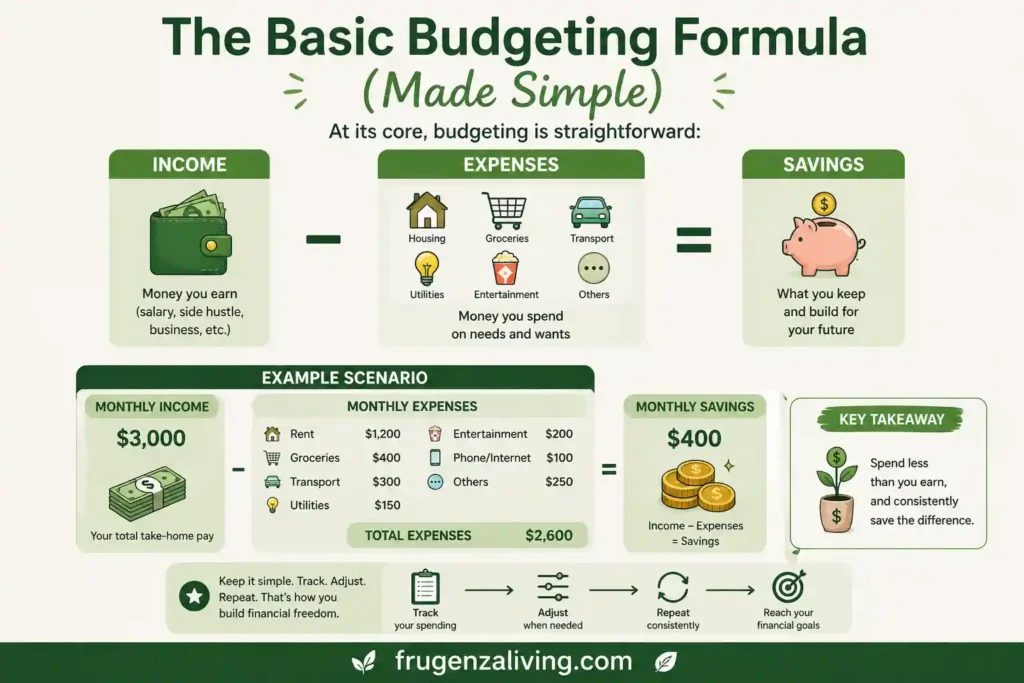

The Basic Budgeting Formula (Made Simple)

At its core, budgeting is straightforward:

Income – Expenses = Savings

But beginners often need more clarity than that.

Breaking it down helps.

Needs vs wants refers to essential expenses like rent, food, and bills compared to flexible spending such as eating out or entertainment. Fixed expenses stay the same each month, while variable expenses change depending on your habits.

Understanding this difference makes it easier to see where adjustments are possible without feeling restrictive.

If your income is limited, it helps to learn how to manage money on a low income in a way that fits your real situation.

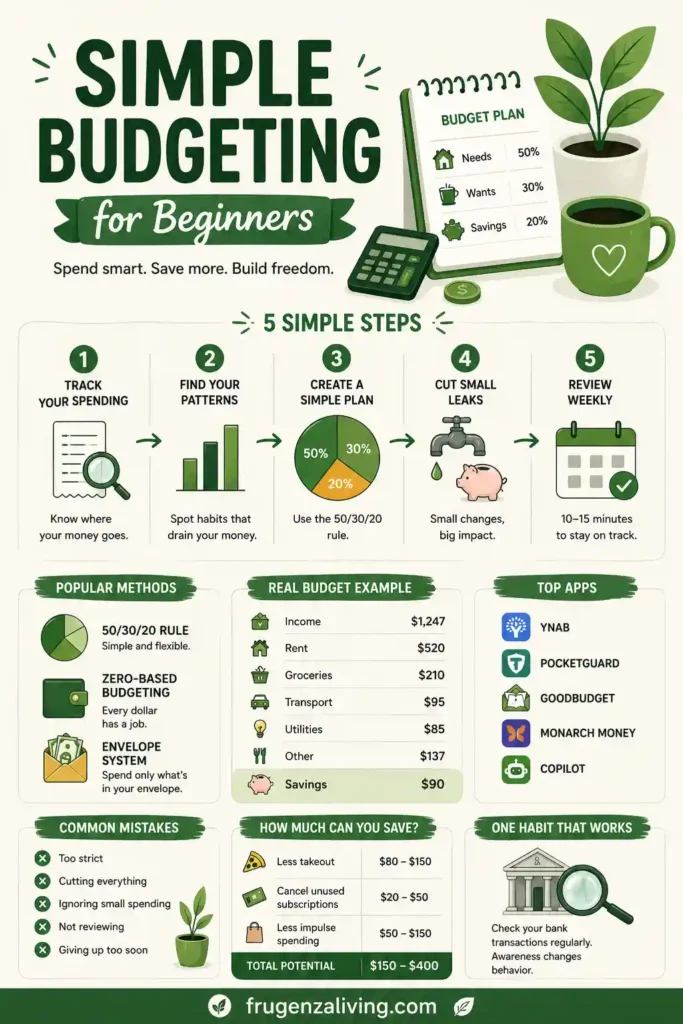

Step-by-Step Simple Budgeting for Beginners

Step 1: Track Your Real Spending (Not Estimated)

When I first reviewed my bank transactions honestly, I was surprised.

There wasn’t a single big expense causing problems. Instead, it was small repeated purchases like $4.50 coffee, $9 lunches, and $12 online buys that added up quickly. In one week, those small expenses reached over $120 without feeling significant at all.

Tracking real numbers creates clarity, and clarity is the first real step in budgeting.

This becomes even more important when you need to save money on a low income each month.

Step 2: Identify Spending Patterns

After tracking for a week or two, patterns start to appear.

You might notice spending more on food during weekdays, impulse purchases at night, or subscriptions that rarely get used. These patterns matter more than individual expenses because they repeat.

After setting up a simple plan, try a few easy budgeting methods to see what works best.

Step 3: Create a Simple Budget Structure

Instead of building a complex system, start with something flexible like the 50/30/20 rule.

Fifty percent goes to needs, thirty percent to wants, and twenty percent to savings. You don’t need to follow it perfectly. It’s a guide, not a rule.

If you prefer a simpler setup, you can budget without using apps and still stay organized.

Step 4: Reduce Small Leaks (Not Everything)

One mistake I made early on was trying to cut everything at once.

It didn’t work.

What worked instead was focusing on one category at a time. Reducing takeout from five times a week to two already made a noticeable difference without feeling restrictive.

If you’re new to budgeting, starting with basic budgeting tips can make the process feel much more manageable.

Step 5: Adjust Weekly (Not Daily)

Daily tracking quickly becomes overwhelming.

A weekly review is more realistic. Spending ten to fifteen minutes checking where your money went is enough to stay aware and make adjustments.

Popular Budgeting Methods (Simplified and Actionable)

50/30/20 Rule

This method is simple and flexible. It gives you a clear structure without requiring detailed tracking, making it ideal for beginners.

Zero-Based Budgeting

In zero-based budgeting, every dollar is assigned a role.

For example, if your income is $1,200, then your expenses and savings must equal exactly $1,200. This method gives full control but requires more consistency.

A budget only works if you can build daily money saving habits alongside it.

Envelope System

The envelope system uses separate categories for spending.

Once the allocated amount is used, spending stops. This approach works well for people who struggle with impulse purchases because it creates a clear boundary.

Best Budgeting Apps for Beginners (Updated)

Budgeting apps can help, but they should simplify your process.

YNAB is structured and ideal for detailed budgeting. PocketGuard shows how much you can safely spend. Goodbudget works well for envelope-style budgeting. Monarch Money offers modern tracking features, and Copilot provides automated insights for easier monitoring.

The most important part is not the app itself, but how simply you use it.

A Real Example of a Simple Monthly Budget

Here is a realistic example:

| Category | Amount ($) |

|---|---|

| Income | 1,247 |

| Rent | 520 |

| Groceries | 210 |

| Transportation | 95 |

| Utilities | 85 |

| Eating Out | 140 |

| Subscriptions | 32 |

| Miscellaneous | 75 |

| Savings | 90 |

This budget is not perfect, but it reflects real-life spending patterns that can be adjusted over time.

Budgeting works best when paired with frugal living basics that guide your everyday decisions.

Treat Your First Budget as a Forecast, Not a Final Answer

A beginner budget is an estimate of what you think will happen. It is not proof that you are good or bad with money.

Some expenses are easy to predict, such as rent or a phone bill. Others may change each month, including groceries, transportation, utilities, and personal spending. Instead of forcing these categories into one perfect number, give yourself a realistic range.

For example, if groceries usually cost between $190 and $230, budgeting exactly $190 may create unnecessary pressure.

A more realistic plan is to use the higher end of the range until you have enough information to make a better estimate.

At the end of the month, compare your plan with what actually happened. Keep the numbers that were accurate, adjust the categories that were unrealistic, and remove details that did not help. Your first budget is not supposed to be perfect. Its job is to teach you how your money behaves.

The Most Common Budgeting Mistakes Beginners Make

Many beginners struggle because they try to track everything perfectly, cut too many expenses at once, or ignore small daily spending.

These mistakes make budgeting harder to maintain and often lead to giving up.

The Hidden Problem: Why Budgets Usually Fail

Budgeting is often treated as a math problem, but it is actually a behavior problem.

Spending decisions are influenced by mood, energy, and habits. Even a well-planned budget will fail if these factors are ignored.

For example, most of my unnecessary spending happened when I was tired. Once I understood that pattern, it became easier to adjust.

One Unexpected Habit That Worked Better Than Apps

One habit made a bigger difference than any budgeting tool I tried.

Checking my bank transactions every few days.

Not analyzing deeply. Just looking.

At first, it felt too simple to matter, but over time it created awareness. That awareness naturally changed spending behavior.

How Much Can You Realistically Save

For most beginners, savings come from small changes:

| Change | Estimated Monthly Savings |

|---|---|

| Reduce takeout | $80 – $150 |

| Cut unused subscriptions | $20 – $50 |

| Reduce impulse spending | $50 – $150 |

| Total Potential | $150 – $400 |

The exact amount depends on your lifestyle, but small adjustments add up faster than expected.

Use a Budget Recovery Rule When You Overspend

Overspending in one category does not mean the entire budget has failed. It means your plan needs a small correction.

First, calculate the difference between what you planned and what you actually spent. Then decide whether the extra cost was temporary or whether the original budget was unrealistic.

An unexpected repair may be a one-time expense, while repeatedly exceeding the grocery budget may mean the category needs a larger amount.

If the overspending is small, spread the correction across the remaining weeks instead of making one extreme cut.

You might reduce optional spending slightly, delay one non-urgent purchase, or use part of the miscellaneous category.

Avoid taking money away from rent, basic food, medication, transportation to work, or required debt payments simply to make the numbers look balanced.

The purpose of a recovery rule is to keep one imperfect week from becoming an abandoned budget. Adjust the plan, protect essential expenses, and continue from where you are.

FAQ: Simple Budgeting for Beginners

What is the easiest way to start budgeting?

Start by tracking your spending for one week and identifying patterns.

Do I need a budgeting app?

No, simple tracking is often enough for beginners.

How often should I check my budget?

A weekly review is usually sufficient.

What if I overspend?

Adjust the next week. Budgeting is flexible.

How much should I save?

Aim for ten to twenty percent if possible, but any amount is a good start.

Ending

Budgeting doesn’t need to be complicated.

It just needs to work.

Start small. Track one habit. Adjust one pattern.

That’s enough to begin.

The ideas shared here come from real-life experience and practical habits that actually work.

→ Read more about Jeffi

- How to Split Bills Between Paychecks Without Overloading One Check - August 9, 2026

- Subscription Audit Checklist: Find and Review Every Recurring Charge - August 9, 2026

- How to Budget for Subscriptions Without Surprise Renewals - August 7, 2026