Saving money as a single person can feel unfair sometimes.

Rent, utilities, groceries, transportation, insurance, subscriptions, emergencies, and social plans all depend on one income. There is no second household paycheck to absorb surprise bills or split the monthly basics.

That is why learning how to save money as a single person is not about cutting every joy or comparing yourself to couples.

It is about building a saving system that works with one income.

You need a plan that protects your fixed costs, controls small money leaks, keeps your social life realistic, and helps you save consistently without feeling like your whole life is restricted.

How Do You Save Money as a Single Person?

You save money as a single person by auditing fixed costs, building a small one-income buffer, controlling grocery and daily spending, setting a social spending boundary, automating small savings, and reviewing your money weekly.

The goal is not to save perfectly.

The goal is to make saving easier to repeat.

If you want to save money as a single person, start by looking at the areas that put the most pressure on one income: housing, bills, transportation, food, social plans, and emergency savings.

Why Saving Money Can Feel Harder When You Are Single

Saving money when single can feel harder because many expenses are not shared.

Rent may take a large part of your income. Utilities still need to be paid. Groceries may cost more per serving if food gets wasted. Transportation, insurance, phone bills, and emergency expenses all land on you.

Financial experts sometimes call this the “single tax”—the extra cost of living alone without someone to split the bills.

Social spending can also be tricky.

You may want to stay connected, but dinners, drinks, events, and weekend plans can quickly become expensive.

Cooking for one can create another challenge. If you buy too many ingredients, food spoils. If you are tired, takeout becomes tempting.

Still, being single is not only a disadvantage.

You can change routines faster. You can simplify meals. You can cancel unused subscriptions without negotiating with anyone. You can choose your own savings goals.

The key is building a system around one income instead of hoping money somehow works out.

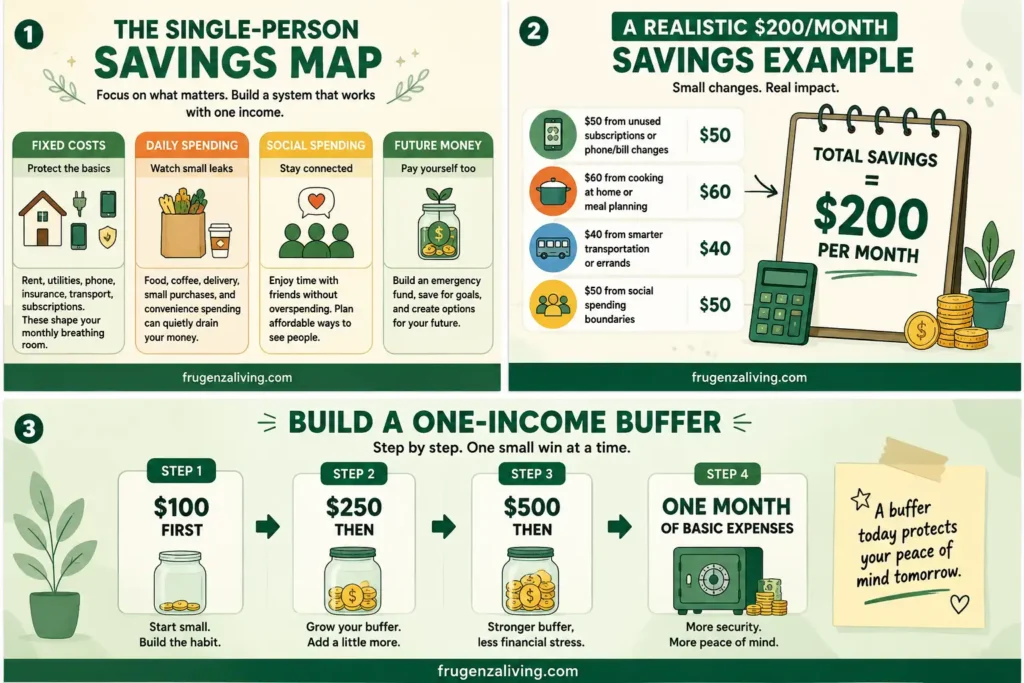

The Single-Person Savings Map

Use this simple map to decide where your money needs attention first:

This keeps your saving plan from becoming random.

You are not only asking, “How do I spend less?” You are asking, “Which part of my single-person budget needs the most attention first?”

Start With a Fixed-Cost Audit

Fixed costs matter more when you are single because they are not shared.

If your solo living expenses feel high, start with the bills that repeat every month before cutting small joys.

Before cutting every small purchase, review:

- rent or housing

- utilities

- phone plan

- insurance

- transportation

- subscriptions

- debt payments

You do not need to make a dramatic change right away.

Start with smaller questions.

Can you switch to a cheaper phone plan? Cancel two subscriptions? Review insurance rates? Reduce electricity waste? Compare transportation costs?

If housing is the biggest pressure point, do not rush into a major move. First, compare what you pay for location, commute, utilities, and quality of life. A cheaper place is not always cheaper if it increases transport costs or stress.

A fixed-cost audit matters because one reduced bill can save money every month without requiring daily willpower.

Saving money alone becomes easier when you follow a monthly budget for one person that matches your actual lifestyle.

Build a One-Income Buffer

A single person savings plan needs a buffer.

When you live on one income, a surprise bill can feel heavier because there may not be a second household income to soften it.

Aim for:

- $100 first

- then $250

- then $500

- then one month of basic expenses

The first goal is not a perfect emergency fund.

The first goal is a little distance between you and the next surprise bill.

Even a small buffer can make your money feel less fragile.

This is why a single income budget should leave at least a little room for future surprises, even if the amount starts small.

Control Food Spending Without Turning It Into a Full-Time Job

Food is one of the easiest places to lose money as a single person.

You buy groceries, use some of them, get busy, and then food spoils. Or you skip groceries and spend more on takeout.

Keep food simple.

Plan 3–4 repeatable meals, use frozen vegetables, keep backup meals, and cook once so you can eat twice.

If you live alone, keeping affordable staples for one person can make saving money much easier.

You do not need a complicated meal prep routine. You need a few reliable meals that stop you from starting every dinner from zero.

A weekly meal plan for one on a budget can help if food is one of your biggest spending leaks. If grocery shopping itself feels hard, saving money on groceries for one person can help you shop with less waste.

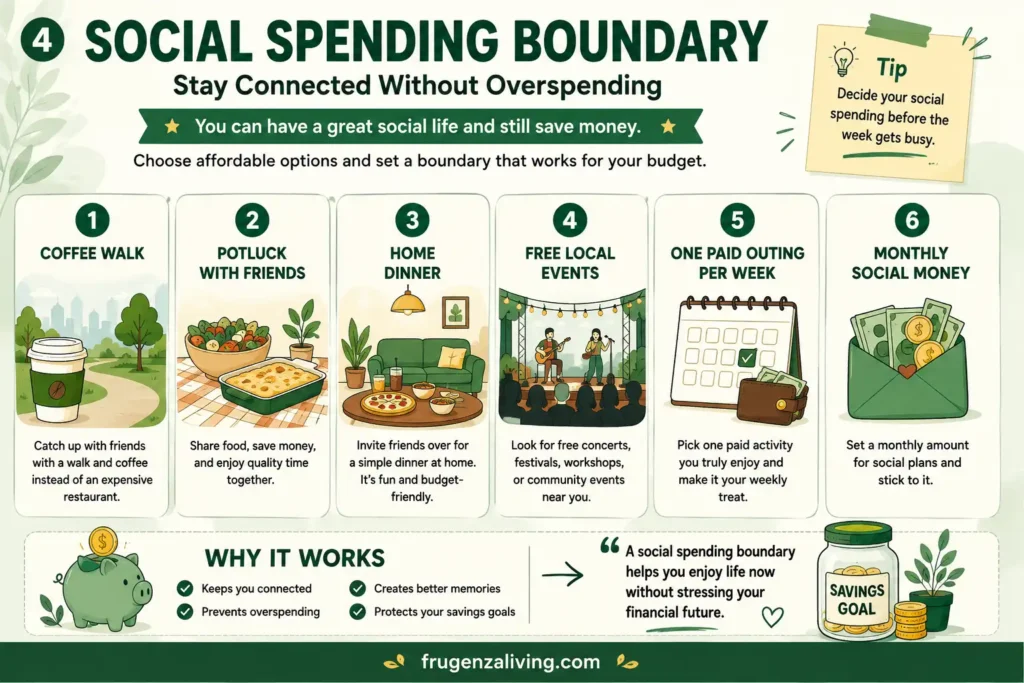

Set a Social Spending Boundary Without Isolating Yourself

Saving money as a single adult should not mean staying home forever.

You still need connection, fun, and a life that feels worth living.

The key is to decide your social spending before the week gets busy.

Try options like:

- coffee walk instead of dinner

- potluck with friends

- rotating dinner at home

- free local events

- one paid outing per week

- a monthly “social money” amount

The point is not to stop seeing people.

The point is to stop every connection from becoming a $40–$80 outing.

A social spending budget gives you permission to enjoy life without letting every weekend reset your progress.

Use the Single Advantage

Being single can be financially hard, but it also gives you control.

You can change your grocery routine quickly.

You can simplify meals without asking anyone else.

You can reset subscriptions, change spending habits, and choose your own saving goals.

For example, you can decide that this month is a low-takeout month, a subscription reset month, or a grocery simplification month without needing anyone else to agree.

You can also decide what matters to you without trying to match someone else’s lifestyle.

This is the “single advantage.”

You may not have shared bills, but you also have fewer shared decisions.

Use that flexibility to build habits that fit your life.

When you live alone, meal planning for one person helps you buy less randomly and use what you already have.

A Realistic $200/Month Savings Example

You do not always need one huge sacrifice to save money.

Sometimes the better approach is combining smaller changes.

For example:

- $50 from unused subscriptions or phone/bill changes

- $60 from cooking at home or meal planning

- $40 from smarter transportation or errands

- $50 from social spending boundaries

That adds up to $200 per month.

The exact numbers may look different for you.

The point is to spread the savings across several areas instead of relying on one painful cut.

Small changes can feel more sustainable when they do not all come from the same part of your life.

Create a Weekly Money Check for Singles

A weekly money check helps you stay aware without obsessing.

Once a week, review:

- bills due soon

- grocery plan

- social plans

- savings transfer

- one upcoming expense

This can take 10 minutes.

You are not trying to rebuild your whole budget every week. You are simply checking whether the week ahead matches the money you actually have.

If you want to save money living alone with less stress, this weekly check gives you a simple way to catch problems earlier.

If you want a broader system, how to save money weekly can help you build a repeatable routine.

If small expenses keep slipping through, how to control daily expenses effectively can help you find the leaks faster.

My Simple Rule for Saving Money as a Single Person

I stopped treating one income as only a disadvantage.

I started building systems around it.

For me, that meant looking at fixed costs first, keeping groceries simple, setting boundaries around social spending, and moving small amounts into savings before the week got busy.

It was not perfect.

But it was repeatable.

Building systems around one income, reducing fixed-cost pressure, planning groceries, and using small weekly savings routines became some of the habits that helped me save over $15,000 in a year.

Your numbers may look different, but building a system around one income can still make saving feel more realistic.

How This Fits Into Your Save Money System

Saving money as a single person works best when your system supports the biggest pressure points.

If food is one of your biggest costs, a weekly meal plan for one on a budget can make cooking for one easier.

If groceries disappear too fast, save money on groceries for one person can help you shop with more intention.

If small spending keeps adding up, how to control daily expenses effectively can help you spot everyday money leaks.

If your savings feel inconsistent, how to save money weekly can help you build a steadier rhythm.

FAQ

How do I save money as a single person?

You can save money as a single person by auditing fixed costs, building a small emergency buffer, planning food spending, setting social spending limits, automating small savings, and reviewing your money weekly.

How can I save money living alone?

To save money living alone, review rent, utilities, phone, insurance, subscriptions, groceries, transportation, and social spending. Start with recurring costs because reducing one monthly bill can help your budget every month.

What is a good budget for a single person?

A good budget for a single person should separate fixed costs, daily spending, social spending, savings, and an emergency buffer. The exact numbers depend on your income, city, debt, and priorities.

How much should a single person save each month?

A single person should save an amount that is realistic enough to repeat. That might be $25, $50, $100, or more depending on income and expenses. Start small if needed, then increase as your budget becomes more stable.

How can a single person reduce food costs?

A single person can reduce food costs by planning repeatable meals, using frozen vegetables, cooking once and eating twice, keeping backup meals, and avoiding groceries that spoil before they are used.

How can I have a social life while saving money?

You can have a social life while saving money by setting a social spending boundary and choosing lower-cost options like coffee walks, potlucks, free events, home dinners, or one planned paid outing per week.

Is it harder to save money on one income?

It can be harder to save money on one income because fixed costs and emergencies are not shared. This is sometimes called the single tax. But being single also gives you more control over routines, subscriptions, food choices, and savings goals.

Final Thought: Build a System Around One Income

Saving money as a single person is not about pretending one income is easy.

It is about protecting your fixed costs, controlling small leaks, planning social spending, and moving small amounts into savings consistently.

You do not need a perfect life to start saving.

You need a system that works with the income you have.

This article is for educational purposes only and is not professional financial advice.

The ideas shared here come from real-life experience and practical habits that actually work.

→ Read more about Jeffi

- Annual Expenses Checklist With a Fillable Yearly Planner - July 1, 2026

- Monthly Bills Checklist for Beginners: Track Every Payment Clearly - June 29, 2026

- How Much Should You Save Each Week? Calculate Your Ideal Target - June 28, 2026