A yearly total can look manageable until several costs arrive within the same six-week period. A registration, insurance renewal, school cost, and annual subscription may be affordable across 12 months but difficult when they cluster together.

An annual expenses checklist should show what may happen, when action is required, how reliable each estimate is, and whether the household is ready for the deadline. This page focuses on predictable household costs that happen less often than monthly—not every regular monthly expense multiplied across a year.

What Should an Annual Expenses Checklist Include?

Record the expense name, type, due or likely month, action month, expected amount or range, timing confidence, amount confidence, amount already reserved, obligation level, and readiness.

A confirmed renewal is different from a seasonal estimate. The payment month may also differ from the month when you should compare alternatives, update documents, or cancel an optional service. Unlike a spending log, an annual expense tracker looks forward.

What Counts as an Annual Expense?

For planning, “annual” does not have to mean paid exactly once each calendar year.

Dated Annual Obligations

These have a known renewal window, such as insurance, vehicle registration, a professional license, annual membership, or software renewal.

Seasonal Expenses

These occur during a recognizable period, such as school costs, holiday spending, planned travel, or scheduled health or pet care.

Predictable Maintenance and Multi-Year Replacements

Routine servicing and foreseeable replacements may happen every few months or years. Tires, devices, appliances, passports, and household equipment can belong when timing is reasonably predictable.

A genuine emergency has timing and cost that cannot reasonably be predicted. Emergency savings may help with it, but the event itself is not a scheduled annual expense.

Quick Discovery Checklist

Check for:

- insurance renewals;

- registrations and licenses;

- annual subscriptions;

- school or activity costs;

- professional fees;

- planned health or pet care;

- holidays and travel;

- vehicle or home maintenance;

- replacements with a known cycle;

- quarterly or semiannual obligations.

Separating annual expenses from your regular monthly bills makes it easier to see which costs need their own savings plan.

Build the Checklist From Records

Review 12 to 24 months of bank and card activity when available. Search email for “renewal,” “annual,” “invoice,” “membership,” “registration,” “premium,” and “subscription.” Check app stores, digital wallets, insurance documents, service schedules, warranties, and household calendars.

Do not copy sensitive account details. You only need enough information to identify the expense, estimate the amount, and know when to review it.

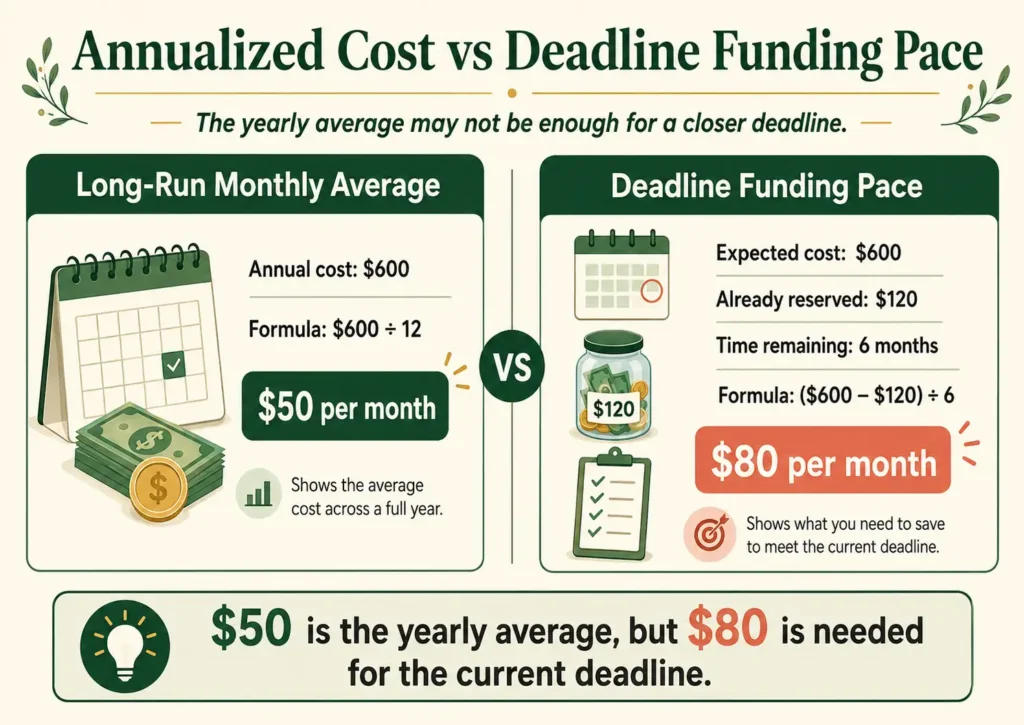

Annualized Cost and Deadline Cost Are Not the Same

Long-run monthly average

Annual recurring cost ÷ 12

This shows the average monthly effect of a full year’s costs. StepChange uses this conversion when turning yearly costs into monthly budget figures.

Deadline funding pace

(Expected cost − amount already reserved) ÷ contribution intervals remaining

For a $600 renewal with $120 reserved and six months left:

- Amount still needed: $480

- Required pace: $480 ÷ 6 = $80 per month

Dividing $600 by 12 gives $50, but that would not fully fund the nearer deadline.

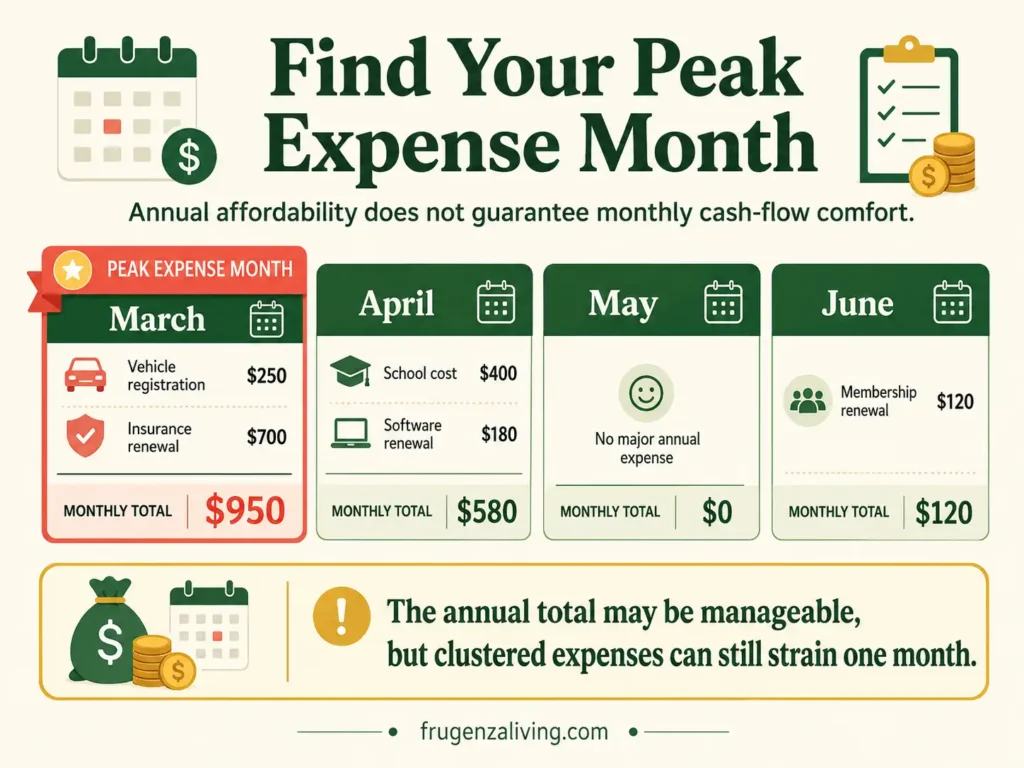

Find Your Peak Expense Month

A household may afford its predictable costs across a year and still face a difficult month. Vehicle registration and insurance might arrive in March, followed by a school payment and software renewal in April. That is expense clustering.

The CFPB Annual Planner, published within its Your Money, Your Goals companion materials, recommends mapping periodic expenses by month so timing becomes visible.

Use the month cards below to identify the highest-cost period. Use one currency consistently.

Annual Expense Timing Map

Use this map for predictable household costs that happen less often than monthly. Record timing, uncertainty, and readiness—not account or card details.

This is a manual worksheet. It does not calculate, save, or submit information. Entries may disappear after a refresh or when you leave the page. Use one currency consistently.

Before printing, expand all expense cards and worksheet sections. Then use your browser’s Print command and review the preview because browser layouts can differ.

If an amount is confirmed, enter the same figure in the low and high fields. Only record money already assigned to that specific expense. Do not count the same savings balance as reserved for multiple costs. Mark “Ready for expected deadline” only when the timing, planning amount, and required preparation are in place.

Annual Expense 1

Annual Expense 2

Annual Expense 3

Annual Expense 4

Annual Expense 5

Annual Expense 6

Twelve-Month Timing Strip

Count the expenses expected in each month and enter one consistent planning total. Use the higher estimate when you want to test possible cash-flow pressure.

Due-Soon Funding Check

Use these rows for the three nearest or most demanding expenses. Complete the math manually and use the same interval within each row.

Required pace = (planning amount − amount already reserved) ÷ intervals remaining.

Manual Annual Summary

For a confirmed expense, use the same number in both all-expenses totals. The confirmed subtotal is for reference and should not be added to those totals again.

Estimate Uncertain Costs Honestly

Use a confirmed amount when you have an invoice or renewal notice. If the amount is confirmed, enter the same number in both low and high fields. Use a range when the cost can vary, a prior actual cost as a reference, or “unknown” when evidence is insufficient.

A range such as $450–$550 is more honest than presenting $500 as guaranteed. Update it when better information arrives. Track timing confidence separately because you may know the likely month while the amount remains uncertain.

Use an Action Month Before the Payment Month

The renewal date is not always the first date that matters. An action month may be when you compare alternatives, review coverage, update a payment method, gather documents, or cancel an optional service.

Lead time depends on the provider, contract, and expense type. Check the terms rather than assuming one reminder period works for every expense.

Plan for Multi-Year Replacements

A $900 device expected to last three years has a long-run annualized cost of about $300 from the beginning of a new replacement cycle.

That does not mean you will pay $300 every year. If the item is already partway through its useful life, use its expected replacement date, amount already reserved, and intervals remaining to calculate the current deadline pace.

Move From the Checklist to the Budget

Use a long-run monthly average when a recurring cost is far enough away. Use the deadline pace when payment is closer. Give earlier attention to required, contractual, and due-soon costs.

For large predictable expenses, create a separate plan for large predictable expenses. When estimates change, bring the updated annual amounts into your monthly budget.

A Note for Irregular Income

Equal monthly preparation may not suit seasonal income. You may prepare more during stronger periods, but the total still has to meet the deadline. See how to adjust preparation around irregular income.

Review the Checklist at Useful Moments

Complete one full annual review, then update the map when a renewal notice arrives, before a high-cost quarter, after a major household change, or when a recurring service is added, canceled, or repriced.

The CFPB’s cash-flow guidance notes that large periodic payments can create timing pressure.

Common Annual-Expense Mistakes

Listing Categories Without Dates

Add a likely month and an action month.

Dividing Everything by 12

The average may be too low when the deadline is closer than 12 months.

Treating Estimates as Confirmed

Label ranges and unknowns, then update them.

Calling Predictable Maintenance an Emergency

Routine servicing and foreseeable replacements are planned expenses.

Counting the Same Reserved Money Twice

Assign a saved amount to one specific cost before recording it as reserved.

Looking Only at the Yearly Total

A manageable total can still produce a difficult peak month.

Use the Checklist to See Timing, Not Just Totals

An annual expenses checklist is useful when it shows what may happen, when it may happen, how reliable the estimate is, and whether the household is ready for the deadline.

Review the previous 12 months of bank, card, email, and household records. Add the first six non-monthly expenses to the timing map, label each estimate honestly, and identify the peak period. Then complete the due-soon check for the expenses that need action first.

This article provides general educational information, not individualized financial, legal, tax, insurance, or debt advice. Costs, renewal terms, deadlines, and legal obligations vary by provider and location.

The ideas shared here come from real-life experience and practical habits that actually work.

→ Read more about Jeffi

- Annual Expenses Checklist With a Fillable Yearly Planner - July 1, 2026

- Monthly Bills Checklist for Beginners: Track Every Payment Clearly - June 29, 2026

- How Much Should You Save Each Week? Calculate Your Ideal Target - June 28, 2026