Sinking funds can make budgeting easier, but they can also become overwhelming fast.

You may start with one fund for car repairs. Then you add holiday gifts, vacations, medical bills, home repairs, subscriptions, birthdays, clothes, school costs, pet care, and appliance replacement.

Suddenly, your budget has 12 tiny savings buckets, and payday feels more crowded than before.

So, how many sinking funds should I have if I want to stay prepared without making my budget harder?

For most beginners, the best starting point is 3–5 sinking funds. That gives you enough structure to prepare for predictable expenses, but not so many categories that your budget becomes a second job.

Editor’s note: This guide is for general budgeting education only. It is not personalized financial, tax, debt, banking, or investment advice. Adjust the examples based on your income, household size, bills, debt, savings, and local cost of living.

This guide uses a simplicity-first approach because sinking funds only work when they are easy enough to fund, remember, and maintain every payday.

How Many Sinking Funds Should I Have?

How Many Sinking Funds Fit Your Budget?

There is no universal perfect number, but 3–5 sinking funds is a realistic starting range for most people.

One or two sinking funds may be too broad if several predictable expenses keep surprising you. But 10 or more sinking fund categories can become hard to manage if your income is tight, irregular, or already stretched.

A simple range looks like this:

- 1–2 funds: very simple, but may be too broad

- 3–5 funds: best starting point for most beginners

- 6–10 funds: workable if your income and tracking system are stable

- 10+ funds: possible for detail-oriented budgeters, but easy to overcomplicate

The right number of sinking funds is not the number of expenses you can list. It is the number of expenses you can realistically prepare for.

If you are still new to this system, start with sinking funds for beginners before deciding how many separate funds you need.

Why Too Many Sinking Funds Can Backfire

More categories do not always mean a better budget.

Too many sinking funds can backfire because every fund needs money, attention, and tracking. If you are putting $2 into 15 different funds, you may technically be saving, but none of the funds may grow enough to help when a real bill arrives.

Too many categories can also slow down payday planning. Instead of asking, “What matters most this month?” you may feel stuck dividing small amounts across too many goals.

A sinking fund should lower budget stress, not create a second budgeting job.

Some financial education resources also warn that too many sinking funds can become overwhelming. MoneyHelper suggests keeping the system small, often around five or fewer, to avoid unnecessary complexity.

A proper sinking fund categories list can help you choose which funds actually matter for your real expenses.

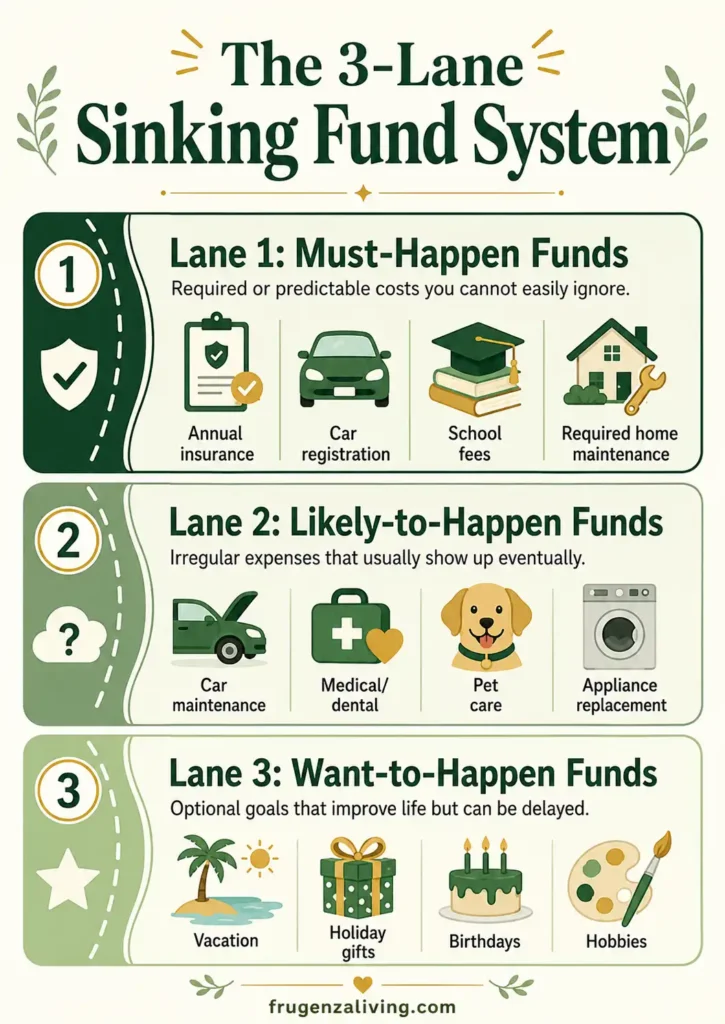

Use the 3-Lane Sinking Fund System

Instead of asking only, “How many sinking funds should I have?” ask a better question:

Which lane does this expense belong in?

The 3-Lane Sinking Fund System helps you organize your savings by priority instead of creating a separate fund for every possible expense.

Lane 1 comes first because these costs are predictable and often necessary. Lane 2 helps with expenses that may not have an exact deadline but usually happen. Lane 3 is still valuable, but it should not crowd out required expenses.

Once you decide how many funds to keep, a sinking fund tracker template can help you manage them without feeling overwhelmed.

The Best Sinking Funds to Start With

The best sinking funds to start with are the ones that would cause the most damage if ignored.

A practical beginner setup may include:

- Annual bills fund

For insurance, subscriptions, taxes, memberships, or yearly renewals. If one annual bill is much larger than the others, give it its own fund; otherwise, combine smaller renewals into one annual bills category. - Car or transportation fund

For oil changes, tires, registration, repairs, parking, or public transportation costs. - Medical, dental, or pet fund

For checkups, prescriptions, dental work, vet visits, or pet medicine. - Home or replacement fund

For appliance replacement, small home repairs, renter needs, moving costs, or household essentials. - Gifts and holidays fund

For birthdays, Christmas, seasonal events, family gatherings, or celebrations.

These are starting ideas, not required categories. A renter without a car will need different funds than a homeowner with children. Someone with pets may need a pet fund more than a vacation fund.

Some expenses belong in sinking funds, while others are better treated as emergencies, so learn the difference between planned expenses vs emergencies first.

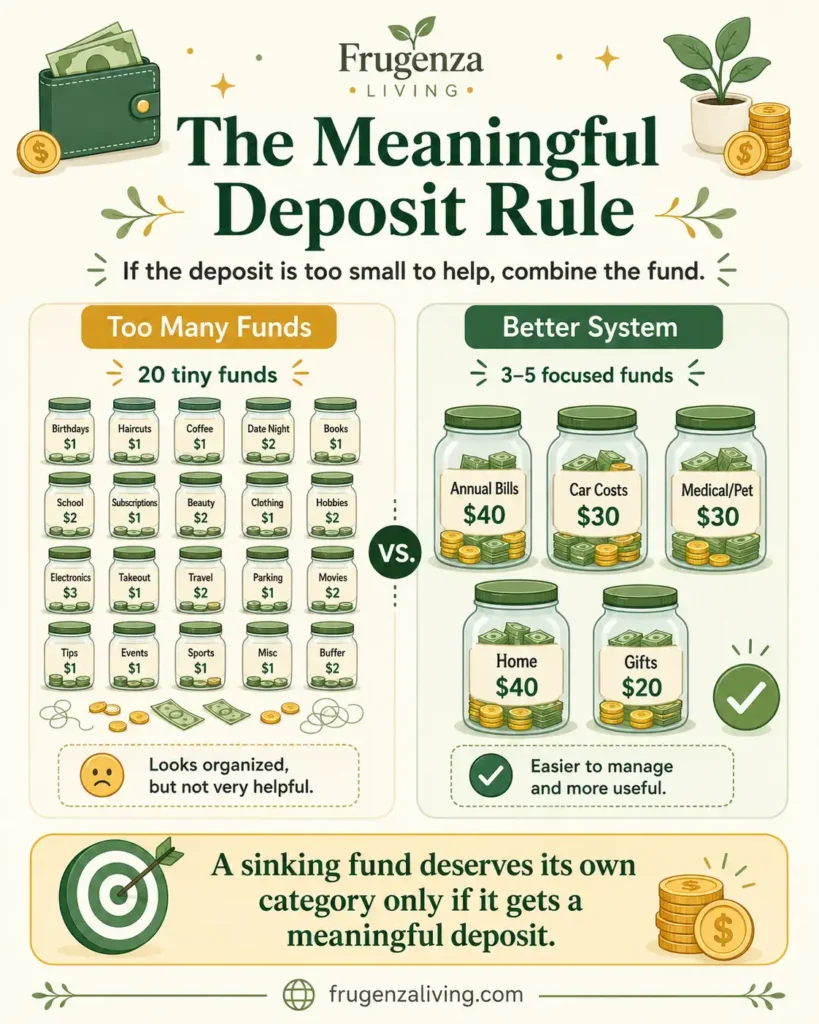

The Meaningful Deposit Rule

A sinking fund deserves its own category only if you can add a meaningful amount to it regularly.

That does not mean the amount must be large. It means the fund should grow enough to reduce stress when the expense arrives.

For example, putting $40 per month into a car registration fund may be useful. But putting $1 into 20 different funds may make your budget look organized without actually preparing you for anything.

Use this rule:

If a fund receives so little money that it will not help when the bill arrives, combine it with a broader category.

The Sinking Fund Limit Test

The Sinking Fund Limit Test

Before adding a new fund, use the Sinking Fund Limit Test.

If the answer is no to most of these questions, you may not need a separate sinking fund yet. Combine it, delay it, or keep it on a future list.

When You Should Combine Sinking Funds

Combining sinking funds is not failure. It is often smarter.

Broad categories are especially helpful when your income is limited, your budget is new, or you do not want to manage too many savings buckets.

For example:

- Birthday gifts + holiday gifts + small celebrations = Gifts & Celebrations

- Oil changes + tires + registration = Car Costs

- Vet checkups + pet medicine + grooming = Pet Care

- Appliance repair + small home fixes = Home Maintenance

- School fees + uniforms + kids activities = Kids & School

Use broad categories when you need simplicity. Use detailed categories only when your cash flow and tracking habits can support them.

For many people, five broad funds work better than fifteen tiny ones.

What Not to Turn Into a Sinking Fund

Not every expense needs a sinking fund.

Avoid creating sinking funds for:

- Daily groceries

- Normal monthly bills

- Tiny impulse purchases

- Every small want

- True emergencies

- Categories you cannot fund consistently

Groceries and regular bills should usually live in your normal monthly or paycheck budget. True emergencies belong in an emergency fund. Small wants can often fit inside flexible spending instead of becoming another category to track.

This keeps your sinking funds focused on predictable expenses that are too large, irregular, or easy to forget.

When It Makes Sense to Add More Sinking Funds

More sinking funds can work when your current system is already stable.

Add another fund only when your income is steady enough, your current funds are easy to track, the new fund has a clear purpose, and the deposit would be meaningful.

For example, if your broad “Car Costs” fund is working well, you might later split it into “Car Maintenance” and “Car Registration.” But if combining them keeps your budget easier, there is nothing wrong with leaving them together.

One Account or Separate Accounts?

Sinking funds do not need separate bank accounts. They need clear labels.

You can organize sinking funds in several ways:

- One savings account with spreadsheet labels

- One bank account with savings buckets

- Several subaccounts

- Digital envelope system

- Cash envelopes for short-term cash expenses

The method matters less than clarity. If you know what the money is for and you do not accidentally spend it, your system is working.

Avoid choosing a complicated system just because it looks more advanced. A simple system you actually use is better than a detailed system you abandon.

Signs You Have Too Many Sinking Funds

You may have too many sinking funds if:

- You cannot remember what each fund is for

- Most funds receive tiny amounts that do not help

- Optional categories crowd out required expenses

- Updating your budget feels exhausting

If this happens, simplify. Combine similar categories, pause low-priority wants, and focus on the funds that protect your budget the most.

Where This Fits in Your Bigger Budget

This article helps you choose the right number of funds.

For the full setup process, use a sinking funds for beginners guide. If you are not sure whether an expense belongs in a sinking fund vs emergency fund decision, compare the difference first. If you plan by paycheck, connect your sinking funds to a paycheck budget template so the transfers feel realistic.

This Frugenza Living guide is designed for general budgeting education. It focuses on helping readers choose a manageable number of sinking funds so their savings system stays useful, simple, and realistic.

Final Thoughts

So, how many sinking funds should I have?

For most beginners, start with 3–5 sinking funds. If your income is tight or irregular, keep the categories broader. If your income is stable and tracking feels easy, you can add more over time.

You do not need a separate sinking fund for every possible expense. The goal is not to create the most detailed budget. The goal is to make predictable expenses easier to handle before they become stressful.

Start simple. Fund what matters most. Add more only when your budget can support it.

FAQ

How many sinking funds should I have?

Most beginners should start with 3–5 sinking funds. This gives enough structure to prepare for predictable expenses without making the budget too complicated.

Can you have too many sinking funds?

Yes. You may have too many sinking funds if you cannot track them, most categories receive tiny amounts, or your budget feels more stressful instead of easier.

What are the most important sinking funds to start with?

The most important sinking funds to start with are the ones that would cause the most budget stress if ignored, such as annual bills, transportation costs, medical or pet costs, home replacement needs, and gifts or holidays.

Should I combine sinking funds?

Yes, combining sinking funds can make budgeting easier. For example, birthdays, holidays, and small celebrations can become one Gifts & Celebrations fund.

Should sinking funds be in separate accounts?

No, sinking funds do not need separate bank accounts. They need clear labels. You can use savings buckets, subaccounts, spreadsheets, or digital envelopes.

How often should I review my sinking funds?

Review your sinking funds at least monthly. Also review them before major seasons, annual bills, holidays, school costs, or any large predictable expense.

The ideas shared here come from real-life experience and practical habits that actually work.

→ Read more about Jeffi

- How to Split Bills Between Paychecks Without Overloading One Check - August 9, 2026

- Subscription Audit Checklist: Find and Review Every Recurring Charge - August 9, 2026

- How to Budget for Subscriptions Without Surprise Renewals - August 7, 2026