A household budget can feel tight even when you are not buying anything expensive.

Sometimes the pressure comes from rent, groceries, utilities, insurance, transportation, subscriptions, and small everyday purchases all stacking up at once.

The problem is not always that you spend too much in one place. Sometimes the real issue is that too many small and large costs repeat without being reviewed.

If you are looking for ways to reduce household expenses, the goal is not to cut everything you enjoy. The better goal is to find the costs that repeat, reduce waste, protect essentials, and keep the changes that actually fit your household.

The Fastest Ways to Reduce Household Expenses

The best ways to reduce household expenses are to review your biggest categories first, cut unused recurring bills, reduce food waste, lower utility waste, compare service plans, and track spending leaks for 30 days.

Start with the areas that usually affect your household budget most:

- housing

- food

- utilities

- transportation

- insurance

- subscriptions

- everyday spending

Cutting one small purchase may help, but reviewing several repeat costs together is usually more powerful than trying to fix your entire budget with one tiny habit.

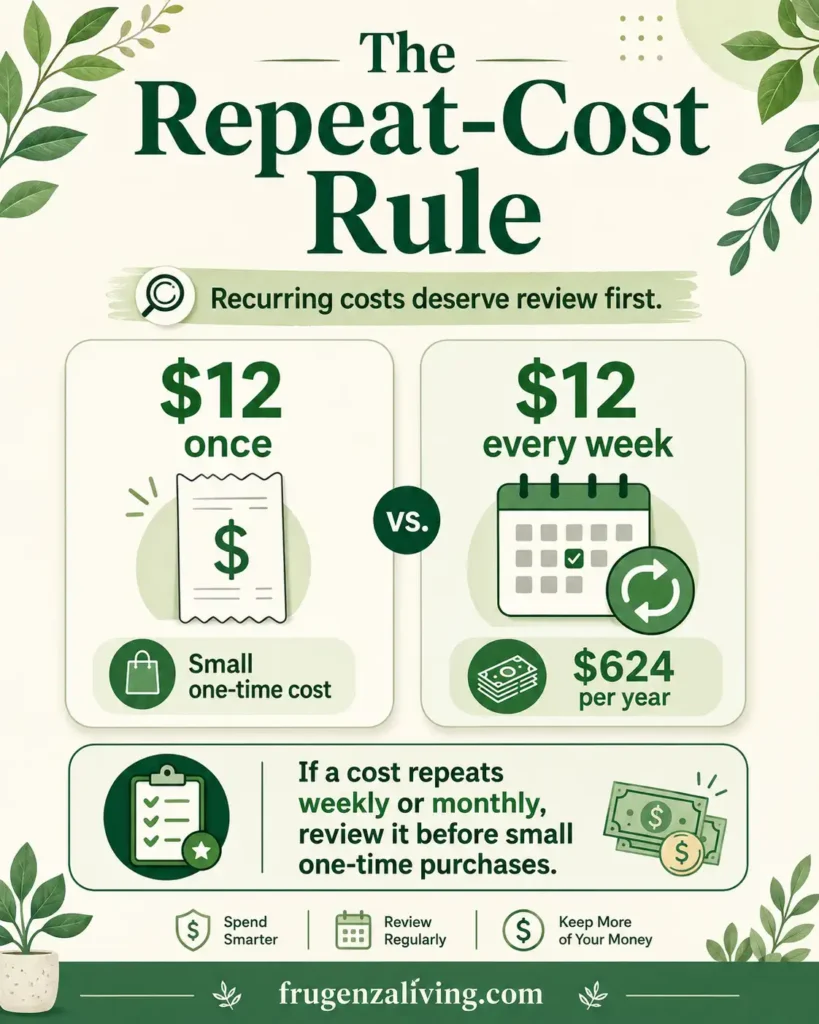

The Repeat-Cost Rule

If a cost repeats weekly or monthly, it deserves attention before one-time purchases.

A $12 purchase once is annoying.

A $12 charge every week is more than $600 a year.

This does not mean every recurring cost is bad. It means recurring costs deserve regular review because they quietly become part of your normal household spending.

Small home habits can help you reduce home costs without changing your lifestyle completely.

That is why a household expense audit should start with repeat bills, repeat habits, and repeat money leaks.

Start With the Big 6 Household Expense Categories

Household expenses are easier to reduce when you know where most of the money usually goes.

BLS household spending data shows that housing and transportation accounted for about half of household spending in 2024, while food accounted for 12.9%. Food expenditures averaged $10,169 per year, including groceries, restaurant meals, delivery, and takeout.

That does not mean small expenses do not matter. It means your first audit should focus on large repeat categories before you spend too much energy cutting tiny comforts.

A simple priority order:

- Safety and essentials first

- Recurring bills next

- Food waste and takeout

- Utilities and transportation habits

- Subscriptions and convenience spending

- Bigger changes like housing or insurance review

1. Housing

Housing may include rent, mortgage payments, property costs, renters insurance, repairs, or shared living expenses.

Ask: Is this cost fixed for the next 12 months, or is there a decision point coming soon?

That decision point could be lease renewal, refinancing, insurance renewal, moving, or finding a roommate.

2. Food

Food costs include groceries, takeout, delivery, snacks, school lunches, coffee runs, and food waste.

Ask: Is the problem grocery prices, food waste, takeout, or unplanned shopping trips?

Those are different problems, so they need different fixes.

3. Utilities

Utilities include electricity, water, heating, cooling, gas, internet, and phone service.

Repeated utility waste can quietly raise monthly household expenses, especially when habits repeat every day.

Reducing household expenses often starts with learning how to save money on electricity without making your home uncomfortable.

4. Transportation

Transportation includes fuel, public transit, car payments, insurance, maintenance, parking, rideshare, and unnecessary short trips.

Ask: Are you paying for car ownership, fuel, insurance, parking, rideshare, or unnecessary errands?

5. Insurance

Insurance is not something to cancel casually.

But reviewing coverage, comparing rates, and checking whether you are overpaying for old policies can be useful.

6. Subscriptions and Everyday Spending

Forgotten subscriptions, automatic renewals, app charges, convenience purchases, and impulse spending often feel small alone.

Together, they can quietly drain a household budget.

Fixed vs Flexible Expenses: Know What You Can Change First

Some household expenses are fixed, some are flexible, and some are semi-flexible.

Fixed expenses are harder to change quickly:

- rent or mortgage

- loan payments

- minimum debt payments

- insurance premiums

- some internet or phone contracts

Fixed expenses may take more effort, but even one change can create monthly savings that repeat.

Flexible or semi-flexible expenses can usually be adjusted faster:

- groceries

- takeout

- utilities

- transportation habits

- household items

- personal spending

- subscriptions

- month-to-month phone or internet plans

A smart household expense plan uses both: review fixed costs for bigger wins, then improve flexible habits for steady savings.

Household costs are easier to reduce when you also control daily expenses that quietly add up.

High-Impact Ways to Reduce Household Expenses

Use this quick guide as a priority map. It does not replace the full audit below; it simply shows where to start when you feel overwhelmed.

Household Expense Reduction Guide

Start With the Costs That Repeat

Reduce household expenses by reviewing the bills and habits that quietly drain money every month.

Recurring Bills & Insurance

High impactReview phone plans, internet, insurance, subscriptions, and service bills before cutting small comforts.

Food Costs

Weekly winUse meal planning, pantry checks, and fewer unplanned takeout meals to reduce food waste and grocery pressure.

Utilities

Easy leakTrack electricity, water, heating, and cooling habits so small household leaks do not repeat every month.

Transportation

Big categoryCombine errands, review fuel use, compare commuting options, and avoid unnecessary short trips when possible.

Spending Leaks

Hidden drainWatch small repeat purchases, forgotten renewals, convenience spending, and impulse buys that do not feel large alone.

Cut the repeat costs first, then improve the small habits you can keep every week.

What Household Expenses Should You Cut First?

Start with expenses that meet at least one of these conditions:

- it repeats every month

- you forgot you were paying for it

- it no longer supports your current life

- a cheaper plan gives the same value

- it causes stress but can be adjusted safely

- it creates waste, like unused food or unused services

One simple way to reduce household expenses is to spend less on cleaning products without sacrificing basic hygiene.

Good first targets include unused subscriptions, expensive phone plans, food waste, frequent takeout, high utility waste, and small purchases that happen automatically.

Do not start by cutting things that protect your health, safety, income, or family stability.

How to Lower Monthly Bills Without Making Big Changes

Lowering monthly bills often starts with bills that renew automatically.

Review:

- phone plan

- internet

- insurance

- streaming services

- cloud storage

- apps

- memberships

- delivery services

For each bill, ask:

- Do I still use this?

- Is there a cheaper plan?

- Can I pause it?

- Can I bundle or unbundle it?

- Is this bill worth its monthly cost?

Set a 20-minute bill review timer and choose only one bill to review first. Starting with one bill is better than opening every account, feeling overwhelmed, and quitting.

One small downgrade may not change everything. But several repeat-cost changes can reduce monthly expenses without making daily life feel restricted.

One simple way to reduce household expenses is to save money on water bill through small daily habits.

Run a Simple Household Expense Audit

Do not guess where the money is going.

Start by writing down:

- monthly bill total

- rent or mortgage

- utilities

- groceries

- transportation

- insurance

- subscriptions

- debt payments

- irregular expenses

- cash or card leaks

Consumer.gov recommends making a list of bills and other expenses, then comparing those costs with income so you can see what needs to change.

At the end of the audit, you should have three lists:

- costs to keep

- costs to reduce

- costs to cancel, pause, or compare

This does not need to be complicated. You can use a notebook, spreadsheet, budgeting app, or bank statement. The important part is seeing the full picture instead of only remembering the most obvious bills.

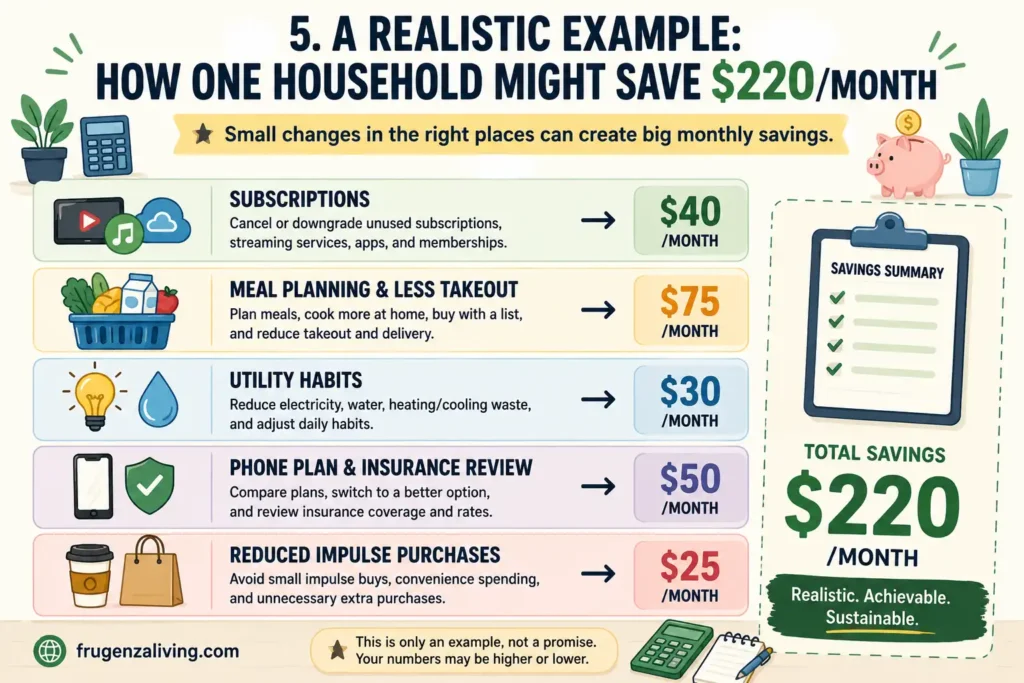

A Realistic Example: How One Household Might Save $220/Month

Here is a realistic example of how one household might reduce monthly expenses. Your numbers may be higher, lower, or zero in some categories.

For example:

- $40 from subscriptions

- $75 from meal planning and fewer takeout meals

- $30 from utility habits

- $50 from phone plan or insurance review

- $25 from reduced impulse purchases

Total: about $220/month

This is only an example, not a promise.

The point is that reducing household expenses often works better when you combine several realistic changes instead of trying to make one extreme cut.

A 30-Day Household Expense Reset

Start today by opening your last bank statement and highlighting every charge that repeats.

Week 1: Track every bill and recurring charge

Look at bank statements, credit cards, app subscriptions, insurance payments, loan payments, and service bills.

Output: a complete list of bills and recurring charges.

Week 2: Reduce food waste and plan meals

Check your pantry, fridge, and freezer before shopping.

Plan simple meals around what you already have. Reduce takeout by making backup meals easier.

Output: a simple meal plan and a short food waste list.

Week 3: Review utilities, phone, insurance, and subscriptions

Look for plans you can downgrade, cancel, compare, or renegotiate.

Focus on repeat costs before cutting small joys.

Output: three bills to cancel, compare, pause, or downgrade.

Week 4: Choose 3 habits to keep

Do not try to keep every new rule.

Choose three changes that feel realistic, then move any savings toward a goal, bill, debt payment, or small emergency buffer.

Output: three habits to keep next month.

What Not to Cut When Reducing Household Expenses

Reducing household expenses should not make your life unsafe or unstable.

Avoid cutting:

- needed medicine

- essential groceries

- insurance without understanding risk

- necessary maintenance

- safe heating or cooling

- anything that protects health, safety, or family stability

A lower bill is not worth creating a bigger problem later.

The goal is to reduce waste, not remove support.

Household Expense Tips for Renters and Families

Renters may not control rent increases, major repairs, insulation, or appliance upgrades.

But renters can still reduce household costs through utilities, food waste, subscriptions, phone plans, transportation habits, and spending leaks.

Families may need a slightly different approach. The goal is not to make every family member feel restricted. The goal is to reduce repeat stress.

Helpful options include:

- meal planning

- shared calendar for errands

- kid or family activity budget

- batch cooking

- subscription audit

- utility habits

For busy households, the best changes are often the ones that reduce decision fatigue.

A simple meal plan, one grocery list, and fewer unplanned errands can save money and mental energy at the same time.

My Simple Rule for Reducing Household Expenses

At Frugenza Living, we used to focus too much on tiny expenses.

But the bigger shift came from reviewing recurring bills, groceries, utilities, and spending leaks together.

A household expense audit made the pattern easier to see. Some costs were fixed. Some were flexible. Some were not necessary anymore. And some were small purchases that repeated so often they became real money.

Household expense audits, weekly check-ins, utility awareness, grocery planning, and reducing small money leaks became part of the system that contributed to saving over $15,000 in a year across multiple categories.

That number did not come from one trick. It came from combining many small and medium changes over time.

Your numbers may look different, but a household expense audit can still show where your money quietly disappears.

How This Fits Into Your Saving Money System

Think of this article as the household expense hub. The linked guides below go deeper into specific categories like utilities, home habits, daily spending, and short-term spending resets.

If you want broader home habits, read how to save money at home.

If utilities are a major pressure point, how to lower electricity bill at home can help you reduce energy waste.

If small purchases are the issue, how to control daily expenses effectively can help you find spending leaks.

If you need a short reset, no spend week challenge can help you pause nonessential spending for seven days.

FAQ

What are the best ways to reduce household expenses?

The best ways to reduce household expenses are to review major categories first, including housing, food, utilities, transportation, insurance, subscriptions, and everyday spending. Start with recurring costs, then adjust flexible spending habits.

What household expenses should I cut first?

Start with repeat costs that do not support your household anymore. This can include unused subscriptions, expensive phone plans, unnecessary service bills, food waste, frequent takeout, and small purchases that happen automatically.

What is a household expense audit?

A household expense audit is a simple review of your monthly bills, recurring charges, flexible spending, and money leaks so you can decide what to keep, reduce, cancel, pause, or compare.

How can I reduce household expenses without feeling deprived?

Focus on waste, not punishment. Keep essentials, protect health and safety, and reduce costs that repeat without adding much value. Meal planning, subscription audits, utility habits, and fewer impulse purchases can help without extreme sacrifice.

How do I lower monthly bills at home?

Lower monthly bills by reviewing phone, internet, insurance, utilities, subscriptions, and recurring services. Compare plans, cancel what you do not use, reduce energy and water waste, and check whether any bill can be negotiated or downgraded.

What are common household money leaks?

Common household money leaks include unused subscriptions, food waste, frequent takeout, convenience purchases, high utility waste, duplicate services, impulse buys, and small purchases that repeat every week.

How can I reduce household expenses in 30 days?

In 30 days, track every bill, cancel or downgrade unused recurring charges, plan meals to reduce food waste, review utilities and service plans, then choose three habits to keep next month.

How can families reduce household expenses?

Families can reduce household expenses with meal planning, batch cooking, shared errand planning, activity budgets, subscription reviews, utility habits, and regular household budget check-ins. The goal is to reduce repeat stress, not remove everything enjoyable.

How can renters reduce household costs?

Renters can reduce household costs by lowering utility waste, using removable draft stoppers, reducing food waste, reviewing phone and internet plans, canceling unused subscriptions, combining errands, and reporting maintenance issues that increase bills.

What is the difference between fixed and flexible expenses?

Fixed expenses are harder to change quickly, such as rent, loan payments, insurance premiums, minimum debt payments, and some contracts. Flexible or semi-flexible expenses are easier to adjust, such as groceries, takeout, utilities, transportation habits, personal spending, subscriptions, and month-to-month plans.

How often should I review household expenses?

Review household expenses at least once a month. A monthly review helps you catch new subscriptions, rising bills, food waste, seasonal utility changes, and small spending leaks before they become normal.

Final Thought: Cut the Repeat Costs First

Reducing household expenses does not mean cutting everything you enjoy.

Start with the bills and habits that repeat every month.

Review the biggest categories.

Reduce waste.

Protect essentials.

Then keep the changes that make your home budget feel lighter.

This article is for educational purposes only and is not professional financial advice. Household costs and savings vary by income, location, family size, housing, debt, and lifestyle.

The ideas shared here come from real-life experience and practical habits that actually work.

→ Read more about Jeffi

- How to Stop Buying Coffee Every Day Without Giving Up Coffee - July 25, 2026

- 8 Meals for One Without Leftovers—and How to Use the Rest - July 22, 2026

- 9 Cheap Dinners for One Person on a Budget That Feel Complete - July 20, 2026