Getting paid every week can feel helpful because money arrives often. But it can also feel confusing when rent, utilities, insurance, phone bills, debt payments, and subscriptions are monthly.

That is why learning how to budget when paid weekly is not just about tracking spending. The real challenge is turning weekly income into a system that can handle monthly bills without leaving you broke by the end of the month.

Weekly pay is not the problem. The problem is that weekly income and monthly bills move on different calendars.

The goal is not to stretch one paycheck across a whole month. The goal is to make each weekly paycheck carry one small part of the month.

Editor’s note: This article is for general budgeting education only. It is not personalized financial, debt, tax, or investment advice. Adjust the weekly budget steps based on your income, bills, household size, and financial priorities.

Why Weekly Pay Feels Easy but Monthly Bills Feel Hard

Weekly pay creates frequent cash flow. That can make everyday spending feel easier because another paycheck is never too far away.

But most major bills are not weekly.

Rent may be due once a month. Utilities, insurance, phone bills, subscriptions, and debt payments may also follow a monthly schedule. This creates a calendar mismatch. You may feel fine in week one, then stressed in week three or four because several bills are coming due.

That does not always mean you are bad with money. It often means your paycheck timing and bill timing are not working together.

A weekly paycheck budget needs a bridge between weekly income and monthly expenses.

If you are paid every week, a weekly budget plan for beginners can make your money easier to organize before the next paycheck arrives.

How to Budget When Paid Weekly: Use the Weekly Bridge Method

The best way to budget weekly pay is to give each paycheck a clear job before spending starts.

I call this the Weekly Bridge Method because it helps bridge weekly paychecks into monthly bills.

This method works because it does not treat every weekly paycheck as free spending money. It gives weekly income a monthly purpose.

Step 1: List Monthly Bills Before Planning Weekly Spending

When you are paid weekly, do not start by asking, “How much can I spend this week?”

Start with this question:

“What monthly bills does this week need to help cover?”

List your monthly obligations first:

- Rent or mortgage

- Utilities

- Phone bill

- Insurance

- Subscriptions

- Debt minimums

- Childcare

- Transportation

- Annual or irregular bills

Annual and irregular bills are easy to forget because they do not show up every week. Examples include car registration, annual subscriptions, school fees, holiday spending, medical co-pays, gifts, tax prep fees, insurance premiums, and car repairs.

If you are behind on rent, utilities, or debt payments, contact the provider before the due date to ask about payment plans, hardship options, or due-date changes.

Step 2: Create a Weekly Bill Hold

A weekly bill hold is money you set aside from each weekly paycheck to cover monthly bills later.

There are two ways to calculate it.

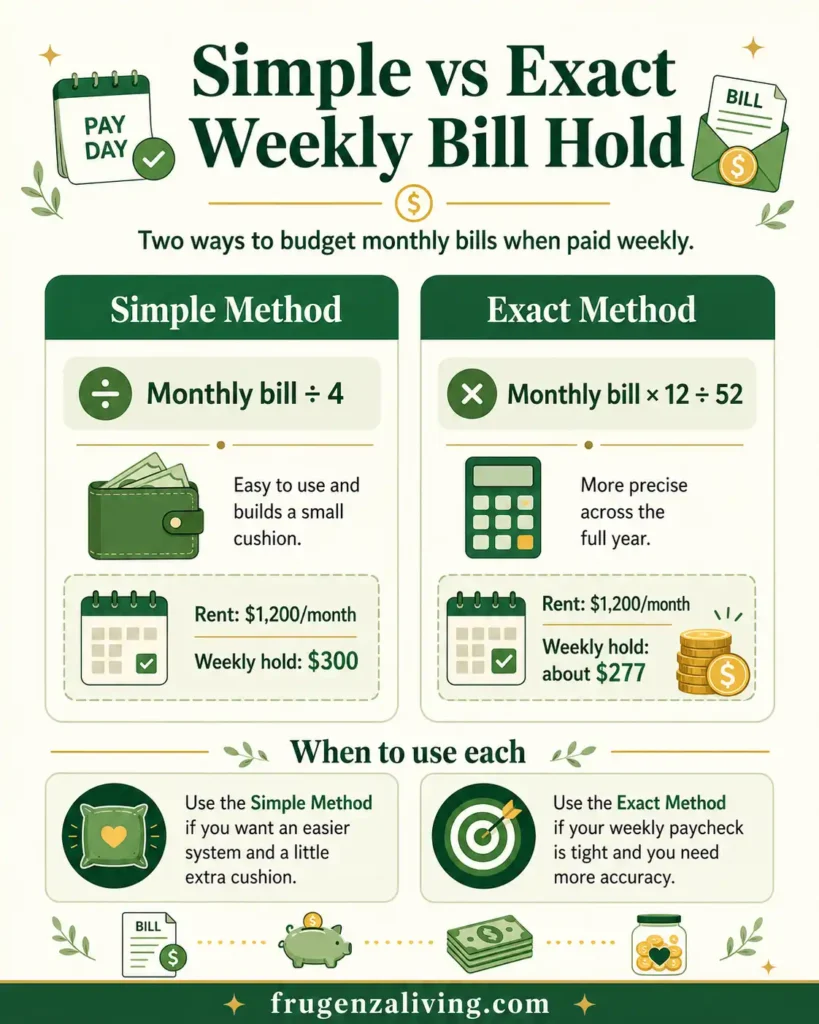

Simple method:

Monthly bill ÷ 4 = weekly hold

This is easy and creates a small cushion because some months have more than four weekly paychecks.

Exact method:

Monthly bill × 12 ÷ 52 = weekly hold

This spreads the bill across the full year more accurately.

For example, if rent is $1,200 per month, the simple method is $300 per week. The exact method is about $277 per week. The simple method builds extra cushion; the exact method is tighter but more precise.

For yearly expenses, use:

Annual cost ÷ 52 = weekly hold

If car insurance is $600 every six months, that is $1,200 per year. Divide $1,200 by 52 and you get about $23 per week.

If weekly pay feels hard to manage, a weekly paycheck budget template can help you separate bills, savings, and flexible spending before money disappears

Weekly Bill Hold Calculator

Use this calculator to estimate how much to hold weekly for a monthly, yearly, or semiannual bill. Use it for each bill, then add the weekly hold amounts together to find your total weekly bill hold.

Weekly Bill Hold Calculator

Enter a bill amount and choose how often it is due to estimate how much you should hold from each weekly paycheck.

Use this calculator for each bill, then add the weekly hold amounts together to find your total weekly bill hold. This calculator is for general budgeting education only.

When you are paid every week, divide monthly bills across weekly paychecks using a clear bill calendar.

What If You Are Starting in the Middle of the Month?

Weekly bill holds work best once the system has time to build. But if you start in the middle of the month, you may not have four weekly paychecks before the next big bill is due.

In that case, do not panic and do not expect the system to be perfect right away.

Bills due in the next 7 days should be paid or fully funded first. Bills due in the next 8–14 days need priority from this paycheck and the next one. Bills due later in the month can start building through weekly holds.

The goal is to slowly get one bill cycle ahead. A 5-paycheck month, overtime, tax refund, bonus, small spending cuts, or unused subscription cancellation can help you build the first bill cushion faster.

Step 3: Give Each Weekly Paycheck One Main Job

A weekly paycheck budget becomes easier when each paycheck has a primary job.

Assign paycheck jobs based on due dates, not just week numbers.

Use the 7-14-30 Rule:

- Bills due in 7 days: pay or fully fund now.

- Bills due in 14 days: fund from this paycheck and the next paycheck.

- Bills due in 30 days: build through weekly holds.

This is a planning rhythm, not a strict template. If rent is due early, Week 1 may focus mostly on housing. If insurance is due near the end of the month, Weeks 1–3 can slowly build that hold.

Weekly pay works better when you know how to budget after payday instead of waiting until the money is already spent.

Step 4: Protect Weekly Spending Categories

Weekly pay can disappear quickly when groceries, gas, takeout, household items, and personal spending all come from one mental bucket.

Separate your weekly spending into simple categories:

- Bill hold

- Groceries

- Transportation

- Household basics

- Personal spending

- Small savings

- Buffer

For example, if your take-home pay is $700 per week, your weekly plan might look like this:

- $350 bill hold

- $150 groceries and household basics

- $60 gas or transportation

- $50 savings or debt

- $60 flexible spending

- $30 buffer

The point is not the exact numbers. The point is that bill money leaves first, then weekly spending gets a clear limit.

What If Your Weekly Paycheck Changes?

Many weekly workers have variable pay because of changing hours, overtime, tips, shift schedules, or deductions.

If your weekly paycheck changes, do not build your fixed bills around your best paycheck. Use your lowest normal paycheck for essentials, then send overtime or extra hours toward buffer, debt, savings, or catch-up.

If your pay changes often, average your last 4–8 weekly paychecks. Use that average as a starting point, but keep essentials based on a conservative number.

Step 5: Build a Weekly Savings Floor

Saving weekly can feel easier than saving monthly because the amount can be smaller and more repeatable.

Your weekly savings floor is the smallest amount you can save every week without quitting.

It might be $5, $10, 1–5% of your weekly paycheck, or any small amount you can repeat consistently.

Saving $10 per week becomes $520 in a year before interest. That may not solve every emergency, but it can stop a small surprise from becoming a credit card balance.

The Consumer Financial Protection Bureau describes emergency savings as money set aside for unplanned expenses or financial emergencies.

Some people manage weekly pay better when they split their paycheck by percentage instead of guessing every Friday.

What to Do in a 5-Paycheck Month

If you are paid weekly, you usually receive 52 paychecks per year. That means some months will have five weekly paychecks instead of four.

Use the 80/20 fifth paycheck rule:

- 80% for catch-up, savings, debt payoff, sinking funds, or future bills

- 20% for guilt-free spending if essentials are already handled

Before spending a fifth paycheck, ask:

- Am I behind on any bill?

- Do I have a small emergency buffer?

- Would next month’s rent feel easier if I saved part of this?

- Is there a yearly bill coming soon?

A 5-paycheck month can be a quiet advantage if you give the extra weekly paycheck a job before it disappears.

Common Mistakes When Budgeting Weekly Pay

Avoid these mistakes if you want weekly pay to feel more stable:

- Treating every weekly paycheck as spending money. Some of each check may already belong to rent, utilities, insurance, or future bills.

- Forgetting monthly bills are coming. Weekly pay feels frequent, but monthly bills still need to be funded before the due date.

- Ignoring annual bills. Car insurance, annual subscriptions, holidays, school costs, and repairs need weekly holds too.

- Mixing grocery money with flexible spending. If groceries and wants share one bucket, takeout and small purchases can eat the food budget.

- Spending the fifth paycheck with no plan. A 5-paycheck month can reduce stress, but only if you use it intentionally.

Where This Fits in Your Bigger Budget

This article helps you turn weekly income into a monthly bill plan.

If you need a full layout, use a paycheck budget template. If you are paid every two weeks, a biweekly paycheck budget will fit better. If future expenses keep surprising you, sinking funds can help. If weekly spending gets loose, cash envelopes can make flexible categories easier to control.

Use the tool that matches your biggest problem first.

Final Thoughts

Weekly pay can be easier to manage when every paycheck has one clear job.

The key is to bridge weekly income into monthly bills, protect weekly spending categories, save a small amount consistently, and plan 5-paycheck months before they arrive.

If you are learning how to budget when paid weekly, start with one step: create a weekly bill hold. Once your monthly bills stop surprising you, the rest of your weekly budget becomes much easier to manage.

FAQ

How do I budget when paid weekly?

To budget when paid weekly, list your monthly bills first, divide them into weekly bill holds, protect groceries and transportation, save a small amount, and give each weekly paycheck a specific job.

How do I pay monthly bills when I get paid weekly?

Use a weekly bill hold. For a simple method, divide each monthly bill by four. For a more exact method, multiply the monthly bill by 12 and divide by 52.

What is the best weekly bill hold method?

The simple method is monthly bill divided by four. The more exact method is monthly bill multiplied by 12 and divided by 52. Use the simple method if you want a cushion and the exact method if your weekly paycheck is tight.

Should I budget weekly or monthly if I am paid weekly?

Use both. Plan monthly bills first, then manage your money with weekly checkpoints. This helps you cover monthly obligations while still controlling weekly spending.

How much should I save each week from my paycheck?

Start with an amount you can repeat consistently, such as $5, $10, or 1–5% of your weekly paycheck. The goal is to build the habit before increasing the amount.

What should I do with a 5-paycheck month?

Use a 5-paycheck month for catch-up, emergency savings, debt payoff, sinking funds, or next month’s bills. Spend a small amount guilt-free only after essentials are covered.

How do I stop spending my weekly paycheck too fast?

Separate bill-hold money from spending money first. Then create weekly limits for groceries, transportation, household basics, personal spending, and savings.

The ideas shared here come from real-life experience and practical habits that actually work.

→ Read more about Jeffi

- How to Split Bills Between Paychecks Without Overloading One Check - August 9, 2026

- Subscription Audit Checklist: Find and Review Every Recurring Charge - August 9, 2026

- How to Budget for Subscriptions Without Surprise Renewals - August 7, 2026