The first time I tried budgeting, I didn’t start simple.

I downloaded multiple apps, watched a few videos, and tried to follow several systems at once. For a few days, everything felt under control. Then real life took over. I got busy, skipped tracking, and eventually stopped checking altogether.

At that point, it wasn’t a money problem. It was a system problem.

That experience changed how I see budgeting. Most people don’t fail because they lack discipline—they fail because the method they’re using doesn’t fit their daily life. That’s why focusing on easy budgeting methods is often more effective than trying to follow complex systems perfectly.

Why Most Budgeting Methods Feel Complicated

If you’ve ever searched for budgeting advice, you’ve probably seen dozens of methods that promise better control. Some ask you to track every expense, others require strict rules, and a few expect daily attention.

In theory, those systems make sense. In practice, they often feel overwhelming.

There was a point when I tried tracking every expense down to the smallest detail. It worked for a few days. After that, I started missing entries, then ignoring them, and eventually abandoning the system completely. The issue wasn’t effort—it was sustainability.

Research in behavioral finance also supports this pattern. When people experience decision fatigue, especially after work or during stressful moments, they tend to prioritize convenience over control. That’s exactly when most unplanned spending happens.

Before choosing a method, it helps to understand the core budgeting principles behind it.

What Makes a Budgeting Method “Easy” (and Actually Usable)

An easy budgeting method isn’t just simple on paper—it has to fit into real life without adding friction.

From experience, three things matter most. The method should feel light enough to repeat without thinking too much, flexible enough to handle unexpected situations, and clear enough to show when spending is getting out of control.

If a system fails in one of these areas, it usually doesn’t last.

The Basic Budgeting Foundation (Without Overthinking It)

Before choosing any method, you only need to understand one idea.

Income minus expenses equals savings.

Everything else builds on that.

Instead of overcomplicating categories, I found it easier to think in broad groups. Essentials like rent, groceries, and bills are non-negotiable. Flexible spending like takeout, shopping, or subscriptions is where most adjustments happen.

That shift alone makes budgeting feel more natural.

5 Easy Budgeting Methods (With Real-Life Context + Pros & Cons)

Instead of treating these as perfect systems, think of them as tools you can adapt.

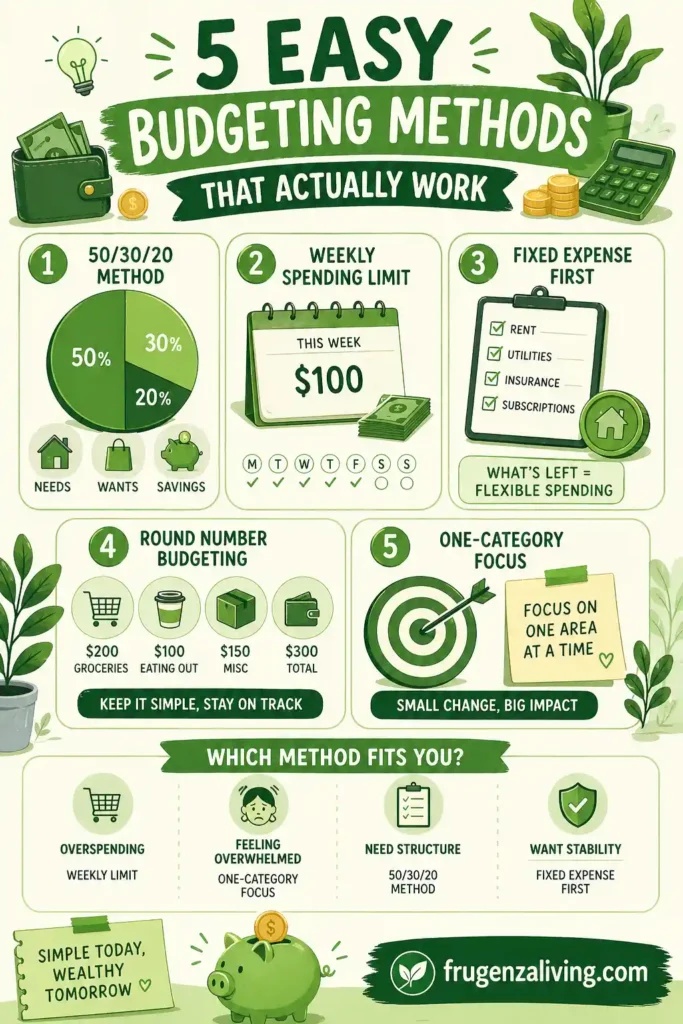

1. 50/30/20 Method (Best for Structure Without Stress)

This method divides income into needs, wants, and savings.

When I first tried it, it felt freeing because I didn’t need to track every detail. I just needed to stay roughly within a range.

However, it didn’t fully work for me at the beginning. Rent alone took more than half of my income, which made the 50 percent guideline unrealistic. That’s when I realized most budgeting advice assumes ideal conditions, not real ones.

This method works well if your income is stable and your fixed costs are manageable. If not, it still works as a guideline, but not as a strict rule.

Many methods work well with a no-app budgeting approach if you prefer simplicity.

2. Weekly Spending Limit (Best for Impulse Control)

This approach simplifies budgeting into one number per week.

I started using this after noticing that most of my overspending happened mid-month. Breaking my budget into weekly chunks made everything feel more manageable.

These methods work best when you apply budgeting methods in real life instead of just planning them.

What helped wasn’t the number itself, but the awareness it created. When I knew I had already used most of my weekly budget, I naturally paused before spending again.

It’s especially useful if your spending tends to happen in small, repeated amounts.

3. Fixed Expense First Method (Best for Stability)

This method focuses on covering essentials before anything else.

When I tried it, the biggest benefit was clarity. After subtracting rent, bills, and subscriptions, I knew exactly how much I had left.

That removed a lot of uncertainty. Instead of guessing what I could spend, I had a clear boundary.

The limitation is that it doesn’t automatically control lifestyle spending unless you actively monitor it.

4. Round Number Budgeting (Best for Simplicity)

This method removes precision and replaces it with simplicity.

Instead of tracking exact amounts, I started using rounded numbers. Groceries became 200 dollars, eating out became 100 dollars, and so on.

At first, it felt too loose. But over time, I realized it reduced mental load. I didn’t need to remember exact numbers or adjust constantly.

This works well if detailed tracking feels overwhelming, but it still requires awareness to stay within limits.

Even the best system won’t work unless you can stick to your budgeting system consistently.

5. One-Category Focus (Best for Overwhelm)

This is the simplest method I’ve used, and honestly, the one that made the biggest difference early on.

Instead of fixing everything, I focused on one category, which for me was takeout. I realized I was ordering food mostly when I was tired, not because I needed it.

Reducing that single habit didn’t fix everything, but it created momentum and made budgeting feel achievable.

No matter which method you choose, it works better when you keep track of your money.

A Real Example (What Changed Over Time)

Here’s a simplified version of how my spending changed after applying these methods:

| Category | Before ($) | After ($) |

|---|---|---|

| Takeout | 200 | 120 |

| Groceries | 200 | 230 |

| Random Spend | 150 | 90 |

| Savings | 80 | 180 |

Nothing extreme changed, but small adjustments created a noticeable shift.

Which Budgeting Method Is Best for You?

One thing I wish I understood earlier is that there’s no universal best method.

The right choice depends on your situation.

| Situation | Best Method |

|---|---|

| Overspending often | Weekly spending limit |

| Feeling overwhelmed | One-category focus |

| Need clear structure | 50/30/20 method |

| Want stability | Fixed expense first |

Instead of forcing a system, it’s better to choose one that fits how you already live.

Choose a Method Based on Where Your Budget Breaks

Instead of choosing a budgeting method based only on what sounds easiest, look at the point where your current budget usually stops working.

If you start the month with good intentions but overspend before the next payday, a weekly spending limit may give you faster feedback.

If bills make you unsure how much money is available, the fixed expense first method may create the clearest starting point.

If detailed categories make you avoid budgeting altogether, round number budgeting may reduce the mental load.

The one-category focus method works differently. It is useful when several parts of your budget feel messy, but one category—such as takeout, online shopping, or entertainment—is creating most of the pressure.

The 50/30/20 method may fit better when your income is predictable and your fixed costs leave enough room for broad percentage targets.

The important question is not “Which method is most popular?” It is “Which method addresses the exact moment where my budget usually breaks?” Matching the method to the problem makes it more useful from the beginning.

What Most Articles Don’t Tell You About Budgeting

Budgeting is not just about numbers, it is strongly influenced by timing and behavior.

Most of my unnecessary spending didn’t happen randomly. It usually happened after work, when I was tired. That’s when ordering food or buying something online felt easier than thinking.

Once I recognized that pattern, I didn’t need stricter rules. I just needed to adjust those moments.

Common Mistakes That Make Simple Methods Fail

Even simple systems can fail when expectations are unrealistic.

Trying multiple methods at once creates confusion. Being too strict makes the process feel restrictive. Expecting fast results leads to frustration.

Keeping things simple and consistent works better in the long run.

How to Choose the Right Method (Without Overthinking)

Instead of asking which method is best, ask which method you can repeat consistently.

A system works better when you build habits around your budget instead of relying on willpower.

If a method feels easy to follow, you will keep using it. And if you keep using it, it will work.

Run a 14-Day Budget Method Test

You do not need to commit to a budgeting method for an entire year before knowing whether it fits. Give one method a 14-day test instead.

During the test, keep the system as simple as possible. Do not change several spending habits at the same time.

Use the method normally and observe three things: how often you remembered to check it, whether it helped you make a spending decision, and whether you still understood how much money was available.

For example, when testing a weekly spending limit, you only need to know the weekly amount and how much remains.

When testing the fixed expense first method, focus on whether subtracting bills gave you a clearer spending boundary. When testing round number budgeting, notice whether the simpler estimates made you more likely to review your budget.

At the end of 14 days, do not ask only whether you saved money. Ask whether the method gave you useful information without requiring more effort than you could realistically maintain.

A method that creates clarity and is easy to repeat is worth refining. A method that you repeatedly avoid probably needs to be simplified or replaced.

How Much Can You Realistically Save

From what I’ve experienced, savings usually come from small adjustments:

| Change | Monthly Savings |

|---|---|

| Reducing takeout | 80 – 150 |

| Cutting random spending | 50 – 120 |

| Better weekly control | 50 – 100 |

| Total Potential | 150 – 300+ |

These numbers are realistic and sustainable over time.

Evaluate the Method, Not Just the Savings Number

The estimates above are examples, not guaranteed results. Actual savings depend on income, housing costs, household size, debt, location, current spending habits, and how much flexible spending is available to change.

A budgeting method can still be working even if the first month does not produce a large savings number.

Look for other signs of improvement: fewer surprise expenses, a clearer available-to-spend amount, fewer rushed transfers between categories, and less uncertainty before making a purchase.

You can evaluate the method with four questions:

- Did I understand how much money was available?

- Did the method help me pause before overspending?

- Could I maintain it during a busy week?

- Did I know what to adjust when the plan changed?

If most answers are yes, keep the method and improve it gradually. If the method provides useful structure but misses one weak area, add one small guardrail instead of replacing the entire system.

For example, you might combine the 50/30/20 method with a weekly limit for discretionary spending, or use fixed expense first with a one-category focus for takeout.

The best method is not necessarily the one that promises the largest savings. It is the one that helps you make clearer decisions consistently.

A Small Upgrade That Most People Ignore

One simple habit made a bigger difference than expected.

Checking spending regularly without trying to fix it immediately builds awareness. Over time, that awareness naturally changes behavior.

It is not about control. It is about noticing patterns.

FAQ: Easy Budgeting Methods

What is the easiest budgeting method?

The 50/30/20 method is often the easiest starting point because it provides a simple structure without requiring detailed tracking. You only need to divide your income into needs, wants, and savings, which makes it easier to follow consistently without feeling overwhelmed.

Do I need to track everything?

No, tracking every single expense is not necessary, especially for beginners. It is more effective to focus on spending patterns and repeated habits, such as frequent takeout or small daily purchases. This approach reduces stress and makes budgeting easier to maintain over time.

Why do simple methods work better?

Simple budgeting methods work better because they reduce mental friction and are easier to repeat consistently. When a system feels manageable, you are more likely to stick with it. Over time, consistency leads to better financial awareness and more sustainable spending habits.

How long until budgeting works?

Most people start noticing small changes within a few weeks, especially after identifying spending patterns and making simple adjustments. However, meaningful financial improvement usually takes a few months of consistent effort, depending on income, expenses, and how regularly the method is applied.

Ending

Budgeting doesn’t need to be perfect to work.

The simpler it is, the easier it is to stick with.

Start with one method, try it for a few weeks, and adjust as needed. Over time, consistency will create real results.

The ideas shared here come from real-life experience and practical habits that actually work.

→ Read more about Jeffi

- How to Split Bills Between Paychecks Without Overloading One Check - August 9, 2026

- Subscription Audit Checklist: Find and Review Every Recurring Charge - August 9, 2026

- How to Budget for Subscriptions Without Surprise Renewals - August 7, 2026